Want to understand what really goes on behind the scenes of the supply and demand model? Read this wonderful clear essay by Russell Roberts. It explains how prices provide information, coordinate, and motivate decisions with many more details than in the summaries of Adam Smith and Milton Friedman in my October 3 post.

Two Masters Speak on Power of Markets

The “free market” lectures–we had them last week at Stanford–are my favorites in Economics One. I wear this Adam Smith tie, give a short summary of Smith’s writings, read his story of the woolen coat from the pages of his Wealth of the Nations, and then we all watch Milton Friedman’s two-minute pencil lecture on YouTube, where you can see that he also wore an Adam Smith tie. We then dive into the technical explanation of how with competitive markets the price system leads to an efficient allocation of resourses and production. I only wish Smith were on YouTube. Next week we consider monopoly, which is not a story of efficiency.

The “free market” lectures–we had them last week at Stanford–are my favorites in Economics One. I wear this Adam Smith tie, give a short summary of Smith’s writings, read his story of the woolen coat from the pages of his Wealth of the Nations, and then we all watch Milton Friedman’s two-minute pencil lecture on YouTube, where you can see that he also wore an Adam Smith tie. We then dive into the technical explanation of how with competitive markets the price system leads to an efficient allocation of resourses and production. I only wish Smith were on YouTube. Next week we consider monopoly, which is not a story of efficiency.

Posted in Teaching Economics

Comments Off on Two Masters Speak on Power of Markets

A Beautiful Model, A Clear Prediction

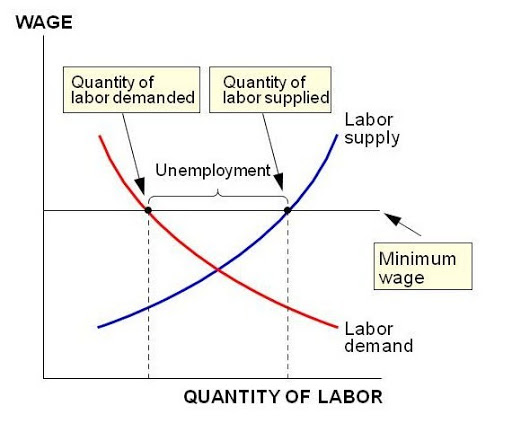

The supply and demand model, which students learn in the first week of Economics One, is a beautiful, powerful tool for investigating real world issues like the minimun wage, the subject of tomorrow’s Wall Street Journal editorial. The model’s prediction is chrystal clear as this little diagram from my lectures shows: a minimum wage causes unemployment, especialy for young unskilled people, just as the Journal argues. Of course the size of the impact depends on the steepness or elasticity of labor demand. So empirical research by economists like David Neumark and Bill Wascher cited in the Journal is essential. Their research is described in this box from my Principles of Economcs book. The research shows the impact to be quite significant. But as is so often the case in economics, not all economists agree, so the box also describes some contrary findings by David Card and Alan Krueger. I side with Neumark and Wascher in this debate, but you can read the editorial, look at the diagram, read the box, and draw your own conclusions.

The supply and demand model, which students learn in the first week of Economics One, is a beautiful, powerful tool for investigating real world issues like the minimun wage, the subject of tomorrow’s Wall Street Journal editorial. The model’s prediction is chrystal clear as this little diagram from my lectures shows: a minimum wage causes unemployment, especialy for young unskilled people, just as the Journal argues. Of course the size of the impact depends on the steepness or elasticity of labor demand. So empirical research by economists like David Neumark and Bill Wascher cited in the Journal is essential. Their research is described in this box from my Principles of Economcs book. The research shows the impact to be quite significant. But as is so often the case in economics, not all economists agree, so the box also describes some contrary findings by David Card and Alan Krueger. I side with Neumark and Wascher in this debate, but you can read the editorial, look at the diagram, read the box, and draw your own conclusions.

