In a speech in Washington last week I made a proposal to restore the legislative requirement that the Fed report and be accountable for its strategy for monetary policy. Such a requirement was the law throughout the 1980s and 1990s, but was removed in 2000. There is a big difference, however, between the old law and what I proposed. The old law focused on reporting about the “ranges of growth or diminution of the money and credit aggregates,” while the new law would focus on the “strategy, or rule, of the Board and the FOMC for the systematic adjustment of the federal funds rate in response to changes in inflation and in the real economy needed to achieve the price stability objective.” Money would still be a factor in the strategy in that the interest rate would be determined in the money market through the demand and supply of money. The Fed would have the discretion to choose the strategy, but would be required to explain in writing and in hearings any deviations from the strategy. One possible strategy could be the Taylor rule, but the Fed could choose any rule as long as it stuck with it or explained why it deviated from it. .

Here is some press reaction to the proposal

Bloomberg News: “Taylor Proposes Altering Fed Law to Require ‘Systematic’ Rate Setting Rule”

Dow-Jones: “Stanford’s Taylor Urges Turning Monetary Policy Rules Into Law to Limit Fed”

Reuters: “Economist Taylor Wants New Law for Fed Policy”

Globe and Mail: “A Rules Based Fed?”

Another reaction, not covered in these articles, came from some of the people who had experience at the Fed in the 1980s and 1990s. They say that they found the old reporting and accountability requirements to be of value in creating a process at the Fed for discussing a monetary strategy and that the new requirements could be of similar benefit.

One logical date is August 27, the day of Ben Bernanke’s Jackson Hole speech where he discussed the framework of quantitative easing in detail. Indeed, this Jackson Hole speech is frequently mentioned in the financial press. The date of the speech is shown in the chart. The long-term rate was 2.66 percent on that date. If anticipations of quantitative easing lowered long-term interest rates, then one would expect this rate to have been lower on November 2, the day before the FOMC’s recent action. But this is not what happened. The interest rate was the same 2.66 percent on November 2 as it was on August 27.

One logical date is August 27, the day of Ben Bernanke’s Jackson Hole speech where he discussed the framework of quantitative easing in detail. Indeed, this Jackson Hole speech is frequently mentioned in the financial press. The date of the speech is shown in the chart. The long-term rate was 2.66 percent on that date. If anticipations of quantitative easing lowered long-term interest rates, then one would expect this rate to have been lower on November 2, the day before the FOMC’s recent action. But this is not what happened. The interest rate was the same 2.66 percent on November 2 as it was on August 27.

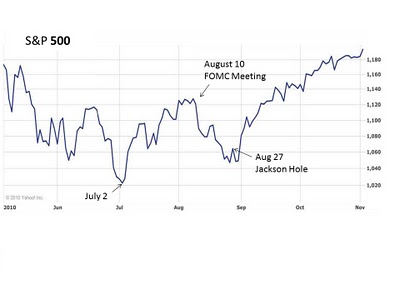

Next consider stock prices. The third chart shows the S&P 500 index over the same period. Observe that the current rally began in early July as shown in the chart. Evidently concerns about a double dip recession had diminished by early July and earnings reports began improving. From July 2 to August 10 the S&P 500 rallied by 10 percent. That rally was temporarily interrupted starting on August 10, but then continued. From August 10 to November 2 the S&P 500 rose another 7 percent.

Next consider stock prices. The third chart shows the S&P 500 index over the same period. Observe that the current rally began in early July as shown in the chart. Evidently concerns about a double dip recession had diminished by early July and earnings reports began improving. From July 2 to August 10 the S&P 500 rallied by 10 percent. That rally was temporarily interrupted starting on August 10, but then continued. From August 10 to November 2 the S&P 500 rose another 7 percent.

John Cogan and I first reported these results in a preliminary way over a year ago in a September 16, 2009 a Wall Street Journal article with Volker Wieland, entitled “

John Cogan and I first reported these results in a preliminary way over a year ago in a September 16, 2009 a Wall Street Journal article with Volker Wieland, entitled “ Using the Mian-Sufi results, which are based on a comparison of different regions of the United States, I estimated the amount by which total personal consumption expenditures first increased as people were encouraged to trade in their clunker and purchase new cars, and then declined because many of the trade-ins were simply brought forward. To make this increase and subsequent decrease easier to see, the second chart focuses on personal consumption expenditure during the period of the program.

Using the Mian-Sufi results, which are based on a comparison of different regions of the United States, I estimated the amount by which total personal consumption expenditures first increased as people were encouraged to trade in their clunker and purchase new cars, and then declined because many of the trade-ins were simply brought forward. To make this increase and subsequent decrease easier to see, the second chart focuses on personal consumption expenditure during the period of the program.  You can see that consumption rises above what it would have been without the program and then actually falls below what it would have been. Some argue that bringing forward purchases like this is exactly what such programs are supposed to do, but the graph makes it very clear that the offsetting secondary effects occur so quickly that the net result is an insignificant blip in the recovery. The impact is not sustainable.

You can see that consumption rises above what it would have been without the program and then actually falls below what it would have been. Some argue that bringing forward purchases like this is exactly what such programs are supposed to do, but the graph makes it very clear that the offsetting secondary effects occur so quickly that the net result is an insignificant blip in the recovery. The impact is not sustainable.