The Financial Crisis Inquiry Commission (FCIC) will meet with more economists on February 26-27 to delve into causes of the crisis, considering in particular: monetary policy, derivatives, shadow banking, GSEs, and bailouts of “too big too fail” institutions. The forum is part of their “ongoing efforts to hear from academic experts and economists on issues related to the crisis.” Many of these issues were also covered in an FCIC hearing last October in which I was joined by Luigi Zingales and Joe Stiglitz. Here are my written answers to some of the FCIC questions, in which I stressed the role of monetary policy, GSEs, and bailouts in causing and prolonging the crisis.

More Economists To Meet with Financial Crisis Inquiry Commission

Posted in Financial Crisis

Comments Off on More Economists To Meet with Financial Crisis Inquiry Commission

New Book on How to End Government Bailouts

America is sick of bailouts. As President Obama called out in the State of the Union “we all hated the bank bailout. I hated it. I hated it. You hated it.” But the bailout mentality continues, and hate alone will not make it go away. So how can we end bailouts?

America is sick of bailouts. As President Obama called out in the State of the Union “we all hated the bank bailout. I hated it. I hated it. You hated it.” But the bailout mentality continues, and hate alone will not make it go away. So how can we end bailouts?

“Make failure tolerable” is George Shultz’s answer, as he explains in the lead essay of a new book in which a dozen policy makers, economists, and lawyers delve into the problem and come up with answers. The book is Ending Government Bailouts as We Know Them and is edited by Ken Scott, George Shultz and me.

If you look through the book, you’ll find

Paul Volcker explaining why his plan to further limit banks will reduce bailouts

Nick Brady reminding us that it wasn’t this way when he was on Wall Street or in the Treasury

Kimberly Summe telling the story of the Lehman Brothers bankruptcy (she was a lawyer there)

John Taylor confessing that systemic risk is not a well-defined concept after all

Darrell Duffie showing how contingent convertible debt is part of the answer

Richard Herring developing wind-down plans for big global financial firms

Joe Grundfest comparing such plans with pre nuptial agreements and Tiger Woods travails

Bill Kroener reviewing the pros and cons of an expanded FDIC operation (he was at the FDIC)

Tom Hoenig (with Chuck Morris and Ken Spong) laying out the rules-based Kansas City plan

Tom Jackson designing a disruption-free Chapter 11F bankruptcy plan for financial firms

Ken Scott evaluating whether the proposals work in theory and in practice

You will also find Gary Stern, Peter Wallison, Monika Piazzesi, David Skeel, Ernie Patrikis, Bob Hall and many others critiquing . With the Obama administration’s bringing Volcker’s ideas into the spotlight and Congressional Republicans finding new support for their bankruptcy ideas, it looks like the book is as timely as it could be.

Posted in Financial Crisis

Comments Off on New Book on How to End Government Bailouts

An Exit Rule as an Exit Strategy for Monetary Policy

Today’s hearing at the House Committee on Financial Services on “Unwinding Emergency Federal Reserve Liquidity Programs and Implications for Economic Recovery” was cancelled because of snow. The hearing was to focus on whether the Fed’s extraordinary measures have worked and on an exit strategy from these measures. Ben Bernanke was to testify at the hearing and according to press reports he was to discuss the Fed’s exit strategy. His testimony will be posted on the Fed’s website.

I was asked to be a witness at the same hearing on a panel following Ben Bernanke’s testimony. Witnesses were asked to give an assessment of whether the extraordinary measures have worked and what is an appropriate policy for unwinding them. Here is the paper which I originally prepared for the hearing; it represents what I would have presented.

The term “exit rule” emphasizes that an exit strategy should describe how reserves and the Fed’s portfolio composition are to be adjusted over time in a predictable way in order to achieve the exit, much like a policy rule for the interest rate. I also propose a particular exit rule that might help policymakers develop such a strategy. It will be interesting to see whether the exit strategy in Ben Bernanke’s testimony has such predictable features.

Posted in Monetary Policy

Comments Off on An Exit Rule as an Exit Strategy for Monetary Policy

The Macroeconomics of Education

The new study by my colleague Rick Hanushek and his coauthor Ludger Woessmann shows that bringing US education levels up to the level of Finland would raise real GDP by over $100 trillion measured in present discounted value terms over the next 80 years. Here is the chart from their paper with billions of US dollars on the vertical axis. Even in these days of trillion dollar rescue packages and growing debt burden on our grandchildren, $100 trillion is a lot of income, and the comparison with Finland shows that it is feasible.

