This week I gave the Swiss National Bank’s Annual Karl Brunner Lecture in Zurich, and I thank Thomas Jordan who introduced me and the hundreds of central bankers, bankers, and academics who filled the big auditorium. Karl was a brilliant, innovative economist who thought seriously about both policy ideas and institutions. For the lecture, I focused on ideas and institutions for international monetary policy.

Since Karl died in 1989, we can only wonder what he would think about monetary policy in the past dozen years. But we can get some hints from his former student, collaborator, friend, and great economist Allan Meltzer, who died earlier this year.

About one year ago at the annual monetary conference in Jackson Hole, Meltzer argued that the Fed’s “quantitative easing” was in effect a monetary policy of “competitive devaluation,” and he added that “other countries have now followed and been even less circumspect about the fact that they were engaging in competitive devaluation. Competitive devaluation was tried in the 1930s, and unsuccessfully, and the result was that around that time major countries agreed they would not engage in competitive devaluation ever again.”

In the lecture, I examined this idea empirically, and I found striking results. A monograph with the details will soon be published by the MIT Press, but a very short taste of the results can be given here.

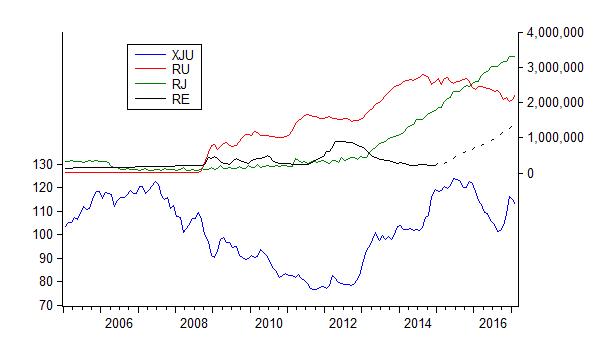

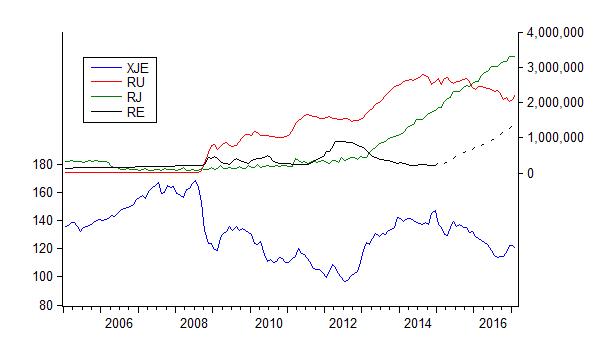

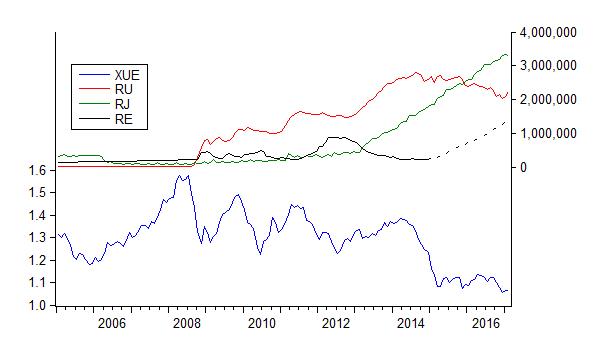

I began by introducing a simple modelling framework which captures key features of recent economic policy. I focused on the balance sheet operations of the Federal Reserve, the European Central Bank, and the Bank of Japan. I concentrated on the liability side and, in particular, on reserve balances which are used to finance asset purchases, as a measure of the balance sheet operations. For the three central banks this gives RU which measures the Fed’s reserve balances in millions of dollars, RJ which measures the BOJ’s current account balances in 100s of million yen, and RE which measures the ECB’s current account plus deposit facility in millions of euros. I also considered the central bank in a relatively small open economy—the Swiss National Bank.

To examine the impact of the balance sheet operations of the central banks in the three large areas I estimated the following equations.

XJU = α0 + α1RJ + α2RU + α3RE

XJE = β0 + β1RJ + β2RU + β3RE

XUE = γ0 + γ1RJ + γ2RU + γ3RE

where XJU is the yen per dollar exchange rate; XJE is the yen per euro exchange rate; and XUE is the dollar per euro exchange rate.

All the estimated coefficients are significant, and they showed that:

- An increase in reserve balances RJ at the Bank of Japan causes XJU and XJE to rise, or, in other words, causes the yen to depreciate against the dollar and the euro.

- An increase in reserve balances RU at the Fed causes XJU to fall and XUE to rise, or, in other words, causes the dollar to depreciate against the yen and the euro.

- An increase in reserve balances RE at the ECB causes XJE and XUE to fall, or, in other words, causes the euro to depreciate against the yen and the dollar.

The charts below show the patterns of reserve balances and the corresponding exchange rate movements: first there is the increase in reserve balances at the Fed with a depreciation of the dollar; second there is an increase in reserve balances at the BOJ with a depreciation of the yen; and third there is increase in reserve balances at the ECB and a depreciation of the euro.

In other words, there are significant exchange rate effects of balance sheet operations for the large advanced countries. In the lecture I then went on to show that there are similar effects for the Swiss National Bank, as in other central banks in small open economies that have little choice but to react to prevent these unwanted moves in their own exchange rates.

These exchange rate effects are likely to be a factor behind balance sheet actions taken by central banks and the reason for the policy contagion in recent years as countries endeavor to counteract other countries’ actions to influence exchange rates. In this sense, there is a “competitive devaluation” aspect to these actions as argued by Allan Meltzer—whether they are intentional or not.

The resulting movements in exchange rates can be a source of instability in the global economy as they affect the flow of goods and capital and interfere with their efficient allocation. They also are a source of political instability as concerns about currency manipulation are heard from many sides. They are another reason to normalize and reform the international monetary system. In my view a rules-based international system is the way to go, as I discussed in the lecture at the Swiss National Bank referring to earlier work here.