A beautiful book, edited by Robert King and Alexander Wolman, https://www.richmondfed.org/-/media/RichmondFedOrg/publications/research/goodfriend/essays_marvin_goodfriend.pdf with original essays in tribute by Alfred Broaddus Jr., Donald Kohn, William Poole, Kartik Athreya and Stephen Williamson, Ben Bernanke, Michael Bordo and Edward Prescott, Douglas Diamond, Michael Dotsey, Andreas Hornstein, and Alexander Wolman, Huberto Ennis and John Weinberg, Vitor Gaspar and Frank Smets, Mark Gertler, Robert Hetzel, Athanasios Orphanides and John Williams, Charles Plosser, Sergio Rebelo and Pierre-Daniel Sarte, Thomas Sargent, Lars Svensson, John Taylor, Mark Watson, Michael Woodford, Robert King and Yang Lu

Essays in Honor of Marvin Goodfriend: Economist and Central Banker

Posted in Uncategorized

Leave a comment

Play By The Rules

Federal Reserve Chair Jerome Powell’s testimony at the House and Senate this week again had much to say about monetary policy rules. The focus on policy rules is encouraging, as it is a way to both get back on track and prevent further harmful deviations in the future, as was the focus of our recent May conference at Hoover and Stanford University

Consider for example the exchange at the Senate Committee on Banking. Housing and Urban Affairs between North Carolina Senator Thom Tillis, the acting ranking member, and Chair Powel on Wednesday June 22.

According to the written record of his remarks, Senator Tillis https://www.banking.senate.gov/imo/media/doc/Tillis%20Opening%20Statement%206-22-22.pdf said in his opening that: “Regarding the Fed specifically – though I am pleased you have begun taking the drastic action necessary to right the U.S. economy – these actions are long-overdue and monetary policy remains too loose. CPI inflation now stands at 8.6% per year but the Fed funds rate sits at only 1.6%. According to the Fed’s semiannual report, the rate should be over 6% under the Taylor rule. This disparity indicates not only the lengths the Fed has yet to go to normalize monetary policy, but also the fact that the Fed has largely boxed itself into a menu of purely reactive policy measures. Unless the Fed works quickly to move away from their discretion-based monetary policy approach that has remained consistently well-behind the curve, I am concerned the Fed will lose its credibility to effectively manage the national economic situation.”

Then, at 55 minutes into the hearing according to a recorded videotape, Senator Tillis https://www.banking.senate.gov/hearings/watch?hearingid=DFA0BB5D-5056-A066-60E6-2BD668AE1552 said further that “By the Fed’s own analysis of various policy rules, including the Taylor Rule, the revised Taylor rule, the balanced approach rule, and the balanced approach short fall rule, rates should have begun to rise long before they did. According to the Fed’s own analysis of these rules, the fed funds rate should currently be above 6 percent; this is in the Report to Congress. Yet the rate currently stands at 1.6 percent. Likewise, the same rules could—should—have prompted the Fed to begin raising rates Q4 last year Q1 this year. I’m concerned that the Fed has opted out of rules-based to discretionary monetary policy. As the Fed reviews monetary policy strategy, Chair Powell, will you commit to considering an increased weight for rules based strategy for its decision making and if not why.”

Chair Powell answered: “We do use policy rules like the various forms of the Taylor rule in all of the analysis that we do. If you are thinking about how monetary policy will affect the economy, you have to have some sort of a rule like that. The Fed has never really used them in a prominent way to actually set policy in real time. But that is not to say that they do not shed light. We do consult them on an ongoing basis. The rules all called for a deeply, deeply, negative rates during the pandemic, and we didn’t do that. They did call of course for rates to move up, and rates now really are moving up much closer to where the Taylor rule—various form of the Taylor rule—are. And I think by the end of the year will be pretty close to where some of the Taylor rule iterations are. It is something we consider. I think in a couple of years when we look at our framework again, that’s something we could look at.”

Senator Tillis then responded: “Chair Powell could you just briefly explain the variance between rules-based decision making being at 6 and where we are today. What are the factors coming into play?”

Chair Powell answered: “Taylor rules don’t keep, they don’t take into consideration changes in financial conditions. They just look at the overnight policy rate. As I mentioned earlier, we began signaling, and we are set up now to signal policy changes going forward with the summary of economic projections that we do four times a year. So markets priced that in, and you are getting a lot of policy tightening well in advance of actually raising rates. As you pointed out we are 1.6 percent only on the federal funds rate, but look out the rate curve, all the…very substantial additional rate hikes are already priced in with financial conditions and they have been for several months. So that’s one way of thinking about it. It’s really only at the very short end of the curve where rates are still in negative territory from a real perspective. If you look farther out, real rates are positive right across the curve. That’s really what we are trying to achieve with policy. In a situation like this where we have forty year highs in inflation, and we know we need restrictive policy. And that is where we are headed.”

