A few weeks ago Paul Ryan and I wrote an article proposing changes in the Federal Reserve Act. One change would require the Fed to focus on “the single goal of long-run price stability within a clear framework of overall economic stability.” Since then some have argued that changing the dual mandate in this way would not have prevented the recent highly discretionary monetary policy, which, in my view, has on balance been counterproductive. For example, Greg Mankiw writes on his blog that “If the Fed’s mandate were different, monetary policy today might well be the same. That is, with inflation now below its target, the Fed could be pursuing QE2 even if it were operating under the proposed mono mandate.” Similarly, in today’s Wall Street Journal Marc Sumerlin writes that such a change would “actually be supportive of the Fed’s current program.”

But there are several reasons to believe that QE2 would not have happened had Fed officials not been able to refer to a dual mandate in the Federal Reserve Act as justification for the intervention. First consider this bit of emprical evidence: There have never been so many references to the dual mandate by Fed officials as in the past year or so. If the dual mandate was not a factor in justifying and embarking on QE2, then why did Fed officials find the need to refer to it so much as justification for QE2 in the past year? In contrast, during the 1980s and 1990s, Federal Reserve officials rarely referred to the dual mandate (even in the early 1980s when unemployment was higher than today), and when they did so it was to make the point that achieving the goal of price stability was the surest way for monetary policy to keep unemployment down. Now, as Paul Ryan and I put it, “Advocates of aggressive Fed interventions cite the ‘maximum employment’ aspect of the Fed’s dual mandate.”

What about the argument that an inflation rate below the Fed’s target is alone enough to rationalize the unorthodox QE2 policy? I do not agree with this because the current low interest rate policy without QE2 is what is appropriate to deal with inflation being below the target. For example, the Taylor rule says that the federal funds rate is where it is because inflation is below its target. In other words that low interest rate policy means that monetary policy is doing what it should be doing to combat “too low” inflation, without QE2. Moreover, I think it would have been much harder to drum up support for QE2 based solely on deflationary concerns. As the Bloomberg graph below on breakeven inflation (USGGBE10) shows, the dip in expected inflation was quite small in 2010 and an argument based on that alone would not have carried the day in my view.

I have long been in favor of the Fed setting a target for inflation but not for unemployment. Here is a paper I gave at the 1996 Jackson Hole conference which explains why. In brief, by trying to focus on unemployment the Fed has actually increased unemployment. That was true in the 1970s and it is true recently: If the Fed had not kept interest rates so low when inflation was rising and the economy was growing in the 2002-2005 period, then we would have avoided much of the boom and the bust which eventually caused the devastating increase in unemployment.

One source of disagreement in debates about the mandate (which I tried to clarify in the 1996 paper) is confusion over the difference between the Fed’s goals and what the Fed reacts to. These are two different things. In particular, Sumerlin’s assessment that the Fed should react to credit aggregates is not inconsistent with the proposed changes in the mandate. Just as cutting interest rates in a recession when GDP falls below potential is an essential part of achieving a price stability goal in the framework of economic stability, so may be raising interest rates in a credit boom. The key idea is for the Fed to have and to lay out a strategy to achieve its goal. The strategy could entail credit aggregates, but that is a debate about how to achieve the mandate, not about the mandate itself.

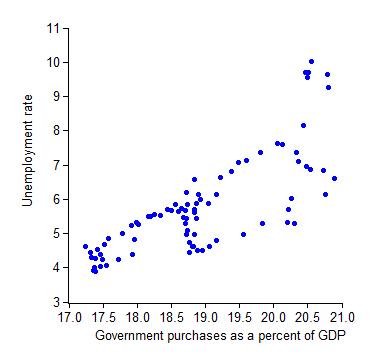

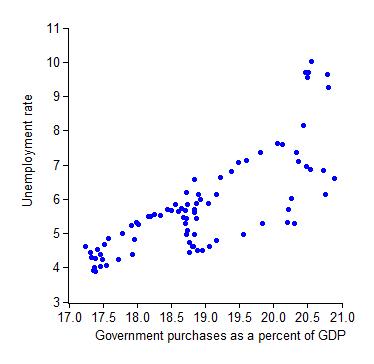

In sharp contrast, the data on spending shares show that the most effective way to reduce unemployment is to raise investment as a share of GDP. The second chart shows the relation between unemployment and fixed investment over the past two decades. Higher shares of investment are associated with lower unemployment.

