The book is entitled HOW MONETARY POLICY GOT BEHIND THE CURVE — AND HOW TO GET BACK and is based on conference held on May 6. The conference is described here: https://economicsone.com/2022/05/08/monetary-policy-got-behind-the-curve-how-to-get-back/ The book on the conference has many insightful papers, great commentary, and excellent press coverage. Current and former Federal Open Market Committee Members gave critical assessments and debated with Fed watchers from the markets and academics.

The stock market reaction to the Kansas City Fed meeting in Jackson Hole today was not so pleasant. The Dow Jones Industrial Average was down over 1,000 points or by over 3 %. The S&P 500 was down 3.4 percent. The markets started to fall with Chairman Powell’s speech in which he said “We must keep at it until the job is done,” and he emphasized credibility almost as if in a full policy rule-like mode.

But the emphasis of the market commentary was not much on the benefits of credibility of monetary policy. Rather it was that the Fed will simply keep raising the federal funds rate until we really see inflation coming down.

The year 1982 was so much different than the year 2022. Inflation had been high for 15 years in 1982, not 15 months as today, and inflation had set in. The wage price spiral was in full bloom. It took a big change in monetary policy too bring inflation down, and that is what had happened. But today inflation is not so entrenched as it was in the 1970s when higher interest rates caused big recessions. An expectation of a credible disinflation policy will prevent pass through to wages and other prices. The emphasis should be on credibility and expectations, and on a clear understanding of how different policy and the economy have been recently compared with the 1960s and 1970s. Yes, the Fed has to adjust the interest rate some more to bring inflation down to levels consistent with the the 2 percent target. But a more credible Fed policy will make the adjustment much smoother and with the main impact on inflation, not on the real economy.

Today the Editorial Board of the Wall Street Journal wrote that the Federal Open Market Committee has shown “little interest in reeling in what has been the most reckless monetary policy since Arthur Burns roamed the Eccles Building.”

Last month I published an article, which Project Syndicate cleverly headlined “Is the Fed Getting Burned Again?” It summarized research consistent with this Wall Street Journal editorial. I presented the research in detail in an April 2021 paper “The Optimal Return to a Monetary Policy Strategy” which I gave at the City University of New York.

This story goes back to memo reprinted in the book Choose Economic Freedom which George Shultz and I published last year (and because we quoted Milton Friedman so much he is a coauthor.) The memo was written fifty years ago (June 22, 1971) from Arthur Burns, who was then Chair of the Fed, to President Richard Nixon. Inflation was picking up, and Burns wanted Nixon and others to understand that the inflation was not due to monetary policy or to any action by the Fed. Instead, Burns recommended “a strong wage and price policy” to Nixon. The memo convinced Nixon, and he instituted a wage and price freeze, and followed up with wage and price controls and guidelines for the whole economy. It was a disaster, and, as the Fed was off the hook, money growth sored, inflation and unemployment got worse for the rest of the decade.

So look at where we are now. Inflation has picked up, and the Fed is saying that it is not responsible for that development. Instead, the Fed argues that today’s high inflation just reflects the bounce back from the low inflation of last year.

And the Fed is more interventionist now than it was in Burns’s day. Its balance sheet is exploding as the Fed purchases massive amounts of Treasury bonds and mortgage-backed securities. M2 growth has risen sharply. The federal funds interest rate is now lower than recommended by many trusted policy rules, including the Taylor Rule, listed on page 44 of the Fed’s most recent July 9, 2021 Monetary Policy Report.

“History hasn’t been kind to Burns” as the Wall Street Journal says in its editorial. It’s not too late to learn from past mistakes and adjust monetary policy. As John Holland of Olathe, Kansas said in a letter to the Wall Street Journal on March 1: “Powell Shouldn’t Repeat Arthur Burns’s Mistakes.”