The press also covered the hearing. In an article called GOP to Powell: Play by the rules Kate Davidson of Politico wrote on June 23 https://www.politico.com/newsletters/morning-money/2022/06/23/gop-to-powell-play-by-the-rules-00041638 and said that

“We expected Republicans to press Federal Reserve Chair Jerome Powell on the need to tighten policy faster at his Senate hearing Wednesday. But we were struck by how they used the occasion to revive an old GOP talking point: the Fed has too much discretion.”

“Sen. Thom Tillis (R-N.C.), who sat in as the ranking Republican at the session, argued that the Fed should be bound by formalized rules in its interest rate decisions, our Victoria Guida wrote. And he pointed to a formula, named after Stanford economist John Taylor, suggesting that the central bank’s main policy rate should be much, much higher than it is.” “The Fed has largely boxed itself into a menu of purely reactive policy measures,” Tillis said. “Unless the Fed works quickly to move away from their discretion-based monetary policy approach that has remained consistently well behind the curve, I am concerned the Fed will lose its credibility to effectively manage the national economic situation.

And in an article Assessing Monetary Policy Through The Taylor Rule by Blu Putnam, Chief Economist, CME Group, said https://www.cmegroup.com/openmarkets/economics/2022/Assessing-Monetary-Policy-Through-The-Taylor-Rule.html : “In policy circles this trade-off is embodied in what is known as the Taylor Rule, which argues that the Fed should raise rates in line with a simple formula for an assumed inflation-jobs trade-off.… Of note, the Taylor Rule today, and for some time in the past, has been suggesting the Fed needs to start removing accommodation, which is what the Fed is now doing.”

And the discussion went global. Here as an article about the Bank of England entitled Bank of England’s Interest Rate Should be Closer to 10% says Swiss Re written by Gary Howes https://www.poundsterlinglive.com/economics/17147-bank-of-england-s-interest-rate-should-be-closer-to-10-says-swiss-re “The most significant central bank tightening cycle in decades has begun and we expect much more policy tightening to come this year and next,” says Jérôme Haegeli, Swiss Re Group’s Chief Economist. “Approximations of an adequate interest rate policy, proxied by our estimates of the Taylor rule, suggest that almost all major advanced economy central banks are at least 2ppts below interest rate levels that would be warranted given the current economic environment,” says Haegeli. “The Taylor rule is an equation that prescribes the central bank policy rate as a function of inflation and economic slack such as the output gap or the unemployment gap.”

To conclude this post, the above is just a sampling of the commentary, and much of it is promising. Much has already been written over the years about monetary policy rules, which answers some of the points raised by Jay Powell. These issues will be covered and analyzed in future writings, as will the recent promising renewal of the focus on rules.

Posted in Uncategorized

Leave a comment

Rules are Back In The Monetary Policy Report

Last March, I quoted Federal Reserve Chair Jerome Powell on this Economics One blog post https://economicsone.com/2022/03/03/well-have-it-in-the-next-one-well-bring-them-back-for-the-july-said-chair-powell-at-the-house-yesterday-and-at-the-senate-today/ from his March 2 and March 3 testimony at the House and Senate that “WE’LL HAVE IT IN THE NEXT ONE.” He was responding to questions at hearings of the House Financial Services Committee on March 2 and of the Senate Banking Committee on March 3, about why he and the Federal Reserve Board omitted the section on monetary policy rules in the just released February 2022 Monetary Policy Report.

Well, he was true to his word. The Monetary Policy Report released today has put the section on policy rules, including the Taylor rule as number one on the list, back in. It has statements that: “Simple monetary policy rules, which relate a policy interest rate to a small number of other economic variables, can provide useful guidance to policymakers.” And that “simple monetary policy rule considered here call for raising the target range for the federal funds rate significantly.”

On May 6 we had our annual monetary policy conference at Hoover and Stanford entitled “How Monetary Policy Got behind the Curve and How to Get Back” Well, we are beginning to see part of the how. With rules back in the Report, we are starting to see how the Fed will adjust policy and “How to Get Back.’

Posted in Uncategorized

Leave a comment

Monetary Policy Got Behind the Curve, How to Get Back

On Friday May 6, we held our annual Monetary Policy Conference at the Hoover Institution at Stanford. This year it was entitled: “How Monetary Policy Got Behind the Curve and How to Get Back,” and the title turned out to describe the theme of the conference, the papers presented, and the discussion from the audience remarkably well. Michael Bordo, John Cochrane and I organized the conference. Condoleezza Rice, Director of the Hoover Institution and former Secretary of State, gave the motivating opening remarks, mentioning monetary policy rules and bringing in the complicating factors in Ukraine. Monika Piazzesi, Stanford Professor of Economics, concluded with a great dinner talk called Inflation Blues: The 40th Anniversary Reissue?

