Two years ago, on Friday Sept 12, 2008, the Lehman Weekend began. Many people are still trying to figure out why the bailout of Lehman was aborted or what would have happened if there were a special bankruptcy chapter for such financial institutions. Books have been written about the Weekend including Sorkin’s Too Big To Fail and more will be written. The Dodd-Frank bill’s requirement for a Fed audit will reveal more. In my view one of the most informative writings is the Lehman Bankruptcy Examiner’s report, based on extensive interviews and examination of documents. The whole report is quite long (thousands of pages), so I thought it would be useful to prepare this excerpt which focuses only on the events of that weekend.

Flying Back to Treasury on 9/11

I was in a hotel room in Tokyo when the first plane hit the World Trade Center. Recently sworn in as Under Secretary at Treasury, I was part of a delegation to Japan that included Paul O’Neill and many reporters, including Michael Phillips of the Wall Street Journal. We all watched the tragedy on television. I got very close—it seemed like inches—to the TV screen. When the first tower started collapsing I looked up from the screen to see faces of horror, disbelief, for some reason noticing, and now remembering, Michael Phillips’ look of utter shock. No one knew it then but Michael would later do five tours in Iraq imbedded with the Third Battalion, Seventh Marines and would write a moving book in 2005, The Gift of Valor, about a young Marine corporal, who sacrificed his life to save his fellow marines, a great American hero in what would come to be the global war on terror. The Marine, Jason Dunham, was awarded the Medal of Honor in 2006.

We immediately cancelled our meetings in Japan and by the next morning—still 9/11 in the United States—we were on a C-17 military jet flying back to America. The plane ride back from Japan was eerie. A C-17 is about as long as a DC-10, but when you’re inside it seems much bigger and more cavernous—an “echoing belly” is how General Tommy Franks described it—designed to hold tanks and other large military equipment. The only passenger seats are straight-backed canvas jump seats bolted along the metal wall of the fuselage. Unable to lie down or even slouch in those seats, some of us simply spread out on the cold bare metal deck when we wanted to sleep.

To get back faster we had an aerial refueling over Alaska. It took place at night, though at that latitude and elevation it seemed like perpetual twilight. The Air Force pilot invited me to watch the refueling from the cockpit, and it was amazing—the most impressive combination of advanced technology, hand-eye coordination, precision teamwork, and raw nerve that I had ever observed.

The rendezvous with the tanker jet had been arranged when the flight plan was put together in Japan. When we got close to the designated time and place, the pilots started looking for the tanker, which was to fly up from a base in Alaska. They first located the tanker plane on radar. Soon after that, they got visual contact. The co-pilot said to me, “See it, sir? It’s right out there.” But I couldn’t see a thing except stars and the twilight at the horizon.

Our plane was to approach the tanker from underneath, and as we got closer to the tanker the small speck the pilots could see grew until suddenly there was this huge jet plane only a few feet above us. Our pilot was using a specially-designed joy stick with a monitoring device consisting of rows of lights that turned red or green depending on whether our plane was coming up at the right position relative to the tanker. It reminded me a lot of a computer game, but this was for real. These two huge jets were zooming through the dark at something like 500 miles per hour, so it was amazing to me, though seemingly routine to those pilots, that the planes were close enough to each other that I could see the faces of the guys in the tanker as they lowered the fuel hose and somehow got it to go into the opening in our fuel tank. After a while the tank registered full and the hose was pulled back in, the tanker disappeared into the night, and we headed home across Canada. As we flew into the lower 48 there were no commercial flights to be seen. The plane’s radar screen was nearly blank.

That remarkable night time aerial refueling would mark a watershed for me and my responsibilities at Treasury. It was the beginning of a much closer cooperation and coordination with the Defense Department and with the U.S. military. It was also the start of many completely new experiences that I could never have expected when I signed up for a job in Treasury. I suppose I could have gotten a little spooked being in that cockpit but I felt very calm, kind of resigned to a new purpose where I would be forging new teams to handle new tasks, and I would be relying on the expertise and experience of others—people like these pilots—and they would be relying on mine. I slept well that night on the steel deck. Months later when I would fly on other military planes—C-130 transports in Afghanistan, Blackhawk helicopters in Iraq—I would always feel just as calm, even at the times when it looked like I was in harm’s way.

