Much continues to be written this week about whether interest rates were too low for too long in the period 2003-2005 . David Papell posted a useful guest analysis on Econbrowser this morning showing that the target federal funds interest rate was too low in 2003-2005 when you use the overall GDP price measure of inflation in the Taylor rule; he also shows that the target interest rate would not have increased in 2008 as Ben Bernanke argued in his Atlanta speech.

In Bernanke Challenged on Rates’ Role in Bust, Jon Hilsenrath reports results in the Wall Street Journal that show that 70 percent of economists of an informal survey agreed that “Excessively easy monetary policy by the Federal Reserve in the first part of the decade helped cause a bubble in house prices” (78 percent of business economists).

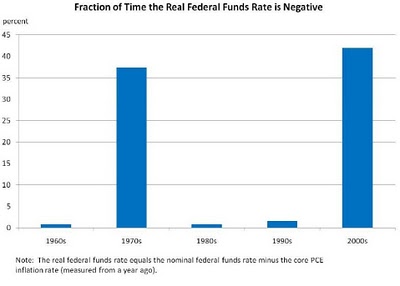

I was interviewed today on CNBC’s Kudlow Report about my Wall Street Journal reply to Ben Bernanke. Among other things Larry Kudlow asked about Thomas Hoenig’s calculation that real interest rates were below zero in the past decade for about as much time as they were in the turbulent 1970s. This bar chart from Thomas Hoenig’s January 7 speech gives the details which are very striking.

Also some asked about the specific reference to the finding of Athanasios Orphanides and Volker Wieland that interest rate were too low for too long if you use private sector forecasts of inflation rather than the Fed’s forecasts in the Taylor rule. Here is the link to the July/August 2008 Review of the St. Louis Fed, the same issue where the Jarocinski-Smets piece mentioned in my Wall Street Journal article appeared.

Also some asked about the specific reference to the finding of Athanasios Orphanides and Volker Wieland that interest rate were too low for too long if you use private sector forecasts of inflation rather than the Fed’s forecasts in the Taylor rule. Here is the link to the July/August 2008 Review of the St. Louis Fed, the same issue where the Jarocinski-Smets piece mentioned in my Wall Street Journal article appeared.