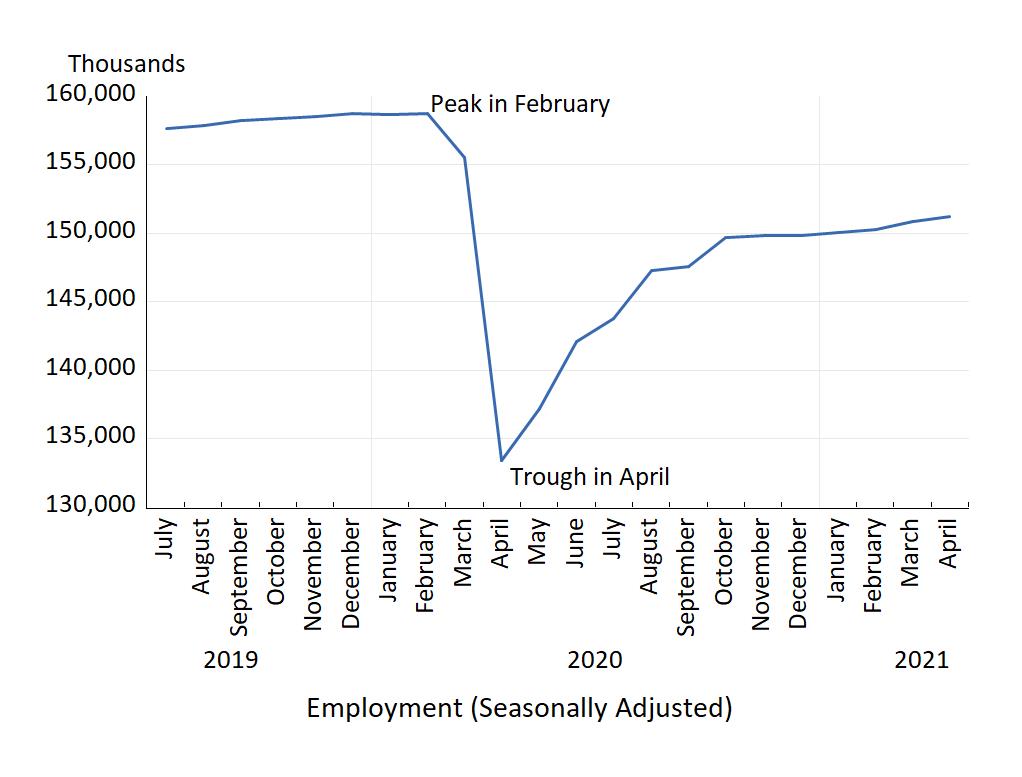

The Business Cycle Dating Committee of the National Bureau of Economic Research has a very important job. It is responsible for determining the peaks and troughs of business cycles in the United States. It thus decides how long recessions are and also how long expansions are. The Chair of the Committee is Professor Robert Hall of Stanford University.

The latest decision of Committee occurred just this week on July 19, 2021. The Committee decided that a trough in monthly economic activity occurred back in April 2020. They also determined that the previous peak occurred back in February 2020. Thus the recession, measured by the decline in employment from peak to trough, lasted only two months. It was the shortest recession in United States history. It was completely caused by COVID-19.

This chart shows total employment in the United States. You can see that the peak in employment occurred in February and the trough occurred in April. Though only lasting two months the decline in employment was huge at 25.4 million.

Today I published an article in Project Syndicate. It starts with a memo sent fifty years ago, on June 22, 1971, by Fed Chair Arthur Burns to President Richard Nixon. Inflation was rising and Burns wrote to Nixon that the Fed was not to blame. Rather the economy had changed and a new policy – a wage and price freeze and controls—was needed.

The memo convinced Nixon, and wage and price controls were implemented. But the intrusive nature began to show and the government controls were failing. Moreover, the Fed let the money supply increase, inflation rose to double digits, and the unemployment rate rose.

Last year, George Shultz and I wrote a book about this period, and we included the full text of the Burns memo because it is a perfect example of how bad ideas lead to bad policies, which in turn lead to bad economic outcomes. By the same token, good ideas lead to good policy and good economic performance, as Schultz and I showed.

The lesson for today is clear: inflation is picking up, and the Fed is once again claiming that it is not responsible for that development. Rather it is simply a bounce back from low inflation of 2020.

Moreover, the Fed’s policy is interventionist. The balance sheet has exploded, the growth rate of M2 has risen sharply, and the federal funds interest rate is now low compared to monetary policy rules in the Fed’s Monetary Policy Report.

It is not too late to learn and to change, but time is running out.