When I got back to Washington, the city was on alert. DC was a logical place for another attack, and the secret service was particularly concerned about security around the White House and the adjacent buildings which included the Treasury. We planned for the worst case scenarios. We made lists of essential jobs that would have to be done if the Treasury was wiped out—running the $30 billion Exchange Stabilization Fund in case we had to intervene in the currency markets was an example. We visited the remote locations that we would live in if the Treasury Building was destroyed, developed plans for continuity of operations and continuity of government, and reviewed the order of succession. We cancelled the annual meetings of the IMF and World Bank, which had been scheduled to be held in Washington on September 29th and 30th. Our intelligence experts expected large groups of protestors and a meeting with thousands of foreign financial officials, bankers, and press would have severely stretched the already overextended Washington security forces. And we had many other things to do.

Condensed from Global Financial Warriors

Posted in International Economics

Comments Off on Flying Back to Treasury on 9/11

Post-Crisis Changes in Principles of Economics Texts

Many have written about how the introductory economics textbook should change as a result of the crisis.

In November 2008, one year after the crisis started, I addressed this question in a practical way when Mike Worls—economics editor at South-Western Cengage, publisher of my principles text with Akila Weerapana—asked if we would write a new crisis edition of our book. We agreed, started work immediately, and published the first post-crisis principles of economics text in the summer of 2009, with such additions as the role of government in the crisis, quantitative easing, zero bound on interest rates, small impact of the 2008 fiscal stimulus, moral hazard, housing bubbles, etc.

Then, two years after the crisis, Alan Blinder addressed the question at the American Economic Association meetings last January explaining how he would change his textbook by, for example, giving more emphasis to short run Keynesian issues and adding in securitization.

Now, three years after the crisis, Paul Gregory addressed the question in a new thoughtful post on his blog. Paul’s piece benefits greatly from the additional evidence that the 2009 stimulus packages had little effect with unemployment still quite high three years after the crisis began. He takes a decidedly non-Keynesian approach, reinforcing his earlier textbook with Roy Ruffin.

Soon Akila and I will be doing another edition with the benefit of even more information, perhaps the first second-edition post-crisis principles of economics text.

Posted in Teaching Economics

Comments Off on Post-Crisis Changes in Principles of Economics Texts

More on Massive Quantitative Easing

In tomorrow’s Wall Street Journal there is a symposium on monetary policy in which Richard Fisher, Rick Mishkin, Vince Reinhart, Allan Meltzer, Ron McKinnon and I participate. One of the points I make in my piece is that another massive dose of quantitative easing is not appropriate now. I briefly explained the rationale for this point of view in a post on this blog several days ago, where I referred to Milton Friedman’s advocacy of stable monetary policy rules. A number of people wrote to ask me about that post, and Scott Sumner has written a thoughtful blog entry about it, quoting Milton Friedman on Japan.

I completely agree that the problems in Japan in the 1990s stemmed from a sharp decline in money growth compared with the 1980s, from 8.9 percent per year during 1980.1–1991.4 to 2.6 percent per year during 1992.1 – 2000.1 as shown in the Table and Chart in this speech I gave at the Bank of Japan. This decline in money growth was a discretionary action which Friedman, Allan Meltzer, and others rightly criticized. This criticism is quite consistent with Friedman’s view that we should avoid large discretionary changes in money growth and instead follow a constant money growth rule. To correct this mistake of a sharp decline in money growth, Friedman recommended that the Bank of Japan increase money growth but “without again overdoing it,” presumably taking money growth back to the more appropriate levels of the 1980s.

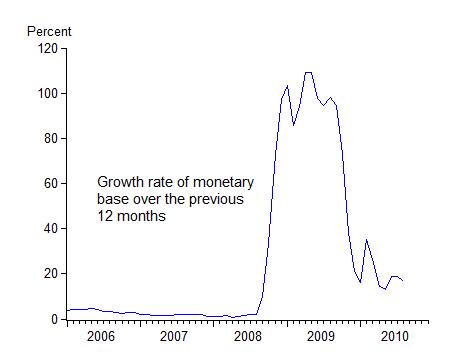

Now consider the current situation in the United States. We did not see the same kind of decline in money growth as in Japan going into the recent recession. The US recession began in December 2007. Measured over 12 month periods, M2 growth rose from 4.8% in January 2006 to 5.9% in January 2007 to 6.0% in January 2008 to 10.4% in January 09. Then, as a result of quantitative easing, which began in September 2008, the growth rate of the monetary base (using the same 12-month measure) increased from 2 percent to over 100 percent which helped increase the growth rate of M2 and other monetary aggregates.  See chart. Now as the size of the Fed’s balance sheet did not keep growing at such a rapid pace, the growth rate of the monetary base (and M2) has declined. Another large dose of quantitative easing would again send the growth rate of money soaring, but then only to decline again as it has recently. So quantitative easing as practiced by the Fed has increased the volatility of money growth significantly.

