People often ask me what it’s like to teach both introductory economics courses and Ph.D. level economics courses in the same academic year, which I have done regularly for many years at Stanford including this year. The courses are at extreme ends of the educational spectrum, and there are several obvious differences.

First is the math. My Ph.D. course is loaded with math—multivariate stochastic processes, differential and difference equations, inter-temporal optimization, vector auto-regressions. It is not unusual to fill several slides or blackboards with equations. Here is what you would see if you walked into my Ph.D. lecture on risk and rates of return on bonds.

In contrast my introductory course has virtually no math beyond high school algebra. The emphasis is on economic intuition, reasoning, applications, and I mainly use graphs. Here is what you would see if you walked into my introductory lecture on risk and rates of return on bonds.

People are always surprised by the amount of math used in teaching economics in graduate school, and some think it is used too much. In an interview with Milton Friedman I published several years ago, he said “I go back to what Alfred Marshall said about economics: Translate your results into English and then burn the mathematics. I think there’s too much emphasis on mathematics as such and not on mathematics as a tool in understanding economic relationships.” While I agree about the need to explain the mathematical results in simple terms, I do not agree about burning the math once translated. Mathematical methods are now used in practice in economics and finance in both the public and private sector, from auctioning the spectrum to matching medical students and residence programs. People need to have an intuitive understanding of the methods, but you also need the math (and the computer programs) to make them work.

A second difference between the introductory course and the Ph.D. course, which you would notice right away if you walked in, is the greater emphasis on entertainment (I call it surprise-side economics) in the former. This is in part because the introductory course is much larger—100s of students compared to about 25 in Ph.D. classes, but also because the Ph.D. students have already decided to become professional economists, and are usually happy to focus on the details of the subject without a constant reminder of the motivating factors.

The most interesting difference between the courses in my view is how you simplify the more complex ideas for beginning students. One of the great teachers who taught at both levels—though in physics rather than economics, Nobel Prize winner Richard Feynman wrote this about teaching at the introductory level: “Now, what should we teach first? Should we teach the correct but unfamiliar law with its strange and difficult conceptual ideas, for example the theory of relativity, four-dimensional time-space, and so on? Or should we first teach the simple “constant-mass” law, which is only approximate, but does not involve such difficult ideas? The first is more exciting, more wonderful, and more fun, but the second is easier to get at first, and is a first step to a real understanding…. This point arises again and again in teaching physics.”

It also arises again and again in teaching economics. Some ideas—like auction theory or mechanism design for matching—probably have to wait to more advanced courses. But in my view it is possible to teach many other amazing economic ideas rigorously at the intro level—for example, the efficiency of competitive markets or how a central bank controls the interbank rate—and thus give beginning students an understanding of the “more exciting, more wonderful, and more fun” parts of economics.

Which course do I enjoy teaching more? Both are challenging and rewarding, though in different ways. Not to dodge the question, but the truth is I enjoy both.

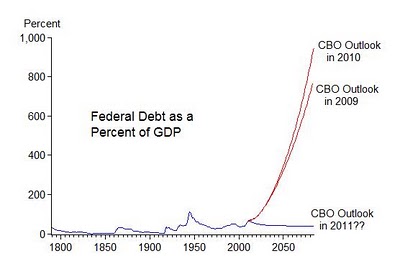

Like the fireworks tonight, you can see one explosion after another, and one higher than the one before. But unlike the fireworks tonight, these are not the kind of explosions you want to see.

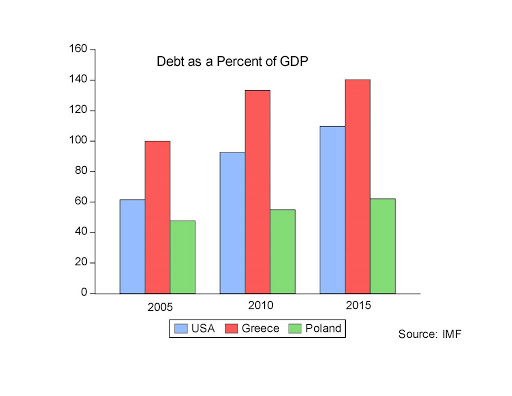

Like the fireworks tonight, you can see one explosion after another, and one higher than the one before. But unlike the fireworks tonight, these are not the kind of explosions you want to see.  Poland is the only country in the European Union which did not have a recession during 2009, as shown in this chart. And among all the OECD countries, Poland had the best real growth performance in 2009. I visited Poland this past week to give some talks and to better understand Poland’s resiliency. One particularly enjoyable talk was joint with Leszek Balcerowicz the former central bank governor and finance minister who deserves much of the credit for transforming Poland’s economy from central planning to a market economy back in 1989.

Poland is the only country in the European Union which did not have a recession during 2009, as shown in this chart. And among all the OECD countries, Poland had the best real growth performance in 2009. I visited Poland this past week to give some talks and to better understand Poland’s resiliency. One particularly enjoyable talk was joint with Leszek Balcerowicz the former central bank governor and finance minister who deserves much of the credit for transforming Poland’s economy from central planning to a market economy back in 1989.

{kind=link}

{kind=link}