Yesterday, I gave a keynote talk at the tenth American Economic Association Conference on Teaching and Research in Economic Education (CTREE). I have been teaching economics for 53 years. I love teaching economics. I love researching economics. And I love doing policy in economics. So it was a pleasure to talk about teaching economics, and the questions from other economic teachers and researchers in the audience were really good. Here are the slides. I talked mainly about teaching introductory economics. My main message is that students and teachers have benefited greatly, and can benefit greatly, from the new technology–including Zoom– but that basic economic ideas still work just fine when applied to the recent pandemic around the world, especially if we learn how to use the new technology well.

Ten years ago, I gave a keynote talk at the first CTREE and here are my slides from ten years ago. Yesterday I built on that earlier lecture. The Conference was then a major new initiative of the AEA to focus on teaching economics at all levels. The first conference was an outstanding success, as was the one held virtually in the past few days. It is a great idea to have a conference on teaching. I have written economics textbooks, including one with Bob Hall that was first published 35 years ago and one on Principles of Economics with Akila Weerapana that was first published 25 years ago, and is now in the 9th edition with FlatWorld.

But much has changed about teaching over the years, and COVID-19 and the responses have provided more lessons. My talk is in three parts

(1) What we learned about teaching following the Global Financial Crisis?

(2) What we learned about teaching in the current crisis?

(3) What are the lessons about teaching for the future?