Posted in Teaching Economics

Comments Off on A Beautiful Model, A Clear Prediction

The Best Economics 1 Lecturer Ever

I decided to invite a young guest lecturer to my Economics 1 class to help students think about the alarming federal debt charts and the exploding debt burden on future generations. She stole the show. Here is a video of some excerpts. I play a supporting role.

Posted in Teaching Economics

Comments Off on The Best Economics 1 Lecturer Ever

The Best Economics 1 Lecturer Ever

I decided to invite a young guest lecturer to my Economics 1 class to help students think about the alarming federal debt charts and the exploding debt burden on future generations. She stole the show. Here is a video of some excerpts. I play a supporting role.

Posted in Teaching Economics

Comments Off on The Best Economics 1 Lecturer Ever

The Real Anniversary

Two weekends ago the big news was the one-year anniversary of the Lehman Brothers bankruptcy and the ensuing panic. But when you look at the data, the real one-year anniversary of the panic is closer to now.

In the four weeks from Friday September 12, 2008, just before the Lehman bankruptcy, through Friday October 10, the S&P 500 fell by a huge 28 percent. But the decline was relatively modest (3 percent) in the first two weeks of that period, from September 12 to September 26, a year ago today. It is not unusual to see that size of change in a one or two week period. The real panic (the remaining 25 percent of that 28 percent decline in the S&P 500) occurred later, from September 26 to October 10. If you look at interest rate spreads or stock prices in other countries you see the same timing. Such facts have led me and others to be skeptical about the commonplace claim that it was simply the decision not to intervene and bail out Lehman’s creditors that triggered the panic. Rather I focus on the chaotic rollout of the TARP which began later and continued through October 13 when its ultimate use was finally defined.

This view is laid out in Getting Off Track as well as in a Wall Street Journal column by John Cochrane and Luigi Zingales and an Arizona Republic column by Robert Robb. An event study using the S&P 500 is in this box from the new Global Financial Crisis Edition of my Principles of Economics with Akila Weerapana.

Posted in Financial Crisis

Comments Off on The Real Anniversary

Why Triple IMF Resources Now?

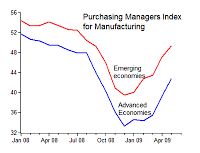

As the G20 Leaders travel to Pittsburgh this weekend they should reconsider their April 2 decision “to treble the resources available to the International Monetary Fund (IMF) to $750 billion.” Why? First, the IMF does not need the money: as the first chart shows, it has loaned only a small fraction (7%) of the targeted $750 billion, even less than it loaned in severe emerging market crisis period of 1995-2003. (The IMF uses SDRs to measure loans: SDR= $1.6). Second, emerging market economies have recovered from the worst of the financial crisis. In fact, according to the purchasing managers index shown in the other chart, they bottomed out in December of last year, well before the April G20 decision to treble resources. Third, providing too many resources to any government institution can be harmful. Discipline is lost without a budget constraint. Even with the best intentions, resources are wasted or misused. Excess resources become a slush fund leading to mission creep, unpredictable policies, and more crises. For more details on the data in the charts see my essay in the useful book edited by Alexei Monsarrat and Kiron Skinner prepared for the G20 meeting.

As the G20 Leaders travel to Pittsburgh this weekend they should reconsider their April 2 decision “to treble the resources available to the International Monetary Fund (IMF) to $750 billion.” Why? First, the IMF does not need the money: as the first chart shows, it has loaned only a small fraction (7%) of the targeted $750 billion, even less than it loaned in severe emerging market crisis period of 1995-2003. (The IMF uses SDRs to measure loans: SDR= $1.6). Second, emerging market economies have recovered from the worst of the financial crisis. In fact, according to the purchasing managers index shown in the other chart, they bottomed out in December of last year, well before the April G20 decision to treble resources. Third, providing too many resources to any government institution can be harmful. Discipline is lost without a budget constraint. Even with the best intentions, resources are wasted or misused. Excess resources become a slush fund leading to mission creep, unpredictable policies, and more crises. For more details on the data in the charts see my essay in the useful book edited by Alexei Monsarrat and Kiron Skinner prepared for the G20 meeting.