See chart. Now as the size of the Fed’s balance sheet did not keep growing at such a rapid pace, the growth rate of the monetary base (and M2) has declined. Another large dose of quantitative easing would again send the growth rate of money soaring, but then only to decline again as it has recently. So quantitative easing as practiced by the Fed has increased the volatility of money growth significantly.

Money growth volatility is something Milton Friedman was surely against. In his Newsweek column of December 1, 1980 entitled “The Fed Fails—Again” he wrote “The key problem has been the erratic swings [in money growth] from one extreme to the other that have produced uncertainty in the financial markets and instability in economic activity.” On top of all this, my research shows that the impact of quantitative easing on mortgage rates or other long term borrowing rates has been quite small and statistically insignificant.

I hope this additional information is helpful.

Posted in Monetary Policy

Comments Off on More on Massive Quantitative Easing

Beyond GDP Measures Don’t Make the US Look Better

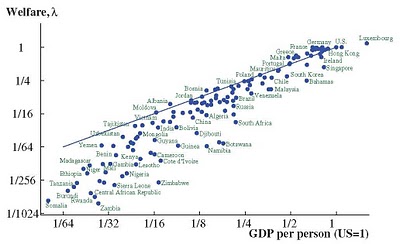

My colleagues Chad Jones and Pete Klenow have computed a new measure of economic welfare which combines consumption, leisure, mortality, and even inequality. Their new measure is closely correlated with GDP per capita as the attached diagram from their paper suggests. But there are differences. For example, income per capita in France is only 70 percent of that in the United States, while the new welfare measure for France is 97 percent of that in the United States. The difference is mainly due to more leisure and less income inequality in France. The gains and losses of utility from different levels of income inequality are based on the Rawls abstract concept of the veil of ignorance in which each person enters a lottery each year determining what country he or she will live in–one with less or more income inequality. Chad and Pete have a whole section on “caveats” in their interesting paper.

Posted in Teaching Economics

Comments Off on Beyond GDP Measures Don’t Make the US Look Better

Got a New Idea for Monetary Policy?

Do you have a new proposal for monetary policy? Perhaps a new policy rule? If so, it would be good to try out your idea first on a model of the economy. See how it works. Better yet, since economic models are different and economists frequently disagree, try it out in several models to be sure your rule is robust. But what models and how ?

Volker Wieland and his colleagues at Goethe University of Frankfurt are performing a valuable public service that makes it much easier to try out new policy ideas than it used to be when work on policy rules was first starting. They are creating an on-line model database containing monetary models used at the Fed, the ECB, and other central banks, including the Swedish Riksbank and the Central Bank of Chile, as well as the IMF and academia.

The models range in size from over 100 equation models to small three equation models (a policy rule equation for the interest rate, a staggered price setting equation for inflation, and an equation relating output to the interest rate). They all have inflexibilities, forward-looking expectations, and a policy analysis based on policy rules. So far there are 35 models in the database. Here is a list. For more information log into Volker Wieland’s model database and have some fun.

