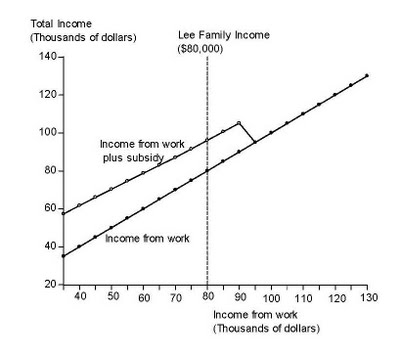

My colleague Dan Kessler writes in today’s Wall Street Journal that Obamacare creates large disincentives to work. I’ve found the following graph useful for showing students why. (The same type of graph is used in of my economics text Chapter 14, p 4o4)  The graph shows income from work and the corresponding health care subsidy for a family of 4 headed by a 55-year old. The subsidy is paid to households earning up to 400 percent of the poverty line. With a poverty line of about $23,300 for a family of 4 in 2014 (when the legislation goes into effect) families earning as much as $93,200 will get a subsidy.

The graph shows income from work and the corresponding health care subsidy for a family of 4 headed by a 55-year old. The subsidy is paid to households earning up to 400 percent of the poverty line. With a poverty line of about $23,300 for a family of 4 in 2014 (when the legislation goes into effect) families earning as much as $93,200 will get a subsidy.

Observe how the subsidy declines with income and then is slashed to zero when 400 percent of the poverty line is hit. You can even see the V-shaped “notch” in the graph, which has become the technical term used to describe such sudden drops in subsidies. Consider the Lee family, for example. They earn $80,000 and thus get a subsidy of $16,100, bringing their total income to $96,100. But suppose they decide to work more. If they increase their income from work by $14,000, bringing their work earnings to $94,000, then their health care subsidy drops to zero. So they get less income by working more, and that’s a big disincentive.

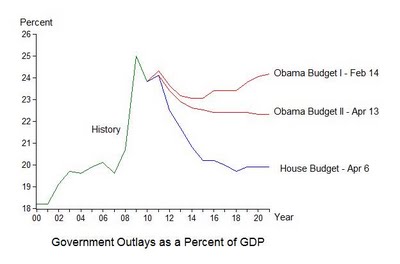

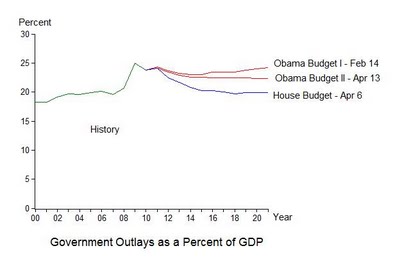

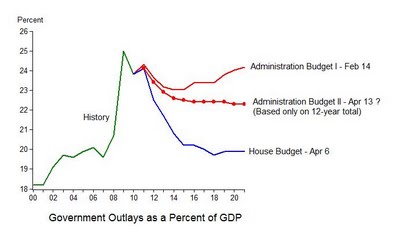

The graph focuses on the next 10 years because that is the frame of reference for Budget I, the House Budget, and the current budget process. It is important to note, however, that my calculations imply that $1 trillion of the $3 trillion outlay reductions in Budget II compared with Budget I occur in the two years after the 10 year window. So in reality the proposed reduction in spending growth is $2 trillion rather than $3 trillion.

The graph focuses on the next 10 years because that is the frame of reference for Budget I, the House Budget, and the current budget process. It is important to note, however, that my calculations imply that $1 trillion of the $3 trillion outlay reductions in Budget II compared with Budget I occur in the two years after the 10 year window. So in reality the proposed reduction in spending growth is $2 trillion rather than $3 trillion.