The Fed’s Monetary Policy Report released last Friday devotes a lot of space to monetary policy rules. This is the third time in a row that the monetary policy report has included such discussions, the first being in July 2017 and the second in February 2018. Compared with the previous two monetary policy reports, this Report adds new material on policy rules, and is joined with a helpful discussion of policy rules now integrated into the Monetary Policy Principles and Practice section of the Fed’s web page.

All this represents progress in my view. It would be good if the new material generates some questions and answers in the Senate and House hearings with Fed Chair Jay Powell this week. Having such a discussion is one of the purposes of the bills in Congress under which the Fed would report on policy rules and strategies.

As with Fed minutes, there is something to be gained from examining the similarities and differences compared the most recent and previous reports, though the process of reporting is probably still evolving and a purpose of policy rules is that they entail less not more fine-tuning.

The new report presents (p. 37) the same key principles of policy embedded in the Taylor rule and other policy rules as discussed in previous reports: “Policy rules can incorporate key principles of good monetary policy. One key principle is that monetary policy should respond in a predictable way to changes in economic conditions. A second key principle is that monetary policy should be accommodative when inflation is below the desired level and employment is below its maximum sustainable level; conversely, monetary policy should be restrictive when the opposite holds. A third key principle is that, to stabilize inflation, the policy rate should be adjusted by more than one-for-one in response to persistent increases or decreases in inflation.” The section “Principles for the Conduct of Monetary Policy” on the Fed’s web site discusses in more detail how these principles relate to policy rules and explains the rationale for the third principle, sometimes called the Taylor principle.

Another similarity is that that the new report focuses on the same five rules as in February: the “well-known Taylor (1993) rule” and “Other rules” which “include the ‘balanced approach’ rule [Taylor rule with a higher coefficient on the output variable], the ‘adjusted Taylor (1993)’ rule, the ‘price level’ rule, and the ‘first difference’rule.”

The paragraph with the title Monetary policy rules (p. 3) is identical to the previous reports. Among other things, it states that monetary policymakers “routinely consult monetary policy rules.” But later paragraphs differ (italics added to show this):

Feb 2018: “However, the use and interpretation of such prescriptions require careful judgments about the choice and measurement of the inputs to these rules as well as the implications of the many considerations these rules do not take into account. (pp. 31-32)

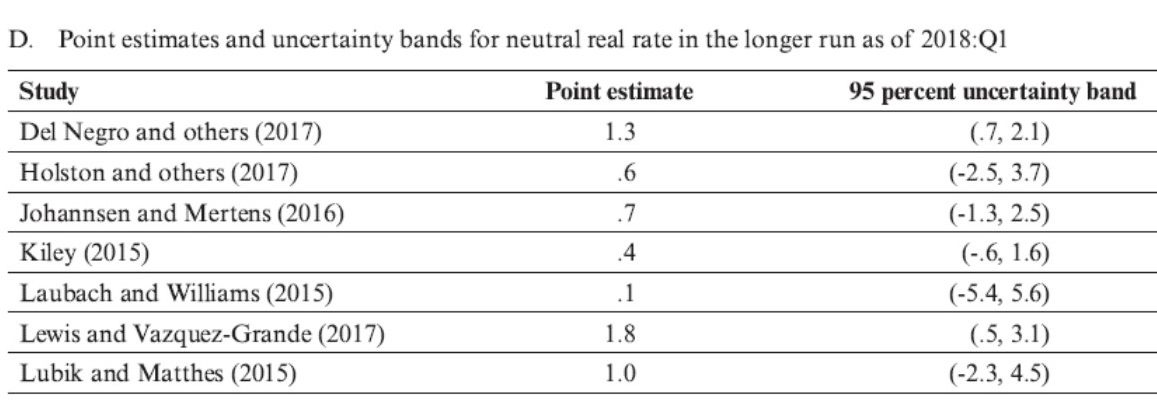

July 2018” “However, the use and interpretation of such prescriptions require, among other considerations, careful judgments about the choice and measurement of the inputs to these rules such as estimates of the neutral interest rate, which are highly uncertain (p 36)

That is, the latest report focuses on uncertainty about the “neutral” or “equilibrium real” interest rate while the earlier reports also focused on uncertainty about the neutral unemployment rate and the measures of inflation. Indeed, the latest report has a new table (p. 41) shown below, and long discussion reporting on recent research on the neutral rate. Note that the point estimates range from 0.1 percent to 1.8 percent.

I think it is significant that the discussion of the neutral rate is placed within the discussion of policy rules in the report. Like many aspects of uncertainty, this particular uncertainty has profound effects on policy making whether policy is rules-based or not. However, the discussion of the policy implications of this uncertainty is much clearer and more informative when it falls, as in this report, within a framework of policy rules.

That there is a wide range of uncertainty is illustrated in this time-series diagram drawn from the report. Note that the the estimated neutral rate was much higher in the years from 2002 to 2007 before the Great Recession indicating that, according to these estimates, the “two-low-for-too long” period cannot be rationalized as due to a decline in the neutral rate.

That there is a wide range of uncertainty is illustrated in this time-series diagram drawn from the report. Note that the the estimated neutral rate was much higher in the years from 2002 to 2007 before the Great Recession indicating that, according to these estimates, the “two-low-for-too long” period cannot be rationalized as due to a decline in the neutral rate.

There is more on policy rules in the report and also, as mentioned above, on the the web page. I would note in particular the section Policy Rules and How Policymakers Use Them which discusses alternative policy rules, the section on Challenges Associated with Using Rules to Make Monetary Policy which delves into issues that the Fed faces when it implements rules, and the section Monetary Policy Strategies of Major Central Banks which contains a good discussion of what is happening abroad with the conclusion that “other major central banks use policy rules in a similar fashion.” This section is very important when one considers monetary policy normalization and monetary reform on a global scale, which is entirely appropriate in today’s integrated world economy