Models in the Database

1. Small Calibrated Models

1.1 Rotemberg, Woodford (1997)

1.2 Levin, Wieland, Williams (2003)

1.3 Clarida, Gali, Gertler (1999)

1.4 Clarida, Gali, Gertler 2-Country (2002)

1.5 McCallum, Nelson (1999)

1.6 Ireland (2004)

1.7 Bernanke, Gertler, Gilchrist (1999)

1.8 Gali, Monacelli (2005)

2. Estimated US Models

2.1 Fuhrer, Moore (1995)

2.2 Orphanides, Wieland (1998)

2.3 FRB-US model linearized as in Levin, Wieland, Williams (2003)

2.4 FRB-US model 08 linearized by Brayton and Laubach (2008)

2.5 FRB-US model 08 mixed expectations, linearized by Laubach (2008)

2.6 Smets, Wouters (2007)

2.7 CEE/ACEL Altig, Christiano, Eichenbaum, Linde (2004)

2.8 New Fed US Model by Edge, Kiley, Laforte (2007)

2.9 Rudebusch, Svensson (1999)

2.10 Orphanides (2003b)

2.11 IMF projection model by Carabenciov et al. (2008)

2.12 De Graeve (2008)

2.13 Christensen, Dib (2008)

2.14 Iacoviello (2005)

3. Estimated Euro Area Models

3.1 Coenen, Wieland (2005) (ta: Taylor-staggered contracts)

3.2 Coenen, Wieland (2005) (fm: Fuhrer-Moore staggered contracts)

3.3 ECB Area Wide model linearized as in Dieppe et al. (2005)

3.4 Smets, Wouters (2003)

3.5. Euro Area Model of Sveriges Riksbank (Adolfson et al. 2007)

3.6. Euro Area Model of the DG-ECFIN EU (Ratto et al. 2009)

3.7. ECB New-Area Wide Model of Coenen, McAdam, Straub (2008)

4. Estimated Small Open-Economy Models (other countries)

4.1. RAMSES Model of Sveriges Riskbank, Adolfson et al.(2008b)

4.2 Model of the Chilean economy by Medina, Soto (2007)

5. Estimated/Calibrated Multi-Country Models

5.1 Taylor (1993a) model of G7 economies

5.2 Coenen,Wieland (2002, 2003) G3 economies

5.3 IMF model of euro area & CZrep by Laxton, Pesenti (2003)

5.4 FRB-SIGMA model by Erceg, Gust, Guerrieri (2008)

Posted in Monetary Policy

Comments Off on Got a New Idea for Monetary Policy?

A Milton Friedman Revival

Bloomberg columnist Caroline Baum laments that monetarists have “followed Milton Friedman the grave.” Monetarist, of course, is a term used to identify those who agree with the ideas of the great free-market economist who died in 2006. But I see neither those ideas nor their adherents going to the grave. Indeed, the experience of this crisis is proving that Milton Friedman’s ideas were right all along, and I can see them gaining favor.

Two of Friedman’s most famous ideas in the macroeconomic sphere were (1) that monetary policy should follow a simple policy rule and (2) that discretionary fiscal policy is not useful for combating recessions, and indeed could make things worse. Both ideas have been reinforced by the facts during the recent crisis.

The first idea is reinforced by the evidence that the crisis was brought on by the failure of the Fed to keep following the rules-based monetary policy that had worked well for 20 years before the crisis. Instead, it deviated from such a policy by keeping interest rates too low for too long in 2002-2005. But Caroline Baum wonders whether the Fed should now just print a lot more money and buy more mortgages or other securities. That might sound like a monetarist solution, but Friedman did not believe in big discretionary changes the money supply. Rather, he advocated a constant growth rate rule for the money supply. I doubt that he would have approved of the rapid increase in the money supply last year, in part because he would have known that it would be followed by a decline in money growth this year. He always worried about monetary policy going from one extreme to the other and thereby harming the economy. That is why the Fed should be clear and careful as it brings back down the size of its balance sheet, which exploded during the crisis.

Friedman’s idea about the ineffectiveness of fiscal policy is being reinforced by the growing recognition that the discretionary fiscal stimulus packages did little good. Forty years ago, in a famous debate with Keynesian economist Walter Heller, Friedman said “The fascinating thing to me is that the widespread faith in the potency of fiscal policy… rests on no evidence whatsoever. It’s based on pure assumption. It’s based on a priori reasoning.” It was bad news that policy makers in Washington did not heed those words in the past few years as they embarked on massive fiscal stimulus packages. But it’s good news that many more are heeding those words now.

Posted in Teaching Economics

Comments Off on A Milton Friedman Revival

The Taylor Rule Does Not Say Minus Six Percent

The Taylor rule says that the federal funds rate should equal 1.5 times the inflation rate plus .5 times the GDP gap plus 1. Currently the inflation rate is about 1.5 percent and the GDP gap is about -5 percent (using the average of the seven estimates of the gap provided in the recent update by Justin Weidner and John Williams).

So a little algebra gives a funds rate of 1.5X1.5 + .5X(-5) + 1 = .75 percent.

This number is nowhere near -6 percent, which is what you sometimes hear people say the Taylor rule implies. If you think that 1 percent is a better measure of inflation, then that would bring the interest rate down to 0 percent. If you use the largest of the seven gaps reported by Weidner and Williams ( – 8 percent) , then you get an interest rate of -.75 percent. Still nothing close to -6 percent.

How do people get such a large negative percent? As I discussed in this oped a year ago, it is probably because they change the Taylor rule, replacing variables or estimating coefficients with data during which the Fed has set interest rates too low for too long. This can give very misleading results.

