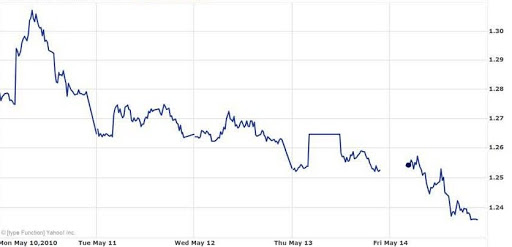

In a column Central Banks are Losing Credibility published in the Financial Times last Tuesday, just after the announcement of the European rescue plan, I noted that the euro’s quick set-back hours after its initial boost was a harbinger of negative consequences. The euro’s continued decline throughout last week (see chart) shows that this set-back was not only a harbinger, but also the first in sequence of negative market reactions. Much commentary during the week supports this view.

Harald Uhlig, in an article “Die Trichetisierung des Euro” in Handelsblatt on Wednesday, raises more credibility concerns about the ECB as does Simon Nixon, in his Friday Wall Street Journal article “Central Banks, Politics Don’t Mix” (adding criticism of the Bank of England’s endorsement of the new British government’s budget plan). Yesterday Mohamed El-Erian warns in an FT.com guest post of the possibility that governments will “do more of the same” and that the US will “press Europe to do more of the same” which is a real concern. Recall that when it was clear that the 787 billion dollar stimulus package passed in the United States in February 2009 was not helping the recovery, some argued that it was not big enough, and they may be soon arguing that the near 750 billion euro package is not big enough. Indeed, that might have been an argument heard on the G7 finance ministers conference call late last week.

But the evidence is that a larger package could easily make things worse. As we learned in the U.S. financial crisis starting in August 2007, more liquidity will not solve a basic solvency problem. As Mohamed El-Erian points out “it is not easy to change track,” but last week reminds us how important it is to at least start getting back on track, the title of my article in the current issue of the St. Louis Fed Review.