In his Saturday Wall Street Journal essay “Why the Economy Doesn’t Roar Anymore”—illustrated with a big lion with its mouth shut—Marc Levinson offers the answer that the “U.S. economy isn’t behaving badly. It is just being ordinary.” But there is nothing ordinary (or secular) about the current stagnation of barely 2 percent growth. The economy is not roaring because it’s muzzled by government policy, and if we take off that muzzle—like Lucy and Susan did in “The Lion, the Witch and the Wardrobe”—the economy will indeed roar.

In his Saturday Wall Street Journal essay “Why the Economy Doesn’t Roar Anymore”—illustrated with a big lion with its mouth shut—Marc Levinson offers the answer that the “U.S. economy isn’t behaving badly. It is just being ordinary.” But there is nothing ordinary (or secular) about the current stagnation of barely 2 percent growth. The economy is not roaring because it’s muzzled by government policy, and if we take off that muzzle—like Lucy and Susan did in “The Lion, the Witch and the Wardrobe”—the economy will indeed roar.

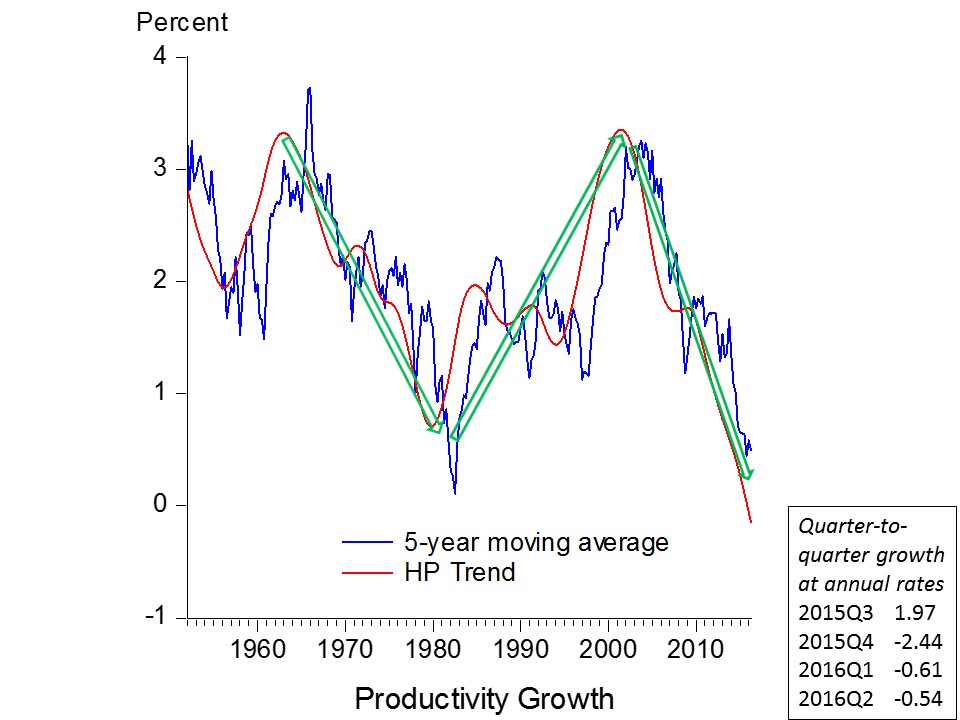

It is of course true, as Levinson states, that “faster productivity growth” is “the key to faster economic growth.” But it’s false, as he also states, that it has all been downhill since the “long boom after World War II” and “there is no going back.” The following chart of productivity growth drawn from my article in the American Economic Review shows why Levinson misinterprets recent history. Whether you look at 5 year averages, statistically filtered trends, or simple directional arrows, you can see huge swings in productivity growth in recent years. These movements—the productivity slump of the 1970s, the rebound of the 1980s and 1990s, and the recent slump—are closely related to shifts in economic policy, and economic theory indicates that the relationship is causal, as I explain here and here and in blogs and opeds. You can also see that the recent terrible performance—negative productivity growth for the past year—is anything but ordinary.

Writing about the 1980’s and 1990s, Levinson claims that “deregulation, privatization, lower tax rates, balanced budgets and rigid rules for monetary policy—proved no more successful at boosting productivity than the statist policies…” The chart shows the contrary: productivity growth was generally picking up in the 1980s and 1990s. It is the stagnation of the late 1960s, the 1970s, and the last decade that is state-sponsored. To turn the economy around we need to take the muzzle off, and that means regulatory reform, tax reform, budget reform, and monetary reform.