Posted in International Economics

Comments Off on Why Triple IMF Resources Now?

Alarming Debt Charts

Simple charts vividly demonstrate the immensity of the exploding debt problem now faced by the United States. The large expansion of debt in World War II looks like a small blip compared to what’s coming if we do not change policy. Click here to see the charts I used to compare U.S. debt history with CBO projections in my Economics lectures at Stanford today. The source is the spreadsheet for CBO’s alternative fiscal scenario in its June Long-Term Budget Outlook.

Posted in Budget & Debt

Comments Off on Alarming Debt Charts

The Crisis: A Failure or a Vindication of Economics?

Today was the first lecture of thirty-five or so lectures I will give this fall in Stanford’s Economics 1, the namesake of this Blog. Enrollment is way up. The financial crisis is naturally generating a great deal of interest in economics.

In the meantime, the financial crisis is generating a great deal of hand-wringing and debate among economists about their subject. This summer a cover of The Economist magazine shows a book titled “Modern Economic Theory” melting into a puddle to illustrate “What Went Wrong with Economics.” It was the most talked about issue of the year. This is an important debate, and the different positions deserve to be covered in the basic economics course.

Some economists are calling for a complete redo of economics—or for a return to a version of the subject popular thirty years ago. They say that economics failed to prevent the crisis or even led to it. Many of these economists argue for a more interventionist government policy, saying that John Maynard Keynes was right and Milton Friedman was wrong. Paul Samuelson was one of the first to speak out this way, saying in January in an interview in the New Perspectives Quarterly (Winter 2009), “today we see how utterly mistaken was the Milton Friedman notion that a market system can regulate itself… This prevailing ideology of the last few decades has now been reversed…I wish Friedman were still alive so he could witness how his extremism led to the defeat of his own ideas”. Paul Krugman’s longer piece two weeks ago in the New York Times Magazine (September 7, 2009) started off another round of debate. He faults modern economics (espeically modern macroeconomics) for bringing on the crisis. He says it focuses too much on beauty over practicality and does not recognize the need for more government intervention to prevent and cure the crisis. His fix is to add more psychology to economics or to build better models of credit.

But there are other opposing views to cover. In my view, the financial crisis does not provide any evidence of a failure of modern economics. Rather the crisis vindicates the theory. Why do I say this? Because the research I have done shows that the crisis was caused by a deviation of policy from the type of policy recommended by modern economics. It was an interventionist deviation from the type of systematic policy that was responsible for the remarkably good economic performance in the two decades before the crisis. Economists call this earlier period the Long Boom or the Great Moderation because of the remarkably long expansions and short shallow recessions. In other words, we have convincing evidence that interventionist government policies have done harm. The crisis did not occur because economic theory went wrong. It occurred because policy went wrong, because policy makers stopped paying attention to the economics.

Posted in Financial Crisis

Comments Off on The Crisis: A Failure or a Vindication of Economics?

Is the Stimulus Working?

My recent Wall Street Journal column with John Cogan and Volker Wieland looked at the data available so far and concluded that there has been no noticeable impact. CNBC’s Steve Liesman takes the other side in a debate with me on the the Kudow Report last Thursday.

My recent Wall Street Journal column with John Cogan and Volker Wieland looked at the data available so far and concluded that there has been no noticeable impact. CNBC’s Steve Liesman takes the other side in a debate with me on the the Kudow Report last Thursday.

Many asked me how we control for other factors, such as oil prices, in such studies; the answer is to use regression techniques as in this AEA paper. A contrast between Keynesian and more modern macro models is found in this robustness analysis by Cogan, Cwik, Taylor, and Wieland

Posted in Stimulus Impact

Comments Off on Is the Stimulus Working?