My Wall Street Journal article yesterday Monetary Policy and the Next Crisis touches on a growing research area in international finance that focusses on gross capital flows as distinct from the current account. For example, in his Ely Lecture at the American Economic Association Meetings this year, Maury Obstfeld argues that “large gross financial flows entail potential stability risks that may be only distantly related, if related at all, to the global configuration of saving-investment discrepancies.” And in a recent Princeton working paper, Valentina Bruno and Hyun Shin write that “Current account gaps have traditionally been considered as the drivers of cross-border capital flows. However, the most notable feature of international finance in recent decades has been the dramatic increase in gross capital flows that dwarf current account gaps.”

One obvious policy implication is that international economic policy groups such as the G20 should pay more attention in their “Mutual Assessment Process” to gross international capital flows rather than focus entirely on current account imbalances.

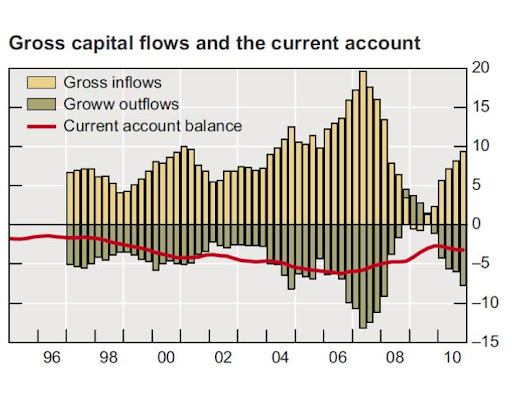

So far, however, the research (including Obstfeld’s Ely Lecture) has not dealt much with the impact of monetary policy on these flows, and that was the main purpose of my Wall Street Journal piece. The paper by Claudio Borio and Piti Disyatat Global Imbalances and the Financial Crisis: Link or No Link? shows that these flows rather than the current account or a global saving glut were the key international factors in the recent crisis. This chart of the U.S. balance of payments is from their paper. It nicely illustrates the importance of gross flows in comparison with the current account.