The full agenda is shown here https://www.hoover.org/sites/default/files/agenda_may_6_2022-hoover_monetary_policy_conference_final.pdf We were pleased that so many knowledgeable speakers (summarized below) joined us, along with many more people with experience in the audience, mostly in-person at Hoover and some on-line. The audience included current policy makers, former policy makers, academics who focus on monetary and fiscal issues, people from the financial markets, and, very important, members of the media both printed press and TV.

Presenters at “How Monetary Policy Got Behind the Curve and How to Get Back“

What Monetary Policy Rules and Strategies Say

Papers be Richard Clarida, Lawrence Summers, and John Taylor

Chair: Tom Stephenson,

Fiscal Policy and Other Explanations

Papers by John Cochrane, Tyler Goodspeed, and Beth Hammack

Chair: Charles Plosser

The Fed’s Delayed Exits from Monetary Ease

Paper by Michael Bordo and Mickey Levy with discussion by Jennifer Burns

Chair: Kevin Warsh

Inflation Risks

Paper by Ricardo Reis with discussion by Volker Wieland

Chair: Arvind Krishnamurthy,

Three World Wars: Fiscal-Monetary Consequences

Paper by George Hall and Thomas Sargent with discussion by Ellen McGrattan

Chair: John Lipsky

Toward a Monetary Policy Strategy

Papers by James Bullard, Randal Quarles, and Christopher Waller

Chair: Joshua Rauh

As with earlier Hoover monetary policy conferences, there will soon be a book outlining the timely and well-reasoned arguments of the conference papers and the discussion. But the excellent and extensive press coverage of the conference already gives a good sense of the overall themes. Here is a summary and a few quotes from the press.

News Articles

In an article published in the New York Times, entitled “Fed Officials Are on the Defensive as High Inflation Lingers” by Jeanna Smialek, and subtitled “Critics have accused the Federal Reserve of not reacting quickly enough to tame rising prices. On Friday, a Fed governor explained why it took so long.” The article mentions that “Christopher Waller, a governor at the Federal Reserve, faced an uncomfortable task on Friday night: He delivered remarks at a conference packed with leading academic economists titled, suggestively, “How Monetary Policy Got Behind the Curve and How to Get Back.” The article added that “Friday’s event, at Stanford University’s Hoover Institute, was the clearest expression yet of the growing sense of skepticism around the Fed’s recent policy approach.” See https://www.nytimes.com/2022/05/06/business/economy/fed-inflation-waller.html

Nick Timiraos published an article in the Wall Street Journal entitled “Ex-Fed Official Says Rates of at Least 3.5% Will Be Needed to Slow Inflation,” and subtitled “Richard Clarida expects central bank will be required to pursue increases ‘well into restrictive territory.’” “Even under a plausible best-case scenario in which most of the inflation overshoot last year and this year turns out to have been transitory, the funds rate will, I believe, ultimately need to be raised well into restrictive territory,” said Richard Clarida, referring to the federal-funds rate, in remarks prepared for delivery Friday at a conference at Stanford University’s Hoover Institution. https://www.wsj.com/articles/ex-fed-official-says-rates-of-at-least-3-5-will-be-needed-to-slow-inflation-1165182940

Ann Saphir and Lindsay Dunsmuir of Reuters published an article entitled Former Fed policymakers call for sharp U.S. rate hikes, warn of recession, saying that “Clarida, speaking Friday to a conference at Stanford University’s Hoover Institution, said the Fed will need to raise rates to “at least” 3.5% if not higher to bring inflation back down to its 2% goal.”…“If inflation, now at 6.6% by the Fed’s yardstick, is a year from now still running at 3%, “simple and compelling” arithmetic by a widely cited policy guide known as the “Taylor rule” means rates will need to rise to 4%, he said. Clarida made the remarks at a conference convened by Stanford’s John Taylor, the author of that rule.” https://www.reuters.com/world/us/former-fed-policymakers-call-sharp-us-rate-hikes-warn-recession-2022-05-06/

Jonnelle Marte and Rich Miller wrote a Bloomberg piece entitled in Fed Officials Defend Policies, Say Forward Guidance Is Working, saying “that Waller, Bullard say Fed guidance has had substantial impact. “Two of the Federal Reserve’s most hawkish policy makers defended the central bank on Friday against charges that it had fallen well behind the curve in fighting inflation.” “Credible forward guidance means that market interest rates have increased significantly before tangible Fed action, Bullard said in remarks prepared for a conference hosted by the Hoover Institution at Stanford University. It provides another definition of ‘behind the curve,’ and the Fed is not far behind based on this definition.” … “A series of speakers at the conference, entitled “How Monetary Policy Got Behind the Curve and How to Get Back”, criticized the Fed for being late to react to rising inflation, which is now at a four-decade high.” https://www.bloomberg.com/news/articles/2022-05-06/fed-s-waller-and-bullard-defend-policies-say-guidance-working