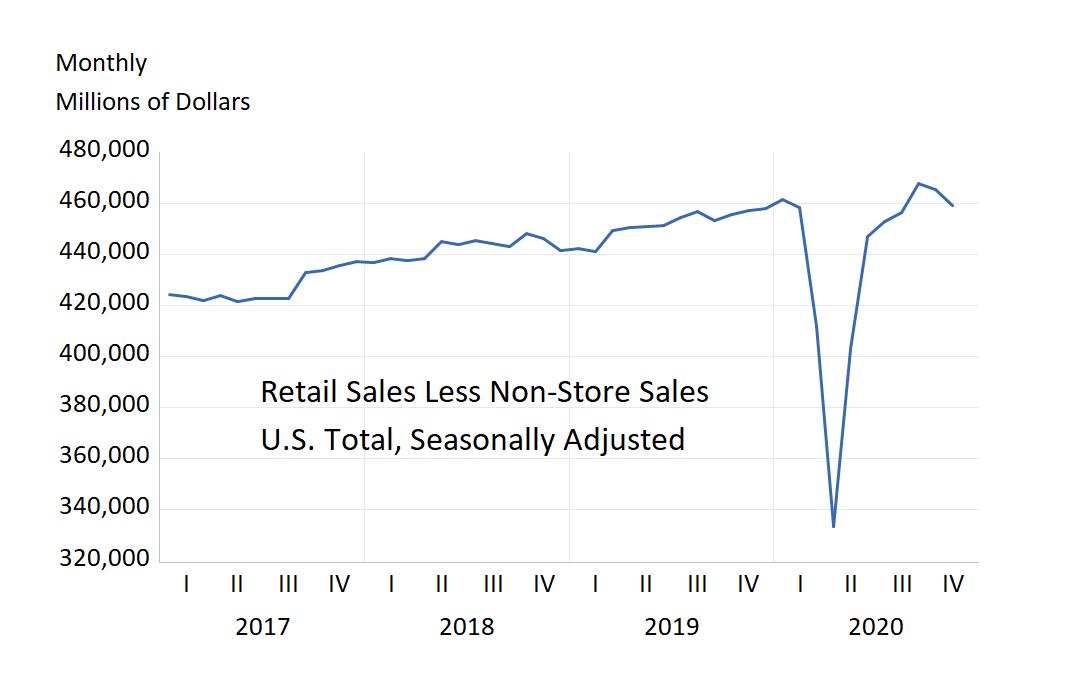

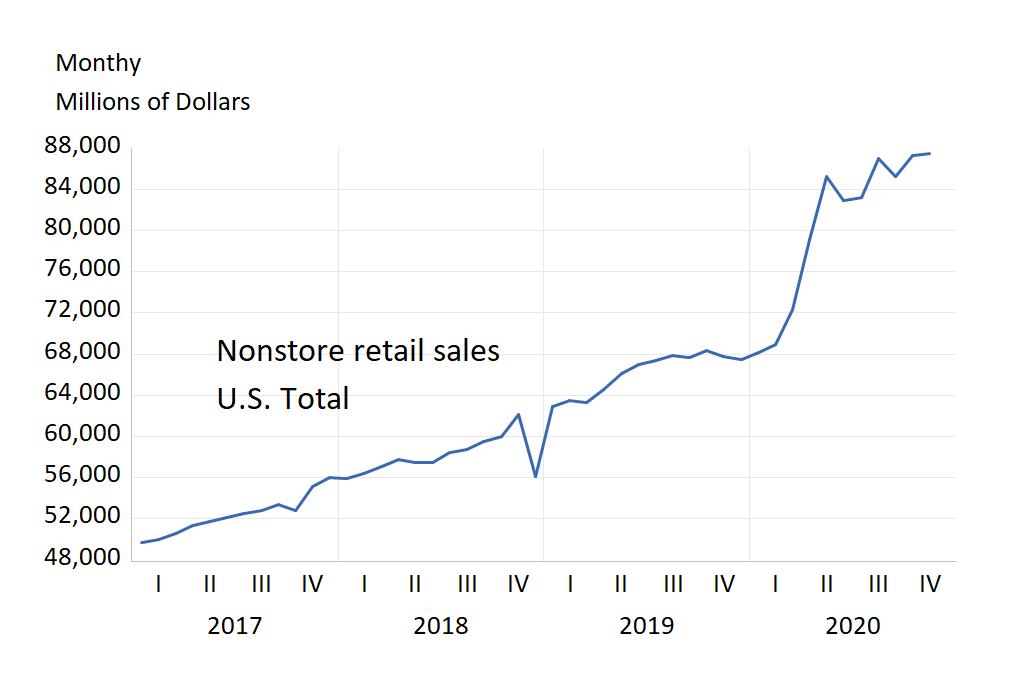

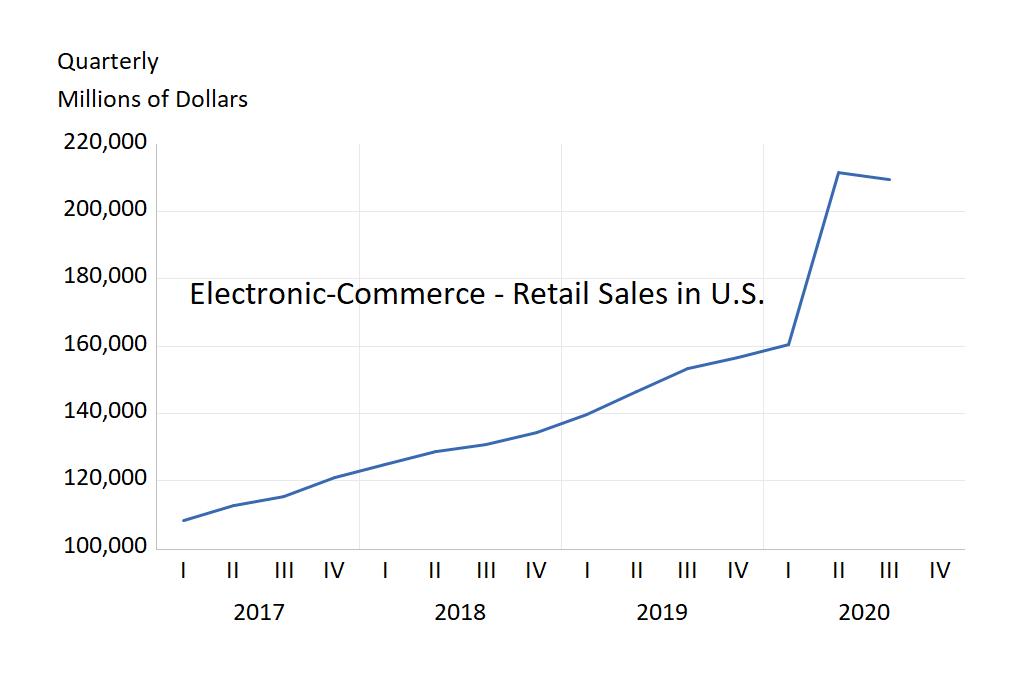

Last week at the American Economic Association meetings, held online, many papers focused on Covid-19. A good example was the session organized by Dominick Salvatore which included Jan Eberly, Raghu Rajan, Carmen Reinhart, Joe Stiglitz, Larry Summers, and me. Most papers focused on the economic policy impact of the Coronavirus. I focused the “supply side” policies rather than on the “demand side” policies. Using a simple model, key facts naturally emerge if one simply divides retail sales into store-sales versus non-store-sales or electronic sales. To see this, take a look at these three figures.