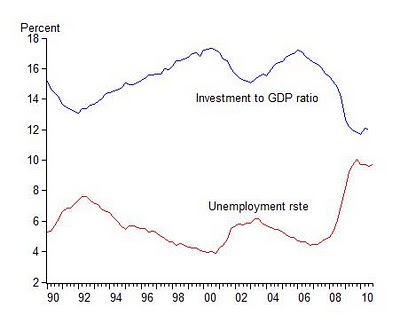

In sharp contrast, the data on spending shares show that the most effective way to reduce unemployment is to raise investment as a share of GDP. The second chart shows the relation between unemployment and fixed investment over the past two decades. Higher shares of investment are associated with lower unemployment.  The time series in the third chart show the relationship from another perspective. Either way you look at it, the relationship between unemployment and the investment share is remarkably close. It holds for both non-residential and residential investment, and is a subject of my current research. Of the four shares of GDP (the other two of course being consumption and net exports), the investment share shows by far the largest negative association with unemployment.

The time series in the third chart show the relationship from another perspective. Either way you look at it, the relationship between unemployment and the investment share is remarkably close. It holds for both non-residential and residential investment, and is a subject of my current research. Of the four shares of GDP (the other two of course being consumption and net exports), the investment share shows by far the largest negative association with unemployment.

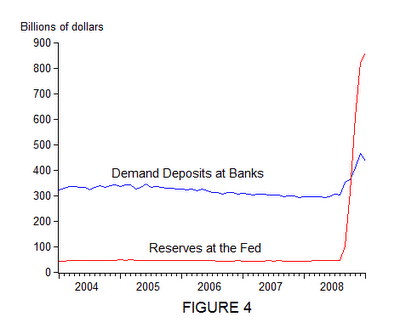

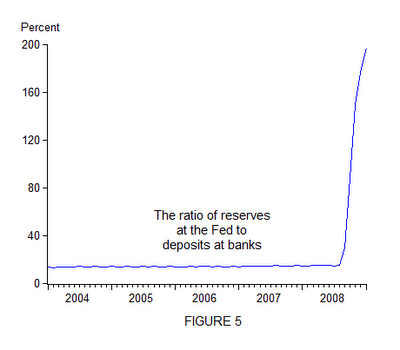

“Note that the increase in demand deposits was not as large as one would expect if the reserve ratio was constant. In fact, as shown in Figure 5, the reserve ratio was not constant. It was nearly constant for a number of years but then increased sharply in the fall of 2008 as banks chose to hold some of the large increase in reserves as excess reserves over the amount they were required to hold. In other words they decided not to lend out all the reserves. Banks did not lend out all the reserves because there was not enough demand for loans and because they were concerned about risks.

“Note that the increase in demand deposits was not as large as one would expect if the reserve ratio was constant. In fact, as shown in Figure 5, the reserve ratio was not constant. It was nearly constant for a number of years but then increased sharply in the fall of 2008 as banks chose to hold some of the large increase in reserves as excess reserves over the amount they were required to hold. In other words they decided not to lend out all the reserves. Banks did not lend out all the reserves because there was not enough demand for loans and because they were concerned about risks.

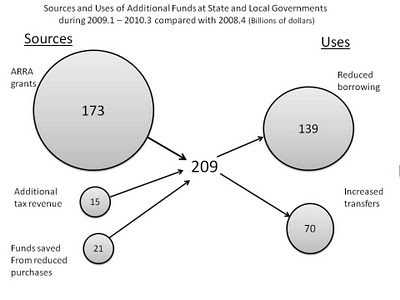

As American Recovery and Reconstruction Act (ARRA) grants from the federal government rose, the amount of net borrowing by state and local governments declined. The data come from the Bureau of Economic Analysis, Department of Commerce. The level of purchases is much less than government officials predicted when ARRA was passed in early 2009.

As American Recovery and Reconstruction Act (ARRA) grants from the federal government rose, the amount of net borrowing by state and local governments declined. The data come from the Bureau of Economic Analysis, Department of Commerce. The level of purchases is much less than government officials predicted when ARRA was passed in early 2009.