This week marks the 20-year anniversary of a “notable conference” on monetary policy as Ed Nelson, who reminded me, puts it. The conference took place at the Cheeca Lodge in the Florida Keys on January 15-17, 1998, and it resulted in the book Monetary Policy Rules published by the University of Chicago Press for the NBER.

This week marks the 20-year anniversary of a “notable conference” on monetary policy as Ed Nelson, who reminded me, puts it. The conference took place at the Cheeca Lodge in the Florida Keys on January 15-17, 1998, and it resulted in the book Monetary Policy Rules published by the University of Chicago Press for the NBER.

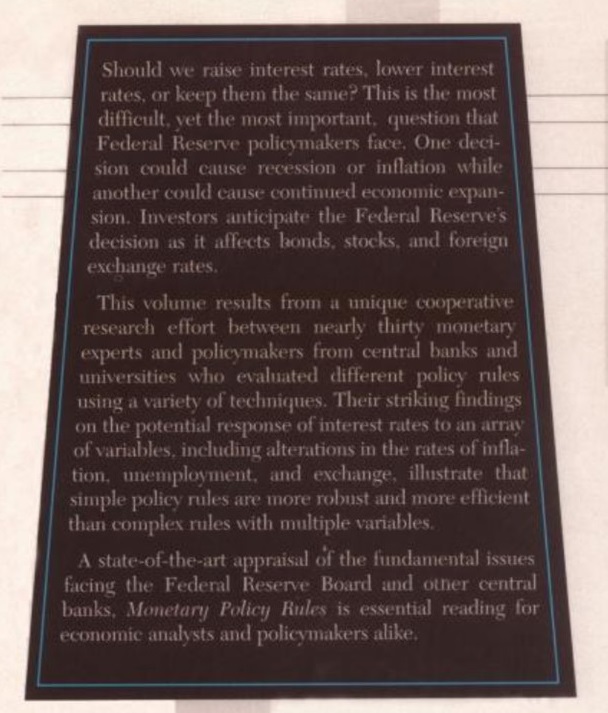

It was an unusual conference. As stated on the back of the book jacket shown below, it was a “unique cooperative research effort between nearly thirty monetary experts and policymakers.” The purpose was to evaluate alternative monetary policies, all of which were described by policy rules for the interest rate. It was unique because the participants in the conference not only evaluated the performance of their own proposed policy rules with their own models, they also evaluated the performance of other participants’ proposed rules with their models. This put the focus on robustness and effectiveness in a way that had not been done before.

As I summarized in the Introduction “we asked researchers who participated in the conference to investigate the other researchers’ proposals for policy rules using their own models. We did not specify what model (whether large or small, rational or nonrational) should be used. That decision was left up to the researchers.” It turned out that nine models participated in the evaluation exercise, each of which was described in the individual research papers given at the conference: Performance of Operational Policy Rules in an Estimated Semiclassical Structural Model by Bennett McCallum and Edward Nelson; Interest Rate Rules in an Estimated Sticky Price Model by Julio Rotemberg and Michael Woodford; Policy Rules for Open Economies by Laurence Ball; Forward-Looking Rules for Monetary Policy by Nicoletta Batini and Andrew Haldane; Policy Rules for Inflation Targeting by Glenn Rudebusch and Lars Svensson; and four models in the Robustness of Simple Monetary Policy Rules under Model Uncertainty by Andrew Levin, Volker Wieland, and John Williams

As I summarized in the Introduction “we asked researchers who participated in the conference to investigate the other researchers’ proposals for policy rules using their own models. We did not specify what model (whether large or small, rational or nonrational) should be used. That decision was left up to the researchers.” It turned out that nine models participated in the evaluation exercise, each of which was described in the individual research papers given at the conference: Performance of Operational Policy Rules in an Estimated Semiclassical Structural Model by Bennett McCallum and Edward Nelson; Interest Rate Rules in an Estimated Sticky Price Model by Julio Rotemberg and Michael Woodford; Policy Rules for Open Economies by Laurence Ball; Forward-Looking Rules for Monetary Policy by Nicoletta Batini and Andrew Haldane; Policy Rules for Inflation Targeting by Glenn Rudebusch and Lars Svensson; and four models in the Robustness of Simple Monetary Policy Rules under Model Uncertainty by Andrew Levin, Volker Wieland, and John Williams

The main finding of this effort surprised people at the time. It was that “simple policy rules are more robust and more efficient than complex rules with multiple variables,” a finding that has stood the test of time and many more studies of over the past two decades.

It was a tough to establish uniformity in the evaluation method so that each rule was treated fairly. Thanks to the model data base of Volker Wieland and improvements in computer and information technology, it is much easier to do conduct this kind of robustness study now.

Monika Piazzesi, a Stanford graduate student at the time, prepared a very useful summary of the discussion that took place at the conference. Soon afterwards the Fed began referring to the Taylor (1999) rule which had a higher coefficient on output than the so-called Taylor rule. (1999 was the year the book was published.). I complained because I had not proposed such a rule in the chapter in the book but simply compared it with other rules. Because of my complaint, Janet Yellen started calling that rule the balanced rule from then on, not that the name made much difference.