The Federal Reserve’s latest Monetary Policy Report just released on February 19, 2021 has a whole section on monetary policy rules. That policy rules are back in the Report is a very welcome development. It re-initiates a helpful reporting approach that began in the July 2017 Monetary Policy Report, as I discussed here, when Janet Yellen was Fed chair. The approach continued under Chair Jay Powell in 2018, 2019 and early 2020, but it was dropped in July of last year. The good news is that it is back.

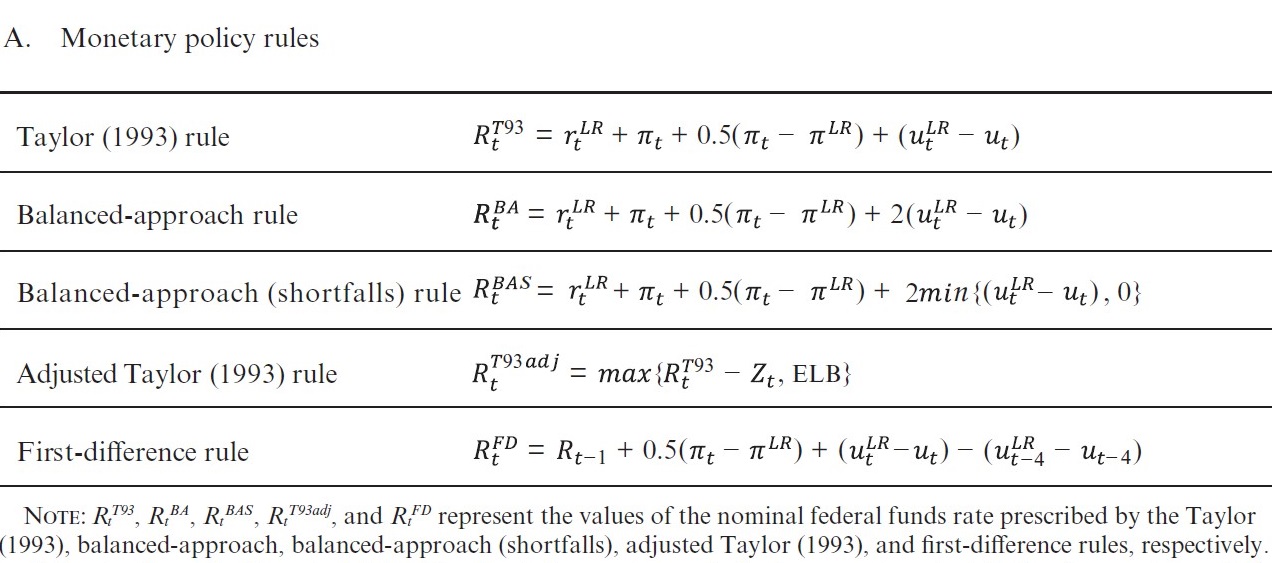

Five rules are discussed in the February 2021 Monetary Policy Report, especially on pages 45 through 48. To quote the Report, these include “the well-known Taylor (1993) rule, the ‘balanced approach’ rule, the ‘adjusted Taylor (1993)’ rule, and the ‘first difference; rule. In addition to these rules” and this is very important, there is a new “‘balanced approach (shortfalls) rule,’ which represents one simple way to illustrate the Committee’s focus on shortfalls from maximum employment.” Here is a table of rules from the Report:

There were also five rules on the earlier Reports, but one is out and a new one–the Balanced-approach (shortfalls) rule–is in. As stated in the document this modified simple rule “would not call for increasing the policy rate as employment moves higher and unemployment drops below its estimated longer-run level. This modified rule aims to illustrate, in a simple way, the Committee’s focus on shortfalls of employment from assessments of its maximum level.”

How much different would this shortfalls rule be compared with the regular balanced-approach rule? There is a helpful graph in the Report which answers this question. I have magnified a portion of that graph below so it is easier to see. Notice that the balanced-approach (shortfalls) rule is below the balanced-approach rule in 2017 through the start of the pandemic in 2020. This is the period when the actual unemployment rate in the United States is lower than the estimate of the long-run unemployment rate. Thus the shortfalls rule does not increase the interest rate as does the balanced approach rule without the shortfall. The rule in between these two in the graphs is the Taylor rule. The shortfalls and the non-shortfalls rule then move together during the start of the pandemic as the unemployment rate rises well above the long run rate. The adjusted Taylor rule stays above zero, but then will stay low for longer than the Taylor rule.

The important contribution of this new discussion is that one now has an explicit way to think about the Fed’s new “shortfalls from maximum employment” approach. One can see if the new rule performs better that the balanced approach or the modified Taylor rule, for example, by simulating models. A huge amount of research can take place both outside as well as inside the Fed. There is much work to do. So let’s get going!

While this is an excellent start, more could be done. It is a bit disappointing, for example, that, as the Report says, the aims “of having inflation average 2 percent over time to ensure that longer term inflation expectations remain well anchored, are not incorporated in the simple rules analyzed in this discussion.” This is a very important issue and may be the subject of future Fed Reports.