The first figure shows that the onslaught of the pandemic in the second quarter of 2020 immediately caused a sharp decline in retail sales less non-store sales in the United States. This was followed by rebound in the second third quarter of 2020. Note that the rebound, while very sharp, left total retail sales in stores no greater than they were before the pandemic.

The second figure shows that non-store sales increased from the time the pandemic began, just as in-stores sales were collapsing. Without non-store sales, total retail sales would have declined.

And the third figure shows an alternative measure: electronic-commerce. It is only available on a quarterly basis but tells the same story as the in-store versus non-store story—a large increase starting at the time of the pandemic.

In sum, the pandemic had a big economic impact on in-person store sales, measured by total sales less non-store sales. But there is a countervailing positive effect through non-store sales or e-commerce.

As of this writing, the increase in non-store or e-commence sales is not abating, but rather continues to rise, even after in-store sales have rebounded. Regulatory policy, tax policy, monetary policy and even international policy must encourage this supply-side growth, not thwart it, if the economy is to continue to grow and create jobs.

As the Wall Street Journalreported and I tweeted yesterday, Senators Chuck Schumer and Patrick Toomey made important news when they agreed that with the new Coronavirus relief legislation, “the $429 billion would be revoked and the Fed wouldn’t be able to replicate identical emergency lending programs next year without congressional approval”

This is a welcome development because it is a start on the best monetary road back to a stronger economy. With the vaccines on the way and with markets functioning again, this is the time for the Fed to get back to a more rules-based monetary policy that it was moving toward before the pandemic struck.

This favorable development owes much to the outspoken insistence and careful reasoning of Senator Toomey. He argued that the Fed’s new direct lending programs enacted earlier this year were not needed going forward, and that their very existence blurred in dangerous ways the operation of fiscal and monetary policy. As Toomey explained on Squawk Box this morning in an interview with Becky Quick, “These facilities were always intended to be temporary…. Their purpose was to restore normal functioning in the private capital and lending markets.”

He then explained that questionable interpretations of the legislation had been recently put forward raising doubts about this temporary status. So he took action, and he drafted legislative language to clarify the situation in the coronavirus relief bill. The concern was that monetary policy would become an instrument of fiscal policy to the severe detriment to good economic policy and thereby threaten a return to a strong, low-unemployment, low-inflation economy. With new legislative language, he said, “The good news is these programs will be the temporary facilities they were intended to be.”

As an editorial in the Wall Street Journal said today: “The best provision in the bill is the limit on potential abuse by the Biden Treasury and Federal Reserve. Credit here to Pennsylvania Sen. Pat Toomey, who held firm on limiting the Fed’s maneuvering room without a new act of Congress.”

I hope this action is an important down payment on a return to a more strategic monetary policy going forward. As far as we can tell, the impetus for this change did not come from the Fed. But it is good news for the Fed that members of congress are supporting a more rules-based monetary policy, and they may even have some help next year from the Administration over at the Treasury.

Yes, America must prioritize in-person K-12 elementary and secondary schools as soon as it is safely possible. Quality in-person learning is essential.

But America must also increase on-line access whether or not in-person schools open now or later Data available since the start of the pandemic has revealed a big educational divide in on-line access. It is much less available for people who have low income.

Unfortunately, the in-person versus on-line issue has become polarized politically with the presidential campaigns and other campaigns staking out strong positions on one side or the other. But the choice should not be between in-person and on-line access. We need both.

The task is daunting and the road ahead is full of challenges, but there are several good solutions available and bridging the divide has never been more pressing. Our paper shows that there are many policies which increase access both on-line and in-person.

Many of them are part of proposals made by the executive branch and by legislators in Congress. Many are part of state and local proposals. Many are from the private sector, and they would thrive with good school choice legislation. But whether federal, state, local or private, it is a national security and economic imperative.