Posted in Regulatory Policy

Comments Off on The Macroeconomics of Education

One Year Later and More Evidence that the Stimulus is Not Working

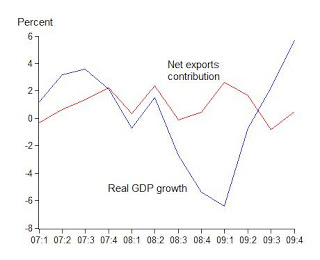

Friday’s data release from the Bureau of Economic Analysis (BEA) shows that real GDP growth rebounded to 5.7 percent in the fourth quarter from 2.2 percent in the third quarter of last year. The rebound was sharper when compared with the -6.4 percent decline in the first quarter and -0.7 percent decline in the second quarter.

How much of the rebound was due to the “stimulus package” passed in February of last year? I have shown in a previous post that the increased transfer payments to individuals and temporary tax rebates had virtually no impact in jump-starting consumption. But what about the increase in government purchases in the stimulus package? A look at the details in the GDP report of Friday shows that changes in government purchases have had virtually no effect. The turn-around in growth has been mainly due to private investment. Four simple graphs illustrate this.

Recall that GDP is the sum of Consumption plus Investment plus Net Exports plus Government Purchases. Thus the growth of GDP can be decomposed into contributions due to each of these four components. Table 2 of the BEA data release reports these contributions, and I summarize them in the four charts. In each chart the blue line shows the growth rate of real GDP from the start of the recession. You can clearly see the decline in growth in the recession and then the start of the rebound. In the first chart the red line shows the contribution from investment. It explains most of the recession and the rebound.  In the next chart you see the contribution of consumption, which plays a noticeable but considerably smaller role.

In the next chart you see the contribution of consumption, which plays a noticeable but considerably smaller role.  The third chart shows the contribution of net exports, which explains some of the smaller movements in early 2008.

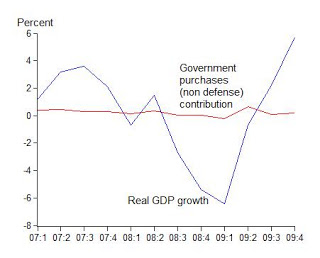

The third chart shows the contribution of net exports, which explains some of the smaller movements in early 2008.  The fourth chart shows the contribution of government purchases. I have focused on non-defense federal plus state and local purchases because defense spending was not part of the stimulus (adding in defense does not change the story). Note that none of the action in real GDP growth is due to government purchases.

The fourth chart shows the contribution of government purchases. I have focused on non-defense federal plus state and local purchases because defense spending was not part of the stimulus (adding in defense does not change the story). Note that none of the action in real GDP growth is due to government purchases.  In other words during the entire first year of the stimulus package, the contribution of government purchases to change in real GDP growth is virtually nil. There is no evidence here that the stimulus has worked either to raise GDP growth or to create jobs.

In other words during the entire first year of the stimulus package, the contribution of government purchases to change in real GDP growth is virtually nil. There is no evidence here that the stimulus has worked either to raise GDP growth or to create jobs.

Posted in Stimulus Impact

Comments Off on One Year Later and More Evidence that the Stimulus is Not Working

Music Videos on Boom and Bust

John Papola and Russ Roberts just put their Hayek versus Keynes rap video on youtube. It’s called “Fear the Boom and Bust.” But also go to their web page EconStories which has much more.

Also today PBS NewsHour aired a new Paul Solman video Unmasking Interest Rates: Honky-Tonk Style, which features Merle Hazard singing “Inflation or Deflation” along with me teaching Stanford Economics 1 students about monetary policy rules and the danger of keeping interest rates too low for too long.

Observe that the theme of both videos is that very low interest rates are a source of booms and busts.

Posted in Teaching Economics

Comments Off on Music Videos on Boom and Bust

Opinions versus Facts About the Chicago School

New Yorker writer John Cassidy argues in a recent article that free market-oriented Chicago school thinking was largely responsible for the financial crisis, and that, for this reason, interventionist-oriented Keynesian thinking has rightly replaced Chicago, which had previously “greatly influenced policy making in the United States.”

