Yellen and Dudley discussed two rules. Using Yellen’s notation these are

R = 2 + π + 0.5(π – 2) + 0.5Y

R = 2 + π + 0.5(π – 2) + 1.0Y

where R is the federal funds rate, π is the inflation rate, and Y is the GDP gap. Yellen and Dudley refer to the first equation as the Taylor 1993 Rule and the second equation as the Taylor 1999 Rule, though the second equation was only examined along with other rules, not proposed or endorsed, in a paper I published in 1999.

The two rules are similar in many ways. Both have the interest rate as the instrument of policy, rather than the money supply. Both are simple, having two and only two variables affecting policy decisions. Both have a positive weight on output. Both have a weight on inflation greater than one. Both have a target rate of inflation of 2 percent. Both have an equilibrium real interest rate of 2 percent.

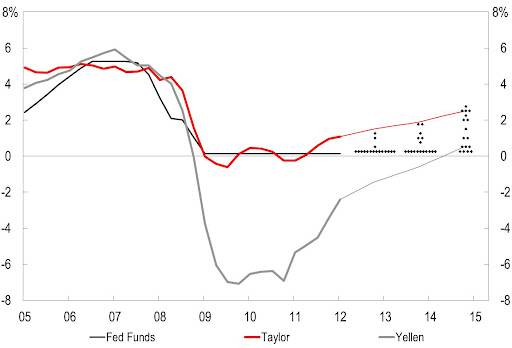

The two rules differ substantially, however, in their interest rate recommendations as this amazing chart constructed last April by Bob DiClementi of Citigroup illustrates. The chart shows two rules along with historical and projected values of the federal funds rate. The rule labeled “Taylor” by DiClementi is the rule I proposed. The other rule is labeled “Yellen” by DiClementi because it corresponds to the rule apparently favored by Yellen. The projected values are the views of FOMC members.

Observe that the first rule never gets much below zero, while the second rule drops way below zero during the recent recession and delayed recovery. The difference continues though it gets smaller into the future. Note that the projected interest rates by FOMC members span the two rules.

This big difference between the two rules in the graph can be traced to two factors: (1) The second rule has a much larger GDP gap, at least as used by Yellen. (2) The second rule has a much bigger coefficient on the GDP gap.

In my view, a smaller value of the GDP gap and a smaller coefficient are more appropriate. This view is based on a survey of estimated gaps by the San Francisco Fed and simulations of models over the years. But given the striking differences in DiClememti’s chart, more research on the issue by people in and out of the Fed would certainly be very useful.