Greg Robb, in an article on Market Watch over at Barron’s captured the theme of his piece with the straightforward title Fed Hawks Say They’re Not so Behind the Curve Combatting Inflation https://www.barrons.com/articles/federal-reserve-inflation-rate-hikes-51651947271?mod=hp_DAY_1

And Colin Lodewick of Fortune touched on similar themes in an article entitled The Fed just increased interest rates by the most since 2000. A former official says it’s not nearly enough to slow inflation https://fortune.com/2022/05/06/former-fed-official-richard-clarida-interest-rate-hikes-not-enough-slow-inflation/

Other Media at the Conference, including Television

There was also lot of TV media set up on the patio outside the auditorium where the conference was held. These included a fascinating Bloomberg TV interview of Lawrence Summers and Niall Ferguson conducted by David Westin. Check it out on YouTube.

Another example was Michael McKee’s interview of me on “Bloomberg Markets: The Close,” also set up out on the patio next to the conference at the Hoover Institution with Caroline Hyde, Romaine Bostick and Taylor Riggs. Watch the video from 2:45 to 10:55 https://www.bloomberg.com/news/videos/2022-05-07/bloomberg-markets-the-close-5-06-2022

Actual Statements by members of the Federal Open Market Committee

While the press coverage was excellent, it is very important to read the actual statements by those at the conference, especially the current members of the Federal Open Market Committee who spoke at the conference. These are now available at the Federal Reserves or at the St. Louis Federal Reserve Bank web pages, and include:

Christopher J. Waller, now Federal Reserve Governor, who published Reflections on Monetary Policy in 2021, a written version of the talk he gave at the Hoover Conference.

James Bullard, President and CEO of the Federal Reserve Bank of St, Louis, “Is the Fed “Behind the Curve”? Two Interpretations.” The press release about the talk from the Federal Reserve Bank of St. Louis is here. https://www.stlouisfed.org/news-releases/2022/05/06/bullard-discusses-is-the-fed-behind-the-curve-two-interpretations

These are all worth reading and watching, and the forthcoming book will be too.

Posted in Uncategorized

Leave a comment

“WE’LL HAVE IT IN THE NEXT ONE,” “WE’LL BRING THEM BACK FOR THE JULY,” said Chair Powell at the House yesterday and at the Senate today

At hearings of the House Financial Services Committee yesterday, and of the Senate Banking Committee today, Fed Chair Jerome Powel was asked about why he and the Federal Reserve Board omitted the section on monetary policy rules in the just released February 2022 Monetary Policy Report.

In fact, the Fed’s Monetary Policy Report sent to Congress last Friday does not include the usual section on monetary policy rules. The Fed has included the section on policy rules in its Reports since July 2017, except for July 2020 during its initial response to Covid. Thus, this section on policy rules had regularly been in the Report 8 times, and goes back to Janet Yellen’s term as Fed Chair.

This omission is significant. It occurred at the same time that the Fed has gotten well behind the curve, and inflation has risen as a result. In fact, the removal happened as the discrepancy between standard policy rules, including the Taylor rule listed in the Monetary Policy Report, and actual Fed policy is as large as it has ever been. The removal thus diverted attention from this big discrepancy. So it is good that Jay Powell was asked about the removal.

By raising the issue, the Members of Congress brought attention to this omission, and Powell’s answers are very important. While he did not provide reasons for the omission, at the House he answered Representative Bill Huizenga, by pledging “We’ll have it in the next one” and he then followed up accordingly with Representative French Hill. In the Senate, Powell answered Senator Bill Hagerty, by pledging “We’ll bring them back for the July.”

The detailed discussion is well worth reading, as the Members of Congress and the Fed Chair raise many points. It is found in the transcript as drawn from the C-SPAN record. The House transcript is here https://www.c-span.org/video/?518192-1/fed-chair-powell-expects-interest-rates-increase-quarter-percentage-point. The question and answer with Congressman Bill Huizenga went as follows (time 1:45).

