At yesterday’s hearing before the Senate Banking Committee, Fed Chairman Ben Bernanke talked about monetary policy rules in response to a series of questions by Senator Pat Toomey. First, the Chairman stated that the Taylor Rule calls for interest rates “way below zero” and that this justifies methods such as quantitative easing. This is puzzling because I have reported for months that the Taylor Rule (see 1993 paper) does not call for an interest rate below zero. Second, when Senator Toomey then asked if Taylor believed the Taylor Rule called for rates below zero, Chairman Bernanke didn’t answer directly, but instead claimed that in 1999 I preferred a different rule to the one I published in 1993; he then said that the 1999 rule gives a much different rate. Senator Toomey then pressed on and specifically said the Taylor Rule called for rates higher than we have now, at which point Chairman Bernanke changed tack and argued that there were other policy rules that call for below-zero interest rates. Here is the relevant part of the transcript.

MR. BERNANKE: … The Taylor Rule suggests that we should be, in some sense, way below zero in our interest rate, and therefore we need some method other than just normal interest rate changes to —

SEN. TOOMEY: Do you know if Mr. Taylor believes that?

MR. BERNANKE: Well, there are different versions of the Taylor Rule, and there’s no particular reason to pick the one that he picked in 1993. In fact, he preferred a different one in 1999 which, if you use that one, gives you a much different answer.

SEN. TOOMEY: My understanding is that his view of his own rule is that it would call for a higher Fed funds rate than what we have now.

MR. BERNANKE: There are, again, many ways of looking at that rule, and I think that ones that look at history, ones that are justified by modeling analysis, many of them suggest that we should be well below zero. And I just would disagree that that’s the only way to look at it.

But anyway, so I think there are some — there is some basis for doing that.

There are several issues raised by this back-and-forth exchange.

Most important, at least from my perspective, is that contrary to what was claimed in the hearing, I did not say that I preferred a different policy rule in 1999 rather than the rule I originally published in 1993. I am not sure where this idea of my preferring another rule came from; I went back and looked at the academic papers I published in 1999 (here is a list); the paper on this list that Chairman Bernanke may have been referring to is A Historical Analysis of Monetary Policy Rules where I looked at two different policy rules during different periods of U.S. history. However, as I said in that paper (page 325), one rule was the “policy rule I suggested” and the other one was what “others have suggested.” The “others” were people at the Federal Reserve so for completeness I included that rule in the historical comparison. I did not propose or prefer an alternative rule in that 1999 paper, and it is hard to see how one could interpret the paper that way. This is not just a matter of academic niceties and citations; it is important to correct the record because the “others have suggested” rule has a much larger coefficient on the GDP gap and is therefore more likely to generate negative interest rates and be used to rationalize discretionary actions such as quantitative easing.

Second, the exchange between Chairman Bernanke and Senator Toomey suggests that the Fed is unclear about what monetary policy strategy it is using for the interest rate. Is it the Taylor Rule, as in the first response? Is it the rule incorrectly attributed to me in 1999, as in the second response? Is it some estimated rule, as in the third response? Or is it something else? It would be useful to know what the strategy is. Greater transparency about the strategy would add greatly to predictability and would help markets understand whether quantitative easing will be extended or when the interest rate will break out of the 0-.25 percent range.

For example if the strategy was reasonably well described by the Taylor Rule the interest rate would equal about 1.5 times the inflation rate plus .5 times the GDP gap plus 1. The most recent quarterly data (through the 4th quarter of 2010, released by Bureau of Economic Analysis on February 25, 2011) show that the inflation rate is about 1.4 percent (change in GDP deflator over the last four quarters). According to the average of the most recent survey by the Federal Reserve Bank of San Francisco, (January 28, 2011, Williams-Weidner) the GDP gap is about 4.4 percent. This implies an interest rate of 1.5 X1.4 + .5X(-4.4) + 1 = 2.1 + -2.2 +1 = 0.9 percent, or about 1 percent, which suggests that the Fed should be raising the rate sometime soon, perhaps before the end of this year. But if it is one of the other rules mentioned by the Chairman we might have to wait longer.

Third, the exchange shows how it would be quite feasible and useful to restore some of the reporting and accountability requirements which were removed from the Federal Reserve Act in 2000. As I have proposed, with such requirements the Fed would establish and report to Congress its strategy or policy rule for monetary decision making. If it later deviated from that strategy it would have to provide an explanation to Congress in writing and at a public congressional hearing. With such a reporting requirement, the testimony at such a hearing would be like this exchange between Chairman Bernanke and Senator Toomey with the very important exception that the Congress and the American people would have some idea of what the Fed’s basic strategy was.

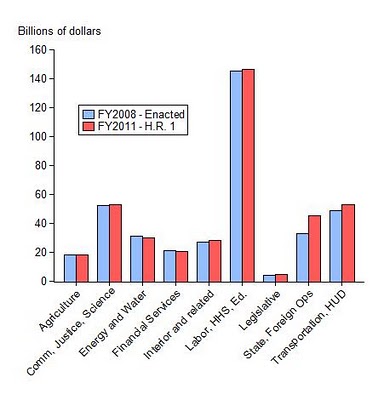

The second chart divides the appropriated spending into nine budget categories (other than defense, homeland security, and military construction). The chart shows how close the 2011 proposal is to 2008 for each category, with some higher and others lower. Of course there will be understandable disagreement between Republicans and Democrats about the composition of spending between and within these budget categories, and this will be a reasonable subject for debate with the Senate and the President. But I think these data show that a reasonable compromise would be to keep the overall totals as in the House proposal and thus take a first important step toward restoring fiscal sanity.

The second chart divides the appropriated spending into nine budget categories (other than defense, homeland security, and military construction). The chart shows how close the 2011 proposal is to 2008 for each category, with some higher and others lower. Of course there will be understandable disagreement between Republicans and Democrats about the composition of spending between and within these budget categories, and this will be a reasonable subject for debate with the Senate and the President. But I think these data show that a reasonable compromise would be to keep the overall totals as in the House proposal and thus take a first important step toward restoring fiscal sanity.

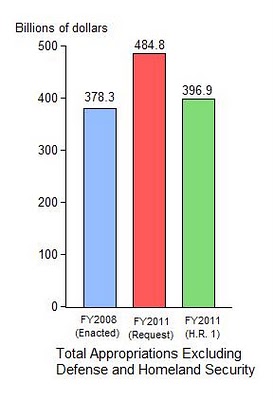

But a very important question going forward is what will be the base for discussing budget proposals in 2012. If one keeps to the logic of the House leadership, then the base to reduce from should be $485B, not $537B, as shown by the dashed line. To complete the reversal of the spending binge, 2012 spending would be brought down to 2007 levels of $459B, which would be a 5 percent reduction from the appropriate 2011 base.

But a very important question going forward is what will be the base for discussing budget proposals in 2012. If one keeps to the logic of the House leadership, then the base to reduce from should be $485B, not $537B, as shown by the dashed line. To complete the reversal of the spending binge, 2012 spending would be brought down to 2007 levels of $459B, which would be a 5 percent reduction from the appropriate 2011 base.