Last week, after attending monetary policy conferences at Stanford, Chicago and Frankfurt, I put forth evidence in EconomicsOne.com of a revival of research on monetary policy rules for the instruments, whether at the conferences, in research papers, or in Fed publications. I offered possible explanations for the revival, also with evidence, including revealed preference by policymakers, the need to deal with the effective lower bound, disappointments with past departures from rules, threats of legislation, and concerns about political pressure.

This week, Peter Ireland posted an article with a carefully worked-through analysis of recent actual monetary decisions, which takes the idea of the Fed using policy rules for the instruments a significant step further, well beyond research papers and into policy arena.

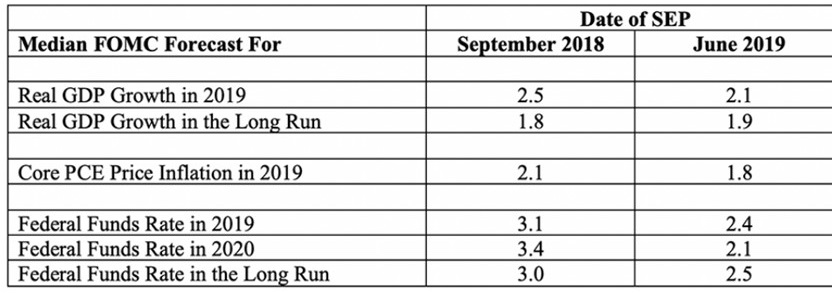

In the article, entitled A Rule That Makes Sense of the Fed, Peter examines recent changes in the Fed’s interest rate target, and he shows they are consistent, according to the Taylor Rule, with changes in real GDP, inflation, and r-star. Going line-by-line through the table below (which I draw from his article)

he shows the Fed’s Summary of Economic Projections (SEP) and demonstrates how a change in the federal funds rate from September 2018 to June 2019 can be explained, via a Taylor Rule, by changes in real GDP, the core PCE inflation rate, and r-star over the same period.

Peter thereby demonstrates that the Fed could be more explicit that these decisions are rules-based. In this way, he shows that “policymakers could explain more easily that the substantial downward adjustment to their expected interest-rate path represents a deliberate response to changes in their outlook for economic growth and inflation, together with their best judgement that r-star is considerably lower than previously thought. Even more important, they could use the Taylor Rule to demonstrate that their interest rate decisions are driven by economic analysis alone and not influenced by political pressure.”

It is another reason for Fed policymakers and other central bank official to strive to make their decisions within a rules-based framework, which can be analyzed with economic models, checked for robustness, and integrated internationally.