Huizenga: I’M GOING TO MOVE ON TO ANOTHER ISSUE WHICH IS RULES BASED APPROACH TO MONETARY POLICY. I’M SORRY IN THE 114th CONGRESS I THINK IT WAS IN 2015 I INTRODUCED THE FORM* ACT WHICH WOULD LAY OUT A RULES-BASED MONETARY POLICY AND I KNOW IN YOUR TESTIMONY TODAY INDICATED THAT A RATE INCREASE IS EXPECTED AND YOU CONFIRM THAT WITH THE RANKING MEMBER. SO, WHAT I’M CURIOUS THOUGH IS SINCE 2017 THE FED’S FEDERAL MONETARY REPORT INCLUDING MONETARY POLICY RULES. YOU’VE BEEN VERY CLEAR AND NOW SECRETARY YELLEN HAS BEEN CLEAR THAT A LOT OF RULES ARE MODELED AND LOOKED AT. THE ONLY EXCEPTION TO THIS WAS 2020, THE FIRST YEAR OF THE PANDEMIC. AND MAYBE MORE SURPRISINGLY, THE REPORT THAT WAS JUST RELEASED THIS MONTH. FOR EXAMPLE, IN 2017 MONETARY POLICY RULE SECTION OF THE REPORT STATED, QUOTE, MONETARY POLICYMAKERS CONSIDER A WIDE RANGE OF INFORMATION ON CURRENT ECONOMIC CONDITIONS. IT’S NOT INCLUDED IN THIS REPORT. CAN YOU SHED SOME LIGHT ON WHY IT WAS ADMITTED THIS YEAR?

Powell: YOU KNOW, I HONESTLY DIDN’T KNOW THAT WAS THE CASE OR IF SOMEONE TALKED TO ME ABOUT THIS BEFORE THE THING WAS PRINTED AND SENT UP HERE, I DON’T REMEMBER. THAT IS ALSO A REAL POSSIBILITY GIVEN THE NUMBER OF THINGS I HAVE ON MY MIND RIGHT NOW. AS YOU SAY, WE DIDN’T HAVE IT IN JULY OF 20. WE’LL HAVE IT IN THE NEXT ONE. IT WAS NO BIG THOUGHT, AS FAR AS I KNOW, GOING INTO THAT. SOMETIMES WE INCLUDE IT, SOMETIMES WE DON’T. I WILL SAY THINKING ABOUT POLICY THROUGH RULES IS SOMETHING THAT I LEARNED A LOT ABOUT MONETARY POLICY DOING THAT. WHEN YOU’RE ACTUALLY IMPLEMENTING POLICY, NO COMMITTEE HAS EVER REALLY USED POLICY RULES AS A WAY OF SETTING POLICY. USE THEM TO INFORM YOUR THINKING.

Huizenga: YES, I GUESS MY IDEA WITH THE FORMAT* WAS TO THEN INFORM THE MARKET AND THAT INCLUDES US AS CITIZENS, AS WELL. I’D LIKE THIS COMMITTEE TO REEXAMINE THAT.

*Note that FORM and FORMAT refer to the Fed Oversight Reform and Modernization Act.

The detailed questions and answers with Representative French Hill are here (time near 2:01)

Hill: I DO ENCOURAGE PEOPLE TO READ THIS REPORT BECAUSE INFLATION IS A THIEF. YOU ANSWERED THE QUESTION TO MR. HUIZENGA YOU WERE NOT AWARE IN THE 2022 MONETARY POLICY REPORT THAT THE RULES SECTIONS IN THE MONETARY POLICY WAS NOT INCLUDED. IS THAT RIGHT?

Powell: I WAS AWARE OF IT A COUPLE DAYS AGO. WHAT I SAID IS I DON’T REMEMBER ANY PRIOR DISCUSSION. BUT THAT DOESN’T MEAN IT DIDN’T HAPPEN. IT JUST MEANS I DON’T REMEMBER IT.

Hill: IN THE FOMC MEETINGS, DO THEY STILL HAVE A PRESENTATION START OF THE STAFF PRESENTATION SORT OF A TREND ANALYSIS ON USING THOSE RULES THAT ARE TRADITIONALLY IN THE POLICY REPORT. DOES THAT STILL GO ON IN FOMC MEETINGS?

Powell: YES

Hill: I THINK THAT’S AN INDICATION THAT IS PROBABLY BEST THAT IT BE INCLUDED IN THE REPORT. I WAS LOOKING AT SOME FORECASTING ABOUT THE SO-CALLED TAYLOR RULE DATING TO THE 1990s WHICH YOU’VE TESTIFIED ON MANY TIMES. ARE YOU AWARE OF WHAT THE TAYLOR RULE WOULD INDICATE NOW IN ITS FORMULA VIS-A-VIS THE INFLATION WE HAVE TODAY?

Powell: GENERALLY, YEAH.

Hill: DO YOU KNOW THE RANGE?

Powell: HIGH.

Hill: THE ANSWER I SAW WAS 9.55%. WHICH DOESN’T MEAN IT’S RIGHT OR WRONG, BUT IT’S ONE OF THE INDICATORS ABOUT HOW FAR OFF WE ARE MAYBE IN OUR FUNDS RATE TARGETING. SO, I’M GLAD TO HEAR YOU’LL CONSIDER THAT BEING PUT BACK IN THE REPORT.

