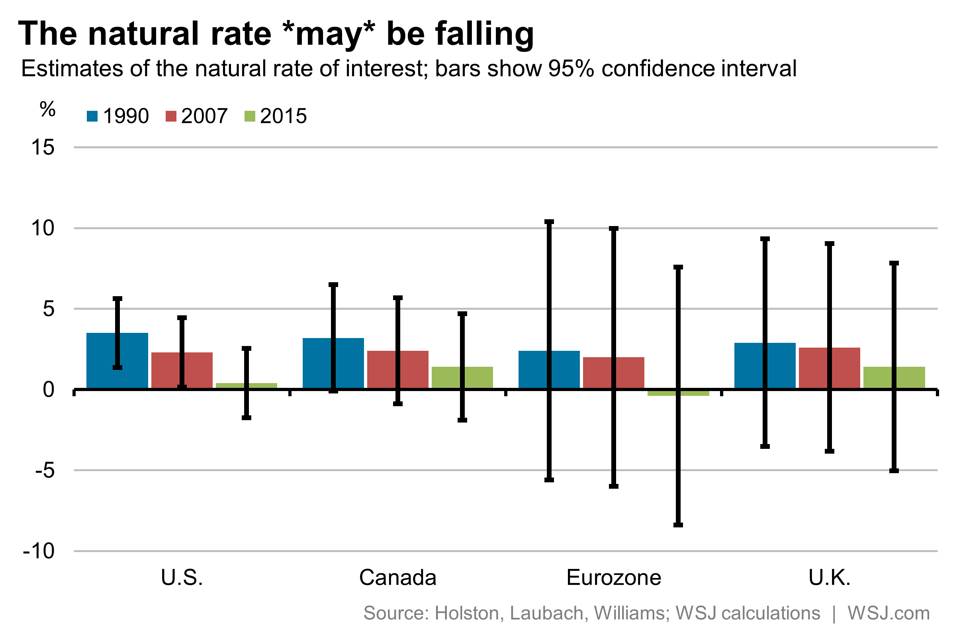

In a recent Wall Street Journal piece, “Think You Know the Natural Rate of Interest? Think Again,” James Mackintosh warns about the high level of uncertainty in recent estimates of the equilibrium interest rate—commonly called r* or the natural rate—that are being factored into monetary policy decisions by the Fed. See discussion by Fed Chair Janet Yellen for example. Mackintosh’s argument is simple. He takes the confidence intervals (uncertainty ranges) from the recent study by Kathryn Holston, Thomas Laubach, and John Williams, which, as in an earlier paper by Laubach and Williams, finds that the estimate of the equilibrium rate has declined. Here is a chart from his article showing the wide range of uncertainty.

Mackintosh observes that the confidence intervals are very wide, “big enough to drive a truckload of economists through,” and then concludes that they are so large that “it’s entirely plausible that the natural rate of interest hasn’t moved at all.”

This uncertainty should give policy makers pause before they jump on the low r* bandwagon, but there is even more reason to think again: the uncertainty of the r* estimates is actually larger than reported in the Mackintosh article because it does not incorporate uncertainty about the models used.

In a recent paper Volker Wieland and I show that the models used by Holsten, Laubach and Williams and others showing a declining r* omit important variables and equations relating to structural policy and monetary policy. We show that there is a perfectly reasonable alternative explanation of the facts if one expands the model to include these omitted factors. Rather than conclude that the real equilibrium interest rate r* has declined, there is an alternative model in which economic policy has shifted, either in the form of reversible regulatory and tax policy or in the form if monetary policy. Moreover we show that there is empirical evidence in favor of this explanation.

Another recent paper “Reflections on the Natural Rate of Interest, Its Measurement, Monetary Policy and the Zero Bound,” (CEPR Discussion Paper) by Alex Cukierman reaches similar conclusions. He identifies specific items that could have shifted the relationship between the interest rate and macro variables including credit problems that affect investment. He also looks at specific factors that shifted the policy rule such as central bank concerns with financial stability. His paper is complementary to ours, and he also usefully distinguishes between risky and risk-free rates, a difference ignored in most calculations.

Overall the Wieland, Taylor and Cukierman papers show that estimates of r* are way too uncertain to incorporate into policy rules in the ways that have been suggested. Nevertheless, it is promising that Chair Yellen and her colleagues are approaching the r* issue through the framework of monetary policy rules. Uncertainty in the equilibrium real rate is not a reason to abandon rules in favor of discretion.