Scare stories about the automatic reduction in federal spending to start on March 1—commonly called the sequester—fall mainly into two categories. First are the concerns that reducing every discretionary budget account by the same percentage—the “meat-axe” approach—would not allow government agencies to prioritize. Hence the scare stories of having to furlough key emergency personnel. But this complaint is easily resolved if President Obama agrees to give agencies, including defense agencies, the flexibility to adjust their budgets within the overall sequester totals. Most Republicans in Congress would agree to this.

Second, the size of the total spending reduction for FY2013 is said to be too big and will slow down the economy. But if you put the reduction into perspective, as in the following chart, you can see that this claim is greatly exaggerated and likely to be false.

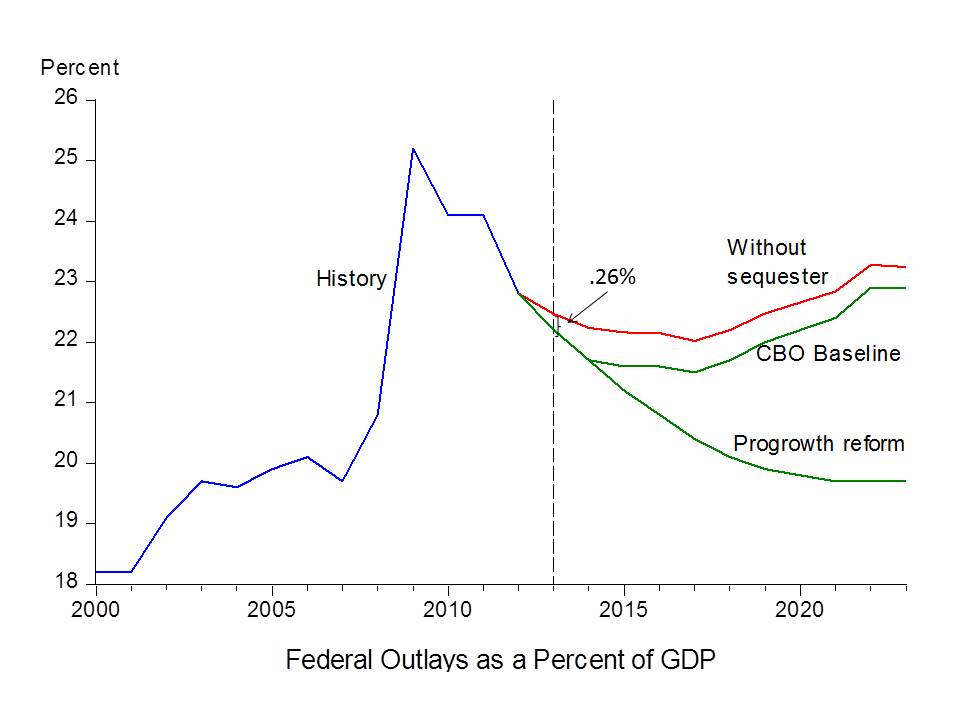

The chart shows federal outlays as a share of GDP as reported by the Congressional Budget Office in their latest budget outlook report. The past history and CBO baseline shows spending rising from 18.2% of GDP in 2000 and remaining relatively high at 22.8% of GDP in 2023 the last year of the CBO outlook. That baseline includes the sequester totals, so if Washington caves and reduces the size of the spending reductions, spending will be higher as shown in the graph.

Note that the reduction for 2013—the year currently under discussion—is very small relative to all the other changes in the budget during the quarter century period shown in the graph. It amounts to only 0.26% of GDP or $42 billion according to CBO. This is less than half the frequently mentioned $85 billion in Budget Authority because it takes time to bring about the outlay reductions. The reduction is also quite gradual, much more gradual than the sudden rise in spending in the past few years, and, with flexibility granted to government agencies, does not have to be draconian. The Administration and Congress agreed to roughly this amount of budget deficit reduction way back in 2011.

Note also that the reduction for this year should be viewed as a modest installment on an overall long-term strategy to bring the federal spending share down to levels consistent with balancing the budget. We do not yet know what that strategy will be because the Administration has not submitted a budget and thus the Congress has not submitted budget resolutions. We do know that for that strategy to increase rather than decrease economic growth it is important that it be gradual and credible as illustrated by the “pro-growth” proposal which I sketched into the diagram above. This pro-growth path brings spending to where it was in 2007 as a share of GDP and would also bring the federal budget roughly into balance—and thus get the debt to GDP ratio on a needed downward path—without any more tax increases. CBO now projects revenue to be just over 19% in 2023 with the recent tax increases.

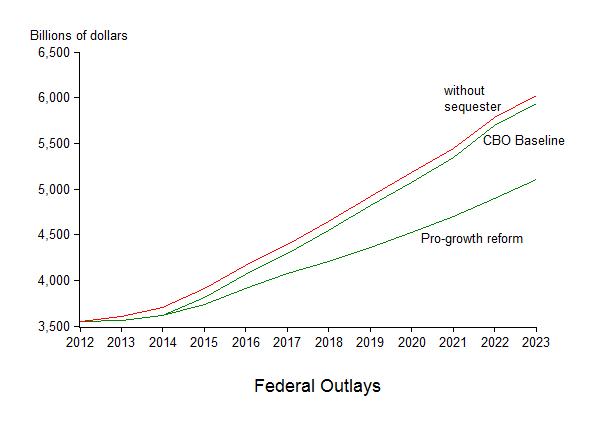

Research discussed here shows that such a path would increase economic growth even with the reduced spending share in 2013. Indeed, as shown in the next graph total federal spending continues to grow according to the CBO GDP forecast.

Whether we get a strategy similar to what I propose here or something else, the diagram shows that postponing or skipping the relatively small installment for 2013 would sap much of the credibility out of any budget consolidation strategy. From a macroeconomic perspective, providing the agencies with flexibility but sticking with the overall totals agreed to would be best for economic growth.