And the detailed question and answer session with Senator Bill Hagerty is here https://www.c-span.org/video/?518193-1/acting-federal-reserve-chair-testifies-economy (at time 1:45)

Hagerty IT FEELS LIKE THE FED IS BEHIND THE CURVE RIGHT NOW AND MAY HAVE TO TAKE MORE AGGRESSIVE ACTIONS THAN OTHERWISE WOULD HAVE BEEN THE CASE, AND THE MONETARY POLICY REPORT EMITTED THE MONETARY POLICY RULES, AND I KNOW THEY ARE NOT INTENDED TO BE SCRIPTED THERE AND THEY ARE THERE TO CONSULT AND IT WAS CONCERNING THAT THEY WERE MISSING. I THINK THE RULES WOULD HAVE INDICATED THAT WE’RE BEHIND THE CURVE, THAT THERE IS MORE TO BE DONE ON INFLATION. IT BROUGHT ME TO THINK ABOUT HOW DOES THE FED THINK ABOUT ACCOUNTABILITY, HOW DO YOU THINK ABOUT HOLDING THE FED ACCOUNTABLE FOR MANAGING INFLATION?

Powell. WE’LL BRING THEM BACK FOR THE JULY. SOMETIMES WE DO AND SOMETIMES DON’T. I WOULD RECOMMEND LOOKING AT THE CLEVELAND FED, IT HAS REALLY ALL OF THE RULES, AND THERE’S A RANGE OF RULES BUT CLEARLY THE MEDIAN RULE IS, YOU KNOW, THERE. SO IN TERMS OF ACCOUNTABILITY, IT STARTS WITH TRANSPARENCY FROM US AND EXPLAINING TO YOU. YOU ARE THE MECHANISM THROUGH WHICH WE GET OUR TRANSPARENCY. WE DELIVER TRANSPARENCY AND WE GET OUR DEMOCRATIC ACCOUNTABILITY BY EXPLAINING OURSELVES IN UNDERSTANDABLE TERMS TO YOU AND YOU HOLDING US ACCOUNTABLE AND OUR SYSTEM OF GOVERNMENT IT RUNS THROUGH THIS COMMITTEE AND THE SENATE AND THE HOUSE AS WELL. WE TRY TO BE VERY TRANSPARENT. WE TRY TO BE ENGAGED WITH MEMBERS TO EXPLAIN AND HEAR YOUR CONCERNS AND THOSE KINDS OF THINGS. ULTIMATELY, IT’S THE BOTTOM LINE. WE BOTH COME FROM THE BUSINESS WORLD AND IT’S WHAT YOU DELIVER, AND WE NEED TO DELIVER PRICE STABILITY AND WE ARE NOT CURRENTLY DOING THAT AND WE ARE HIGHLY MOTIVATED TO GET THE ECONOMY BACK TO WHERE WE HAVE THAT UNDER CONTROL.

Posted in Uncategorized

Leave a comment

A New-Old Critique of Monetary Policy

Today, John Cochrane, Mickey Levy, Kevin Warsh & I spoke at a roundtable discussion on the Fed’s monetary policy at the Hoover Economic Policy Working Group. Cochrane talked about the fiscal side, Levy about the best inflation measures, Warsh about regime change, and I talked about the big deviations in policy from standard monetary policy rules. Many of the speakers had written about these issues for a year or so, but bringing them together revealed different perspective but with a common theme: the main concern was the high inflation rate induced by the new policy actions, whether the super low policy interest rate, the high money growth, or the big balance sheet expansion.

Some talked about how the Fed got into this difficult situation, and that brought back old memories of the 1970s where the critique was similar. All agreed that the Fed was now behind the curve, and the question was when and how rapidly to get back on track. The event had many commentators and guests–including monetary experts alike Mervyn King, Andy Levin, David Papell, and Robert Heller, who also spoke out on the same theme.

The whole Zoom event was video-recorded, and can be found here: https://www.hoover.org/events/roundtable-economic-policy-john-cochrane-mickey-levy-kevin-warsh-and-john-taylor along with the list of participants and slide presentations, which contain many useful charts and background references.

Posted in Uncategorized

Leave a comment

Bill McGurn Shows Nice Video Clip of Milton Friedman

Bill McGurn make a lot of good references to Milton Friedman in a video just posted on the Wall Street Journal web site. We hear Milton talking about the power of the market. https://www.wsj.com/video/series/main-street-mcgurn/wsj-opinion-joe-biden-milton-friedman-and-a-lesson-in-inflation/E3400D7C-AA91-49CC-8341-65721E37BDF4 It is a great video and I always use it my Economics 1 introductory economics lectures at Stanford. Below is a review slide from the lecture on September 29 of this year with the link to Friedman’s video at the end, and here is the link: https://www.youtube.com/watch?v=R5Gppi-O3a8

