In a new paper I examine the ways for the Fed to engage in a reentry to a rules-based monetary policy. For several years, starting around 2017, the Fed had begun to move to a rules-based monetary policy that had worked well in the US in the 1980s, 1990s, and in other years. Many papers were written at the Fed about the benefits, and the Fed began to report on rules-based policy in its Monetary Policy Report.

That move was interrupted in the first quarter of 2020 when COVID-19 hit. The Fed took a number of actions to deal with the effects and by most accounts these actions were special and were not consistent with rules-based policies. The Fed also stopped reporting on rules-based policy in its Monetary Policy Report.

Later in 2020 the Fed completed a review of its monetary policy and reported on possible changes in policy. By early 2021 the Fed began to put rules back in its Monetary Policy Report and the new rules reflected some of these changes. But these changes have not yet affected actual monetary policy decisions and there is evidence of big difference between the rules-based policy and the actions of the Fed.

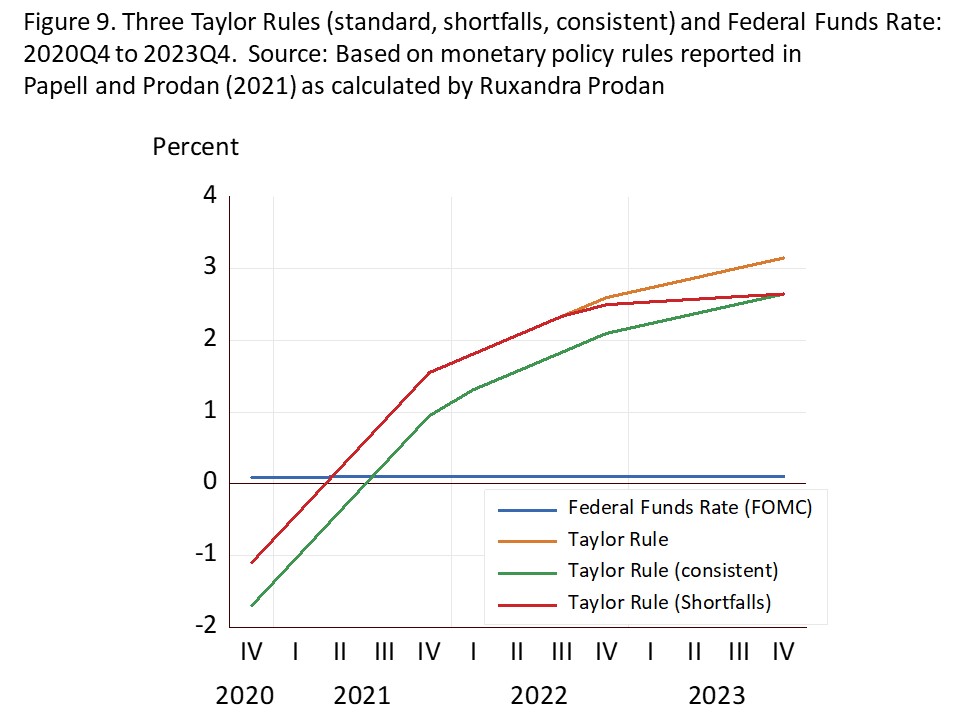

To develop an optimal reentry, I consider a recent paper by David Papell and Ruxandra Prodan. For the Taylor (shortfalls) rule & the balanced approach (shortfalls) rule, they replaced the difference between the unemployment rate in the long run and actual unemployment rate with minimum of the difference and 0. If the unemployment rate is 3.5 percent and long run level is 4.0 percent, the interest rate is not raised. That is, zero is the minimum of .5 percent (=4.0-3.5) and zero.

They also considered another adjustment which results in a Taylor (consistent) rule and a balanced approach (consistent) rule. They assume that the Fed would not adjust the interest rate if inflation is 2.0 or 2.1 percent; rather it would watch for inflation going above 2.2 percent. Also assumed is that the equilibrium real interest rate is .5 percent.

I looked at the period from the 4th quarter of 2020 through the 4th quarter of 2023. Figure 9 from the paper copied below shows a big difference between the rules-based policy and the actions of the Fed.

It is time for reentry.