An old, but forever crucial, question for monetary policy is whether it should be rules-based or purely discretionary. The Economist, in a Free Exchange article this week with the title “Rule It Out,” goes all in for pure discretion, abandoning rules-based strategy. It’s a new view compared to previous articles over the years in the magazine and, more importantly, not based on any new facts.

The article’s main mode of argument is to invent and then shoot down straw men. It argues, for example, that “Algorithms…should not supplant central bankers” even though no proposal out there suggests anything of the kind. It asserts that a rules-based policy is an “unnecessary constraint” on central bank “autonomy,” when experience shows that clear strategies and principles help defend autonomy. Strangely, it says that sensible flexibility built into rules-based policy demonstraes its “pitfalls” which are then never even mentioned. The article is so infatuated with unlimited discretion that it even argues that if the Congress wants oversight it would be better to designate another purely discretionary body to give opinions about monetary policy than to ask the central bank to report on and be accountable for its own policy rule or strategy.

In trying to justify discretionary policy the article discusses the Taylor rule in detail, adding a Taylor rule chart cutely labeled “Dropping Stitches;” in doing so it repeats arguments that have been refuted or discounted many times over the years. It says that “interest rates should be lower than the Taylor rule suggests” because “many economists suspect [the long-term real interest] rate is permanently lower,” and it says that “Estimates of slack are themselves the product of qualitative judgment…” Debates over the long-term rate and the degree of slack are fine to have, but the issues create no more difficulty for rules-based policy than for pure discretion. In fact, a rules-based policy is preferable in this regard because it provides a way to consider the implications of, and to resolve disagreements about, such issues without sweeping them under the rug. A policy rule is not “a recipe for disagreement,” as the article claims, it is a reasonable way to discuss and resolve disagreements.

I got a little bit of déjà vu about the discussion of the Taylor rule in the article, and decided to look back at previous articles in the magazine. In fact, The Economist has published quite a few articles and charts about the Taylor rule over the years, but, completely unlike the article this week, those articles used the rule in a constructive way to discuss and take positions about monetary policy.

I recalled a piece published in The Economist almost two decades ago entitled “Monetary Policy, Made to Measure” (August 1996) with a chart labeled (yes, you guessed it) “Well Taylored.” It asked if there was a rule “which will tell central bankers how to adapt their policies…” and then described the Taylor rule as “one such rule…” It discussed the uncertainty about the “neutral” interest rate and the “output gap” in the rule and recognized that the rule “includes only part of the information available to central banks,” which meant that such a rule should not be used mechanically without central bankers exercising discretion in its implementation—a view of rules-based policy that I expressed clearly when I introduced the rule a few years earlier and continue to hold. Nevertheless, the 1996 Economist article used the rule—as many others were doing—to make the case that monetary policy was about right in several countries at the time.

Then there was the famous period when The Economist criticized the Fed for deviating from rules-based policy. The article “Nicely Taylored?” from November 2004 used the rule to suggest that interest rates ought to have been rising faster. Then, later looking back at that period from the vantage point of August 2007, The Economist argued that “By slashing interest rates (by more than the Taylor rule prescribed), the Fed encouraged a house-price boom.” In “Tangled Reins” (September 2007), The Economist warned that “the Fed’s efforts to exude a cowboy confidence will be undermined by the suspicion that it is dealing with the consequences of its own errors.”

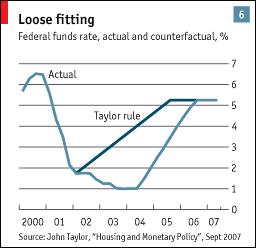

And in “Fast and Loose” (October 2007) it came down very hard on the Fed for deviating from rules-based policy. The article noted that “Of course the Taylor rule is only a rough guide. The neutral rate and the output gap, in particular, cannot be measured precisely.” And it then went on to say, “But the rule can tell you whether policy is roughly right or a long way out. The Fed missed by a mile.” The article illustrated the point with this “Loose Fitting” chart.

None of this history of The Economist writings on the harm caused by discretionary deviations from rules-based monetary policy is mentioned in this week’s article except to say that Taylor “thinks” such a scenario was possible. My brief review here is not meant, of course, to be a call for the magazine to be consistent over time if facts change, and besides it was fun to recall the clever titles (Monetary Policy, Made to Measure; Well Taylored; Nicely Taylored; Tangled Reins, Fast and Loose, Loose Fitting, Rule It Out, Dropped-Stitching). But what facts have changed to lead to such a change of view? If anything there is more evidence that departures from rules-based policy are harmful (David Papell et al) or at best useless (John Hussman). And I note with interest that Clive Crook, who wrote and was Deputy Editor for The Economist in those earlier years, recently wrote two Bloomberg View columns “The Fed Needs Some Guidance” and “Dreaming of Normal Monetary Policy” making the case for rules-based policy.