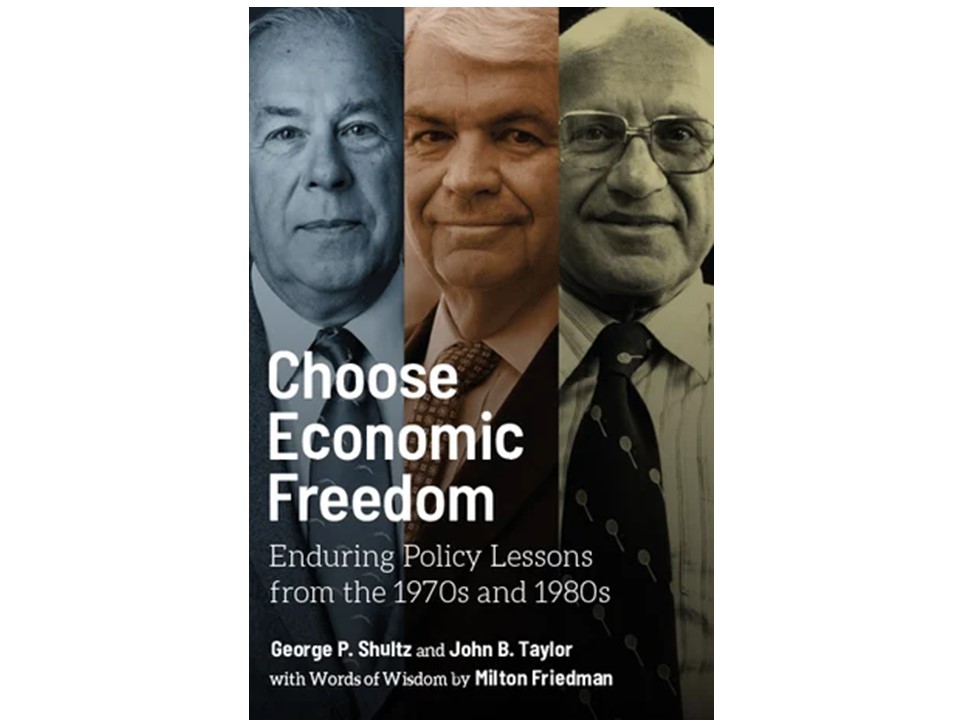

Of course, a big reason to refer to Milton Friedman these days is the ongoing increase on inflation which virtually every person is now seeing and talking about. That is the main message of McGurn. It is also the message of a recent book Choose Economic Freedom with George Shultz, Milton Friedman and me in which we trace out the history of the 1970s, and see it repeating itself, unless the Federal Reserve takes action soon.

Posted in Uncategorized

Leave a comment

New Principles of Economics Now Available

I am very happy to say that the new edition of Principles of Economics v9.1 is now officially published. Here is where you can find it on the FlatWorld web page: https://catalog.flatworldknowledge.com/catalog/editions/principles-of-economics-9-1. It has been pleasure for me to continue to work on this edition with Akila Weerapana of Wellesley College, who brings terrific experience and knowledge of teaching basic economic principles.

The book continues to cover basic economic principles at the introductory level, and it shows how economics is more important than ever. It remains grounded in the central idea that people make purposeful choices with scarce resources and interact with others when they make these choices. The new edition covers key issues related to COVID-19 and the economic policy responses. It is updated to reflect the current economic situation, and incorporates the latest GDP, inflation, and unemployment data in charts and figures. It includes tables and a discussion of the start and end dates of the 2020 recession sparked by the coronavirus pandemic. Applications reflect the impact of the coronavirus pandemic, and the book shows how students can use the basic model to understand the impact of the COVID-19 on the economy .

The book now has over 180 new links, including brief video lectures scripted and recorded by me that have been usefully aligned to introduce, explain, and illustrate key economic concepts. There are also links to videos that apply to real-world situations. The new book covers the fiscal policy responses and special monetary policy actions including the rapid growth of the Fed’s balance sheet in response to the impact of the COVID-19 pandemic and prospects for eventual unwinding.

There will also be separate volumes of the book, titled Principles of Microeconomics and Principles of Macroeconomics, available. All of the supplements for the books are updated to reflect the new videos and the content updates made in this version.

Posted in Uncategorized

Leave a comment

“The Most Reckless Monetary Policy Since Arthur Burns”

Today the Editorial Board of the Wall Street Journal wrote that the Federal Open Market Committee has shown “little interest in reeling in what has been the most reckless monetary policy since Arthur Burns roamed the Eccles Building.”

Last month I published an article, which Project Syndicate cleverly headlined “Is the Fed Getting Burned Again?” It summarized research consistent with this Wall Street Journal editorial. I presented the research in detail in an April 2021 paper “The Optimal Return to a Monetary Policy Strategy” which I gave at the City University of New York.

