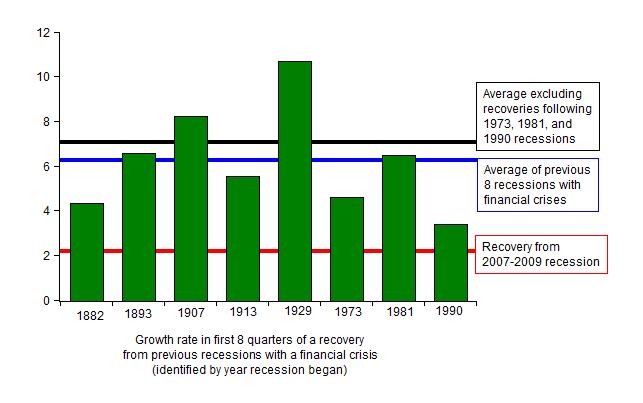

As the presidential election campaign reaches its final crucial hours, the main issue remains the economy—unemployment, jobs, growth—and what the economic policy can do about it. Campaigning in Ohio and other swing states, President Obama says his policies have meant “real progress” and wants to stick with them, while Governor Romney says they have meant “stagnation” and wants to change them. If you have been monitoring this blog since it started three plus years ago—long before the political season began—you probably know that my view is that it’s “stagnation,” not “real progress,” and that policy is the problem.

The High Unemployment is a Tragedy

This “stagnation versus real progress” debate came up in several TV shows I did on Friday, and in each case the networks chose headlines that reflect my view well:

Our Unemployment Number is a Tragedy, Bloomberg TV

(30 second video pull quote) Unemployment a Tragedy, We Can Do Better

We Could Be Doing Better, CNN

Slow Growth Is Biggest Economic Challenge Facing Incoming President, (paired up with Austan Goolsbee), PBS NewsHour

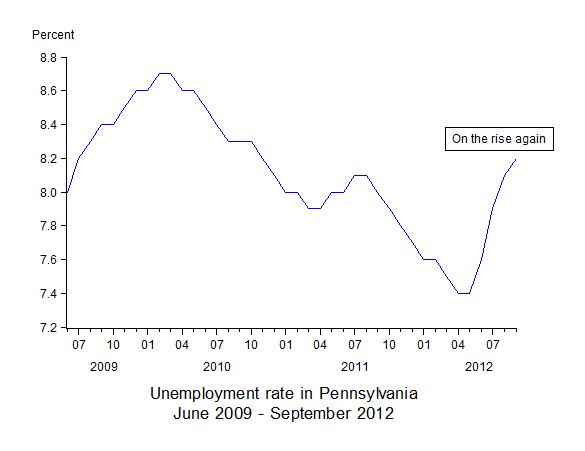

Jeffrey Brown was the interviewer on Newshour and asked at the opening: “What is the problem that most needs to be addressed by whoever is the next president?” I answered: “That unemployment rate. It’s too high. It shouldn’t be this high. And it has increased a bit. But it’s increased even more in states like — I think Pennsylvania went up from 7.4 to 8.2 over the last few months. And the reason is the weak economy. We shouldn’t be growing this slowly. We have an economy which can do much better. It’s done better in similar periods in the past. And with the right policies, it can do much better, get the unemployment down much further. And there’s also people dropping out of the labor force. You know, in Ohio, since the recovery began, 194,000 people just dropped out of the labor force, stopped looking for work. That’s another bad sign that I think people should be very concerned about. It’s really depressing what’s happening with respect to the labor market right now in this country.”

In my view, it’s also a concern that some people have begun talking as if the unemployment problem does not exist. I know this is hard to believe, but if you search, for example, the 20 page glossy brochure on the economy recently distributed by the Administration, you will not find the word “unemployment.” If one does not discuss a problem—its magnitude, its causes—how is one ever going to fix it?

Now consider what is happening in the Swing States

Ohio

Yesterday, The New York Times argued that “Mr. Obama was right when he talked about ‘real progress’ in the economy during a campaign swing in Ohio, where the state unemployment rate has declined from 8.6 percent a year ago to 7 percent recently.”

But the Times skips over the reason why unemployment fell in Ohio, and it’s “stagnation,” not real progress: Virtually all of the decrease in unemployment in Ohio has been caused by unemployed people dropping out of the labor force—discouraged not to find a job after many months of search. There has been virtually no increase in the number of jobs during the recovery. Worse, 33,000 jobs have been lost in the past four months.

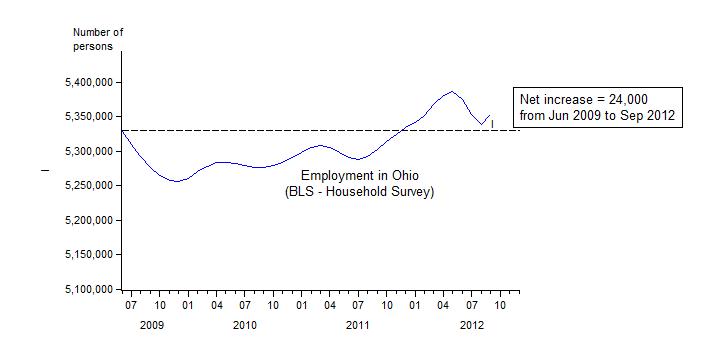

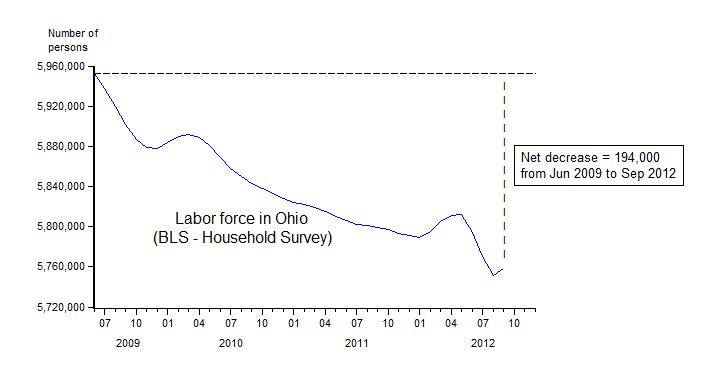

By the official definition of the Bureau of Labor Statistics, unemployment in Ohio fell by 218,000 persons since the national recession ended and so-called recovery began in June 2009. But the vast amount of the decrease in unemployed was due to 194,000 persons leaving the labor force. There were only 24,000 additional jobs. In other words, 9 of 10 workers who had been counted as unemployed are no longer counted as unemployed simply because they are no longer looking for work. Were it not for this decline in the labor force, the unemployment rate would be around 10% rather than the 7% mentioned by the Times.

The two charts below tell the tragic story: With few jobs, people are dropping out of the labor force and are no longer even looking for work. Here is a picture of how employment has actually declined in Ohio.

Iowa

In an oped in the Cedar Rapids Gazette today, Tad Lipsky and I wrote about why there was employment stagnation in Iowa, and even worse than in Ohio. The chart below shows that employment is actually lower than at the start of the recovery or the day the Obama Administration began.

Colorado, New Hampshire, and Wisconsin

The recent employment drop off in Ohio and Iowa is also occurring in Colorado, New Hampshire, and Wisconsin. In Colorado, the number of people employed has fallen by over 17,000 since March. In New Hampshire, the number of people employed has fallen by nearly 8,000 since April. And in Wisconsin, the number of people employed has fallen by over 30,000 since May.

Pennsylvania

This post is already too long. I conclude with chart of the unemployment rate in Pennsylvania which speaks for itself.