Some skeptics have complained about the 5% national economic growth target put forth by former Minnesota Governor Tim Pawlenty in his speech this week about his economic plan. They say it can’t be done. But I think the goal makes a great deal of sense. It would focus policymakers like a laser beam on the great benefits that come from higher growth and on the pro-growth policies needed to achieve it. As with any goal, if you take it seriously, you’ll choose policies that work toward that goal and reject those that don’t.

As stated in the speech, “5% growth is not some pie-in-the-sky number.” One way to see why is by dissecting the number into its two parts using basic economics. As we teach in Economics 1, economic growth equals employment growth plus productivity growth. Productivity is the amount of goods and services that workers produce on average in a given period of time. Thus, higher economic growth can come from higher employment growth or from higher productivity growth. Now consider some examples of average growth rates over the next ten years.

First, look at employment growth. Given the dismal jobs situation, that’s the highest priority. Currently the percentage of the working-age population (age 16 and over) that is actually working is very low at 58.4 percent. In the year 2000 it reached 64.7 percent, so that is at least a feasible number. Raising the employment-to-population ratio to 64.7 means an employment increase of 10.8 percent (64.7-58.4/58.4 = .108) or about 1 percent per year over 10 years, even without any growth of the population. Adding in about 1 percent for population growth (from Census projections), gives employment growth of 2 percent per year.

Now consider productivity growth. Since the productivity resurgence began around 1996, productivity growth in the United States has averaged 2.7 percent according to the Bureau of Labor Statistics. So numbers in that range are not pie in the sky. As Harvard economist Dale Jorgenson and his colleagues have shown, the IT revolution is part of the explanation for the productivity growth, and, if not stifled, is likely to continue, as is pretty clear to me as I sit a few hundred yards from Facebook and other high-tech firms.

Now if we add the 2.7 percent productivity growth to the 2 percent employment growth, we get 4.7 percent economic growth, which is within reaching distance of—or simply rounds up to—the 5 percent target set by Governor Pawlenty. Thus, five percent growth is a good goal to aspire to, whereas 3 or 4 percent would be too little and 6 or 7 percent too much. Of course, one can fine-tune these calculations–for example, by estimating changes in hours per worker or the difference between nonfarm business (which BLS productivity numbers refer to) and total GDP–or raise questions about demographic effects on the employment-to-population ratio. And one could use different examples, perhaps lower employment growth and higher productivity growth, but the basic point about the goal would be the same.

You can see how the types of pro-growth policies in the Pawlenty plan would work toward the goal by reducing spending growth enough to balance the budget without tax increases and thereby remove threats of a debt crisis; by lowering marginal tax rates to spur hiring and job growth; by scaling back unnecessary new regulations which impede private investment and higher productivity, and by restoring sound monetary policy to remove uncertainty about inflation or another financial crisis.

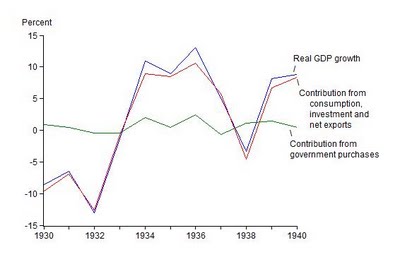

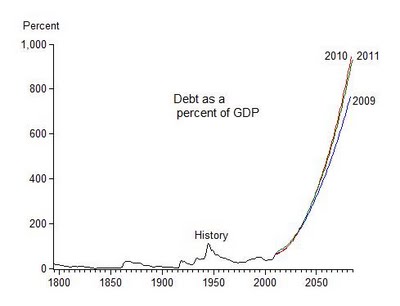

This means that the backdrop used two years ago by the “

This means that the backdrop used two years ago by the “ Today the Joint Economic Committee of the Congress held a hearing on whether a credible plan to reduce government spending growth would bolster or hinder the recovery. I argued that a credible budget strategy would strengthen the recovery, by removing the threats of another fiscal crisis, higher taxes, higher inflation and higher interest rates—all caused by the huge deficits and growing debt and all impediments to private investment and job creation (written testimony

Today the Joint Economic Committee of the Congress held a hearing on whether a credible plan to reduce government spending growth would bolster or hinder the recovery. I argued that a credible budget strategy would strengthen the recovery, by removing the threats of another fiscal crisis, higher taxes, higher inflation and higher interest rates—all caused by the huge deficits and growing debt and all impediments to private investment and job creation (written testimony