We can still learn much from Milton Friedman, who was born 100 years ago today. Here I focus on his role in the macroeconomic debates of the 1960s and 1970s, because they are so similar to the debates raging again today.

Friedman, Samuelson, and Rules Versus Discretion

First, go back to the early 1960s. The Keynesian school was coming to Washington led more than anyone else by Paul Samuelson who advised John F. Kennedy during the 1960 election campaign and recruited people like Walter Heller and James Tobin to serve on Kennedy’s Council of Economic Advisers. In fact, the Keynesian approach to macro policy received its official Washington introduction when Heller, Tobin, and their colleagues wrote the Kennedy Administration’s first Economic Report of the President, published in 1962.

The Report made an explicit case for discretion rather than rules: “Discretionary budget policy, e.g. changes in tax rates or expenditure programs, is indispensable…. In order to promote economic stability, the government should be able to change quickly tax rates or expenditure programs, and equally able to reverse its actions as circumstances change.” As for monetary policy a “discretionary policy is essential, sometimes to reinforce, sometimes to mitigate or overcome, the monetary consequences of short-run fluctuations of economic activity.”

In that same year Milton Friedman published Capitalism and Freedom (1962) giving the competing view on role of government which he then continued to espouse through the 1960s and beyond. He argued that “the available evidence . . . casts grave doubt on the possibility of producing any fine adjustments in economic activity by fine adjustments in monetary policy—at least in the present state of knowledge . . . There are thus serious limitations to the possibility of a discretionary monetary policy and much danger that such a policy may make matters worse rather than better . . . The basic difficulties and limitations of monetary policy apply with equal force to fiscal policy . . . Political pressures to ‘do something’ . . . are clearly very strong indeed in the existing state of public attitudes. The main moral to be had from these two preceding points is that yielding to these pressures may frequently do more harm than good. There is a saying that the best is often the enemy of the good, which seems highly relevant . . . The attempt to do more than we can will itself be a disturbance that may increase rather than reduce instability.”

Resolving the Disagreements

So there were two different views: the Samuelson view versus the Friedman view. The fundamental disagreement was not really over which instrument of government policy worked better (monetary versus fiscal), but rather over discretion versus rules-based policies. From the mid-1960s through the 1970s the Samuelson view was winning with practitioners putting many discretionary policies into practice.

But Friedman remained a persistent and resolute champion of his alternative view. At one time during the 1970s, F.A. Hayek even seemed to be siding with the discretionary approach, at least in the case of monetary policy. But Milton Friedman didn’t waver. In fact he sent a letter to Hayek in 1975 saying: “I hate to see you come out as you do here for what I believe to be one of the most fundamental violations of the rule of law that we have, namely discretionary activities of central bankers.” Fortunately, in my view, Friedman’s arguments eventually won the day and American economic policy moved away from such a heavy emphasis on discretion in the 1980s and 1990s.

The Debate Returns

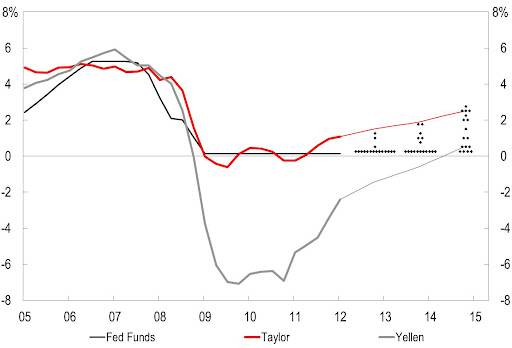

But this same policy debate is back today. Economists on one side push for more discretionary fiscal stimulus packages. They argue that the stimulus packages of 2008 and 2009 either worked or should have been even larger. They also push for more discretionary monetary policy such as the quantitative easing actions. They are not so worried about discretionary bailout policy, discounting the increased moral hazard that lack of a credible rule implies. In these ways they are descendants of the Samuelson school.

Other economists argue for more stable fiscal policies based on permanent tax reforms and the automatic stabilizers. They also push for a return to more predictable and rule-like monetary policy.They argue that neither the discretionary fiscal stimulus packages nor the bouts of quantitative easing were very effective, pointing to the risks of increased debt or monetization of the debt. They worry about the consequences of the discretionary bailouts. In these respects they are descendants of the Friedman school.

Of course there are many nuances today, some related to the difficulty of distinguishing between rules and discretion. You can see this, for example, in discussions of nominal GDP targeting, where some see it as a rule and some see it as a license to proceed with whatever discretionary action it takes. Interestingly, you frequently hear people on both sides channeling Milton Friedman to make their case.

Resolving the Debate Again

While academics are still the main protagonists, the debate is not academic. Rather it is a debate of enormous practical consequence with the well-being of millions of people on the line. Can the disagreements be resolved? Milton tended toward optimism that they could be resolved, and I am sure that this is one reason why he kept researching and debating the issue so vigorously.

Here people on both sides can learn from him. First, while a vigorous debater he was respectful, avoiding personal attacks and never failing to answer a letter. Second, he had a strong believe that empirical evidence would bring people together. He was influenced by statistician Leonard (Jimmie) Savage: Yes, people would come to the issue with widely different prior beliefs, but their posterior beliefs—after evidence was collected and analyzed—would be much closer. In this way the disagreement would eventually be resolved. I think we saw this in the late 1970s and the basic agreements lasted for at least two decades.

Unfortunately, posterior beliefs in the macro area now seem just as far apart as prior beliefs were 50 years ago. Clearly we have a lot of work to do, and clearly we can learn a lot from Milton Friedman in deciding how to proceed.