Note that the numbers actually implied by the Taylor rule are close to the 0 to .25 percent range currently set by the FOMC. So if inflation begins to pick up or growth gets to be higher than potential GDP growth, then the interest rate should rise. Some , including my colleague Ron McKinnon and also Chuck Schwab, argue that the federal funds rate should be higher, perhaps 1 percent, because they are worried about the functioning of the money market or the low rates on saving. They are much closer to the Taylor rule than those who say -6 percent.

Posted in Monetary Policy

Comments Off on The Taylor Rule Does Not Say Minus Six Percent

New Ideas about Monetary Policy from Jackson Hole

I write from Jackson Hole Wyoming as the early morning sun shines sharply on the Grand Tetons where I just spent a very enjoyable few days at the annual monetary conference. I have been coming to these Jackson Hole conferences on and off since the first one on monetary policy in 1982, and as usual I learned a lot. Here is a brief sampling. I recommend reading the papers and the commentary once they are posted by the Kansas City Fed.

The main thing I took away from Ben Bernanke’s opener (the tradition going back to Paul Volcker and Alan Greenspan is for the Fed chair to lead off) was his call for a “cost-benefit” approach to determine whether another dose of unorthodox large scale asset purchases is needed. This is a big improvement over a “whatever it takes” approach, and it opens the door to a transparent discussion of the costs and benefits of such policies. My own view (based on research with Johannes Stroebel) is that the benefits in terms of lower rates are very small, while the short-term costs of greater uncertainty about the exit strategy and long-term costs from a loss of independence are large.

Larry Christiano presented a new and interesting modification of the Taylor rule which replaces the output gap with a measure of credit growth. He presented some preliminary model simulation work to see how his idea would work in practice. Given the measurement problems with the output gap, more research along these lines would be valuable. Milton Friedman once proposed that I consider replacing the output gap with money growth (M2) in the Taylor rule, which is a similar proposal.

Jim Stock and Mark Watson presented a novel model for inflation forecasting. It focuses entirely on the statistical regularity that inflation declines during recessions. Most important for the current economic situation was their finding that the chances of deflation are quite low right now.

Alan Blinder and I presented our separate critiques of Bank of England Deputy Governor Charlie Bean’s ideas for future monetary policy. Charlie started off by revisiting the critique I presented at the 2007 Jackson Hole conference that policy rates were too low for too long leading up to the crisis; he mentioned recent work by Ben Bernanke, but omitted other papers which I brought to people’s attention. I was surprised that Charlie placed so much emphasis on studies of Fed asset purchases which simply looked at announcement effects, recalling my experience running the international division at Treasury where announcement effects in the currency markets are usually offset soon afterwards. Alan Blinder argued for a more discretionary and interventionist approach, buying more assets including private sector assets. I stressed the benefits of getting back to the rules-based Framework that Works, which is how I labeled the policy that was used effectively for most of the 1980s and 1990s. Here is my commentary. Read Alan’s when it is posted. This debate will continue.

Throughout the conference the growing U.S. government debt problem was the gigantic elephant in the room. Eric Leeper’s dramatic exploding debt charts and his plea for a more scientific approach to fiscal policy analysis made this problem crystal clear for everyone, even though public finance economists in the audience vigorously defended their approach. This debate will also continue.

Posted in Monetary Policy

Comments Off on New Ideas about Monetary Policy from Jackson Hole

The Russian Export Ban: An Economic Story Worth Telling

The Soviet Union used to provide me with plenty of current event stories to tell students in Economics 1 about the wastes and harms of price controls and central planning. But most first-year college students taking introductory economics this fall were born after the collapse of the Soviet Union. Those good old stories are far from students’ personal memory and are certainly not current events.

That’s why I was so interested in Paul Gregory’s recent blog about this summer’s grain export ban in Russia. It’s a current event well worth telling students about. After the damage from the heat to Russia’s grain crop, Prime Minister Putin imposed a ban on grain exports. But as Paul Gregory shows the reason the story is worth telling is that Russia is now an exporter of grain. In contrast the Soviet Union actually had to import grain from the United States and other countries, because of the inefficiency of the collective farms and misallocation of resources under central planning. Recall that President Carter put an embargo on U.S. exports of grain to the Soviet Union, using it as a lever to get the Soviet’s to leave Afghanistan.

In the years before the Russian Revolution, Russia was an exporter of grains. Ukraine was considered the breadbasket of Europe. Now after the collapse of the Soviet Union, Russia and the Ukraine are exporting again. So this fall the inefficiencies of central planning in the Soviet Union can be explained with a current event after all.

Posted in International Economics

Comments Off on The Russian Export Ban: An Economic Story Worth Telling

{kind=link}

{kind=link}