Cassidy makes his case mainly through a star witness, Judge Richard Posner, who Cassidy says “has shocked the Chicago School by joining the Keynesian revival.” Cassidy also reports the views of other University of Chicago economists about the Chicago School and its influence, but he dismisses many of them out of hand, especially John Cochrane and Gene Fama, who he calls “true believers” or “in the denial camp.” To his credit, Cassidy posted his interviews with these other economists on his blog. Nevertheless, relying on the interpretations of opinions of Posner or anyone else is an inherently subjective way to characterize a school of thought or to measure the extent of its influence on policy making.

Are there more objective, perhaps quantitative, ways? Consider, for example, measuring influence by the representation of members of a school in top economic positions in government where there is an opportunity to influence policy. And consider as a measure of an economist’s school, the university where he or she received the PhD. The data in the chart follows this approach. It shows the university PhD percentages of appointees to the President’s Council of Economics Advisers (CEA).

The blue line shows the percentage of presidential appointees to the CEA who have a PhD from Chicago. The red line shows the same for MIT or Harvard (Cambridge), one possible definition of an alternative to the Chicago school. The years from the creation of the CEA in 1946 until 1980 are shown along with each presidential term thereafter. Observe that the peak of the Chicago school influence was in the Reagan administration; it then dropped off markedly. In contrast Cambridge reached a low point of zero appointees to the CEA during the Reagan administration and then rose slightly to 20 percent in Bush 41, to 82 percent in Clinton, and to 100 percent in both Bush 43 and in Obama.

Blaming the financial crisis on the free-market influence of the Chicago school is certainly not consistent with these data. There were no Chicago PhDs on the President’s CEA leading up to or during the financial crisis. In contrast there was a great influx and then dominance of PhDs from Cambridge. And also notice that there were plenty of Chicago PhDs on the CEA at the time of the start of the Great Moderation—20 plus years of excellent economic performance. These data are more consistent with the view that the waning of the free-market Chicago school and the rise of interventionist alternatives was largely responsible for the crisis. But the main point is that there is no evidence here for blaming the influence of Chicago.

Of course, such measures are imperfect. Neither Milton Friedman nor Paul Samuelson served on the CEA, but their students did. And while PhDs from any insitution certainly do not fit in any one mold, the people who learned about rules versus discretion with Friedman likely had a different policy approach than people who learned about rules versus discretion with Samuelson. The data are robust when you look beyond the CEA to other top posts normally held by PhD economists. All assistant secretaries of Treasury for Economic Policy appointed during the Bush 43 and Obama Administrations had PhDs from Harvard. During the same period, all chief economists appointed to the IMF had PhDs from MIT, and, except for Don Kohn, who was promoted from within and Susan Bies who was appointed as a banker, all PhD economists appointed to the Federal Reserve Board were from Cambridge MA.

Posted in Teaching Economics

Comments Off on Opinions versus Facts About the Chicago School

The GAO Audit of the Fed’s AIG Bailout: Toward Increased Transparency?

Today’s letter from Ben Bernanke to the GAO stating that the Fed would “welcome a full review by GAO of all aspects of our involvement in the extension of credit to AIG” is a step in the right direction. Importantly, the letter also indicates that the Fed “will make available to the GAO all records and personnel necessary to conduct the review.”

A key set of records, which should be made available publicly, are the minutes of the Federal Reserve Board meeting, or meetings, where the decision to bailout AIG was made, along with the Board staff analysis relating to that decision. A full review would also require release of information (perhaps minutes from other Board meetings) where the decision not to extend credit for Lehman was made–a decision made just two days before. According to press accounts, and to Sorkin’s book Too Big Too Fail, the AIG bailout was recommended to the Board by Timothy Geithner, who was then president of the New York Fed, but who was not, of course, a member of the Board. There is now much debate and conflicting testimony about the nature and even the existence of the systemic risk which is currently cited as a factor in the Board’s decision.

In keeping with the spirit of letter sent today, there is no reason why the Board should not regularly release detailed minutes of such crucial meetings just as the Federal Open Market Committee does. Currently, the only minutes available for those Board meetings that involved the “unusual and exigent circumstances” clause were for the March 14, 2008 and March 16, 2008 meetings, which related to Bear Stearns. The Board released these on June 27, 2008, three months after the meetings took place, but it has not released minutes from the Board meeting on AIG or related meetings of more than a year ago.