This story goes back to memo reprinted in the book Choose Economic Freedom which George Shultz and I published last year (and because we quoted Milton Friedman so much he is a coauthor.) The memo was written fifty years ago (June 22, 1971) from Arthur Burns, who was then Chair of the Fed, to President Richard Nixon. Inflation was picking up, and Burns wanted Nixon and others to understand that the inflation was not due to monetary policy or to any action by the Fed. Instead, Burns recommended “a strong wage and price policy” to Nixon. The memo convinced Nixon, and he instituted a wage and price freeze, and followed up with wage and price controls and guidelines for the whole economy. It was a disaster, and, as the Fed was off the hook, money growth sored, inflation and unemployment got worse for the rest of the decade.

So look at where we are now. Inflation has picked up, and the Fed is saying that it is not responsible for that development. Instead, the Fed argues that today’s high inflation just reflects the bounce back from the low inflation of last year.

And the Fed is more interventionist now than it was in Burns’s day. Its balance sheet is exploding as the Fed purchases massive amounts of Treasury bonds and mortgage-backed securities. M2 growth has risen sharply. The federal funds interest rate is now lower than recommended by many trusted policy rules, including the Taylor Rule, listed on page 44 of the Fed’s most recent July 9, 2021 Monetary Policy Report.

“History hasn’t been kind to Burns” as the Wall Street Journal says in its editorial. It’s not too late to learn from past mistakes and adjust monetary policy. As John Holland of Olathe, Kansas said in a letter to the Wall Street Journal on March 1: “Powell Shouldn’t Repeat Arthur Burns’s Mistakes.”

Posted in Monetary Policy

Leave a comment

Shortest Recession in US History

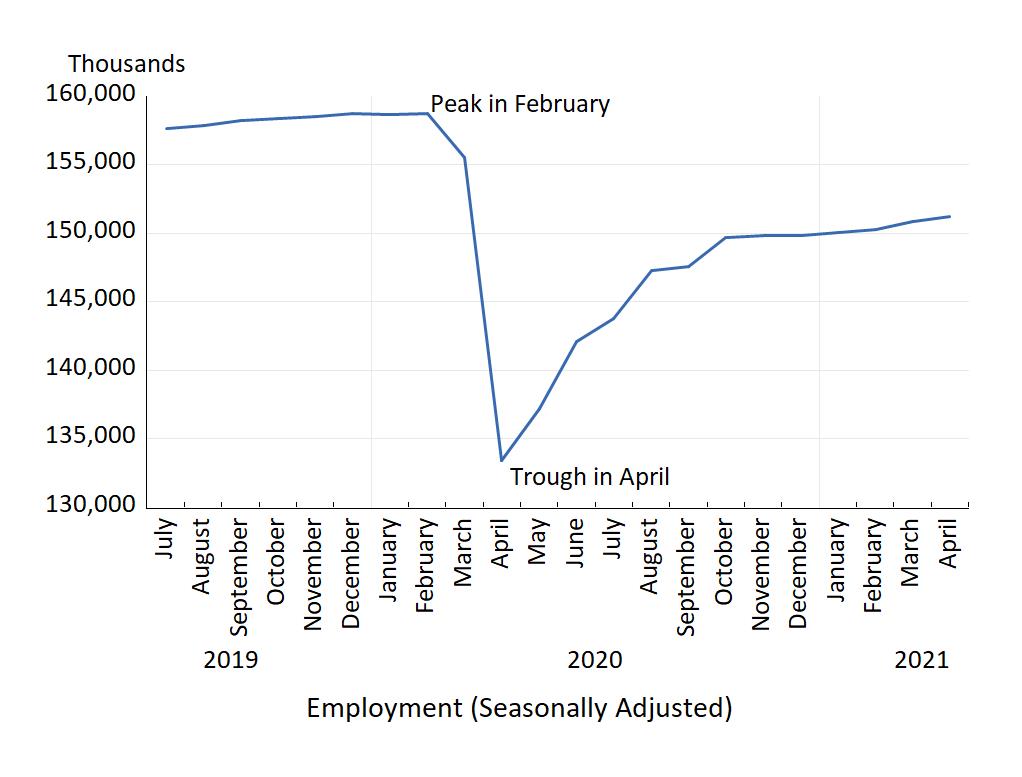

The Business Cycle Dating Committee of the National Bureau of Economic Research has a very important job. It is responsible for determining the peaks and troughs of business cycles in the United States. It thus decides how long recessions are and also how long expansions are. The Chair of the Committee is Professor Robert Hall of Stanford University.

The latest decision of Committee occurred just this week on July 19, 2021. The Committee decided that a trough in monthly economic activity occurred back in April 2020. They also determined that the previous peak occurred back in February 2020. Thus the recession, measured by the decline in employment from peak to trough, lasted only two months. It was the shortest recession in United States history. It was completely caused by COVID-19.

This chart shows total employment in the United States. You can see that the peak in employment occurred in February and the trough occurred in April. Though only lasting two months the decline in employment was huge at 25.4 million.

Posted in Financial Crisis

Leave a comment