The Atlanta Fed, through its “macroblog,” has joined the discussion about reform of the Federal Reserve. It’s a good discussion to have. David Altig, Senior Vice President of the Federal Reserve Bank of Atlanta and main blogger, wrote the latest entry on my Wall Street Journal article of last week which offered proposals to return to sound fiscal and sound monetary policy. Macroblog has no quarrel with the proposals for sound fiscal policy but, as in past posts, disagrees with the analysis of monetary policy.

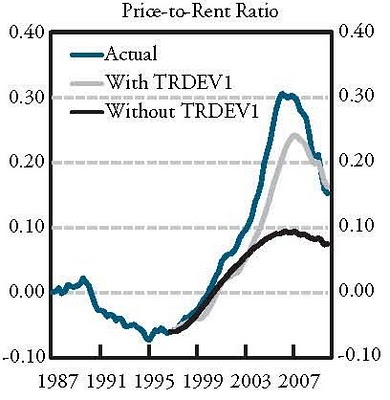

The latest macroblog entry starts by appealing to a paper from New Zealand which shows that an “estimated” Taylor rule indicates that interest rates were not too low for too long in 2003-05 as I have argued. But the “estimated” policy rule in that paper doesn’t looks anything like what I proposed and given that there are already scores of existing models I fail to see the advantages of another model from New Zealand. For example, at the Federal Reserve Bank of Kansas City, George Kahn shows that deviations from a policy rule were a major reason for the housing price boom and bust. A chart from his paper which I copy below shows clearly that policy without the Taylor Rule deviation (TRDEV1) would have avoided the boom and bust.

The Atlanta Fed’s macroblog post also argues that the Fed has already laid out an exit strategy for reducing its balance sheet, and it gives a link to minutes of the FOMC with a list of tools. However, as I explained in testimony to Congress last year, a list of tools is not a strategy. A strategy is a path or contingency plan for the balance sheet over time. I gave an example in the tesimony. If it is good to lay out a path to reduce the federal debt as a share of GDP, then why not lay out a contingency path to reduce the Fed’s balance sheet?

Regarding my proposals to restore the Fed’s reporting and accountability requirements removed in 2000, I think macroblog post’s reference to Ben Bernanke’s speech at the American Economic Association last January supports my point rather than refutes it. If there had been such reporting requirements in place in 2003-05, then the Fed would have been required to report the strategy at the time in Congress, not 7 years later at the AEA. Also if you look back at the FOMC transcripts at the time you will see that the Fed was intentionally holding rates extra low for an “extended period” and only increasing them at “measured pace,” which does not seem consistent with policy as usual. In my view if the Fed had laid out its strategy at the time, then there would have been a more informed public discussion.

Then there is the question of the Fed’s multiple mandate. The record shows that explicit mention of the term “maximum employment” entered the FOMC Statement for the first time only last fall, after more than thirty years of no such mention since the mandate was put into legislation way back in 1977. So the connection between the mandate and QE2 seems most evident based on the record. In my view, the rate of inflation and the level of GDP last year justified an interest rate near zero, but not QE2. The Atlanta Fed macroblog post argues that QE2 was effective. But any connection between QE2 and its purported effects is tenuous when long-term Treasury securities, which the Fed has been purchasing, have declined in price, gone in the wrong direction.

The recent post by David Altig ends by referring to the Financial Crisis Inquiry Commission, which seems to have chosen a “perfect storm” explanation of the crisis where everyone shares some blame. In that report, the Fed shares blame, but mainly because of a failure to enforce existing regulations. The debate over interest rates seems to have ended in a draw in the Commission with short reviews of arguments made by Ben Bernanke, Alan Greenspan, and me. The conclusion of the minority that U.S. monetary policy may have contributed to the credit bubble is about as far as one could expect from such a commission and should be enough incentive to look for policy reforms to improve monetary policy in the future.