There is a stark contrast between the relatively high degree of transparency of FOMC decisions and the lack of transparency of Board decisions. To see this, compare the most recent FOMC minutes with the Board minutes of March 2008 cited here, or with no minutes at all. Increasing the transparency of the Board meetings to the level of the FOMC meetings would improve public discourse on these important decisions.

Posted in Financial Crisis

Comments Off on The GAO Audit of the Fed’s AIG Bailout: Toward Increased Transparency?

More on “Too Low For Too Long”

Much continues to be written this week about whether interest rates were too low for too long in the period 2003-2005 . David Papell posted a useful guest analysis on Econbrowser this morning showing that the target federal funds interest rate was too low in 2003-2005 when you use the overall GDP price measure of inflation in the Taylor rule; he also shows that the target interest rate would not have increased in 2008 as Ben Bernanke argued in his Atlanta speech.

In Bernanke Challenged on Rates’ Role in Bust, Jon Hilsenrath reports results in the Wall Street Journal that show that 70 percent of economists of an informal survey agreed that “Excessively easy monetary policy by the Federal Reserve in the first part of the decade helped cause a bubble in house prices” (78 percent of business economists).

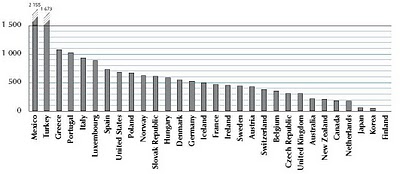

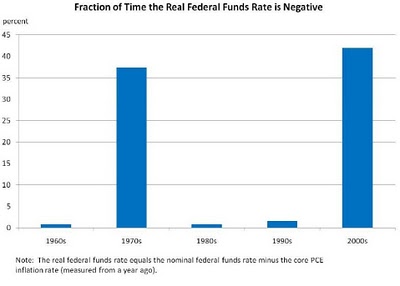

I was interviewed today on CNBC’s Kudlow Report about my Wall Street Journal reply to Ben Bernanke. Among other things Larry Kudlow asked about Thomas Hoenig’s calculation that real interest rates were below zero in the past decade for about as much time as they were in the turbulent 1970s. This bar chart from Thomas Hoenig’s January 7 speech gives the details which are very striking.

Also some asked about the specific reference to the finding of Athanasios Orphanides and Volker Wieland that interest rate were too low for too long if you use private sector forecasts of inflation rather than the Fed’s forecasts in the Taylor rule. Here is the link to the July/August 2008 Review of the St. Louis Fed, the same issue where the Jarocinski-Smets piece mentioned in my Wall Street Journal article appeared.

Also some asked about the specific reference to the finding of Athanasios Orphanides and Volker Wieland that interest rate were too low for too long if you use private sector forecasts of inflation rather than the Fed’s forecasts in the Taylor rule. Here is the link to the July/August 2008 Review of the St. Louis Fed, the same issue where the Jarocinski-Smets piece mentioned in my Wall Street Journal article appeared.

Posted in Monetary Policy

Comments Off on More on “Too Low For Too Long”

From Fiscal Stimulus and Fiscal Anti-Stimulus

In an interesting new paper, University of Chicago economists Thorsten Drautzburg and Harald Uhlig calculate the impact the $787 billion fiscal stimulus package passed last year. Previous research, such as the paper by John Cogan, Tobias Cwik, Volker Wieland and me (CCTW), assumed that the higher taxes needed to pay interest on the increased debt caused by the bigger deficits were of the lump-sum variety with no distortions. Drautzburg and Uhlig more realistically assume that future marginal tax rates must rise. Because higher marginal tax rates reduce supply, they find that “the output loss in the medium-to-long term is substantially larger than in the lump-sum tax version” of CCTW. The results are illustrated in Figure 2 of the Drautzburg-Uhlig paper which shows that the longer-term losses outstrip any shorter-term gains very quickly. The paper is one of several technical papers presented at the conference “New Approaches to Fiscal Policy” at the Federal Reserve Bank of Atlanta last week

Posted in Stimulus Impact

Comments Off on From Fiscal Stimulus and Fiscal Anti-Stimulus