Today the Federal Open Market Committee described its upcoming plans for the federal funds rate through 2023. It is good, as I wrote last month on this blog that “Rules Are Back In The Fed’s Monetary Policy Report,” after a short absence, but it would more helpful if the Fed incorporated some of these rules or strategy ideas into its actual decisions.

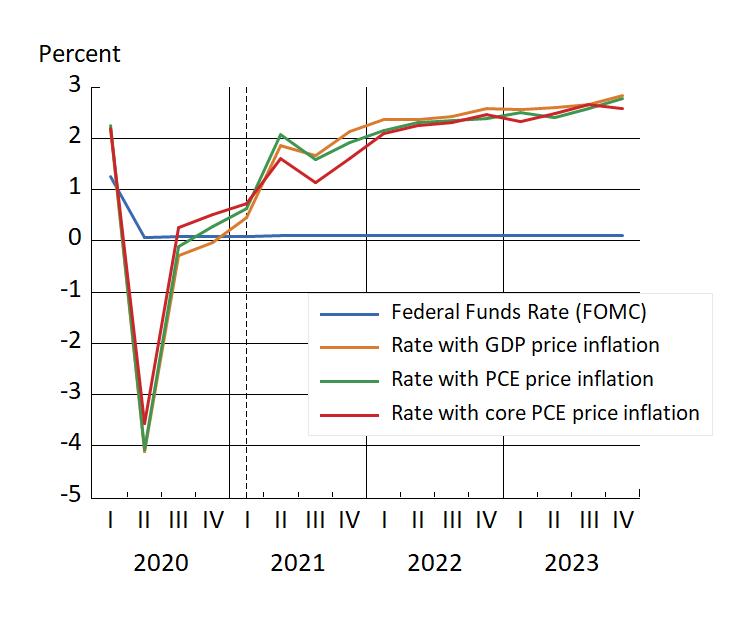

Apparently this did not happen, as the chart below shows. The chart gives the FOMC’s projection of the federal funds rate and three different rules-based paths for the federal funds rate through 2023. This FOMC projection is the “value of the midpoint of the projected appropriate target range for the federal funds rate or the projected appropriate target level for the federal funds rate at the end of the specified calendar year,” as stated in Table 1 of the Fed’s Summary of Economic Projections.

The three other rate paths show the federal funds rates from three policy rules using the same parameters as those in the Taylor rule–discussed in the Monetary Policy Report–with the so-called equilibrium interest rate reduced from 2 percent to 1 percent, as has been suggested at the Fed. The three policy rules use the four-quarter inflation rates of the GDP price index, the PCE price index, or the core PCE price index, based on the most recent Congressional Budget Office (CBO) projections. They use the same percentage deviation of real GDP and from potential GDP as in the CBO report. Most other forecasters do not have inflation and real GDP much different from CBO.

Even with this smaller equilibrium interest rate, the Fed’s path for the federal funds rate is well below any of these policy rules. There is a difference now (in the first quarter of 2021), and the difference grows over time.

There is no mention of why the discrepancy exists between the Fed’s actual decisions and the rules. Does this mean that the Fed will actually keep the rate this low under these circumstances regarding real GDP and inflation? Will it then raise the rate sharply in 2024? Taken literally, this is the implication because there is no indication that the Fed will do otherwise. I see no reason why the Fed could not be indicating now that its strategy is to raise policy interest rate as economic growth increases and inflation rises. Such an interest rate strategy would clarify the Fed’s monetary policy and facilitate the market adjustment when it takes place. So would a strategy for asset purchases and other aggregates.