In my article on British monetary policy in yesterday’s Financial Times, I suggested (recommendation 5) that as the Bank of England seeks a way to implement forward guidance it might want to consider a “rule for all seasons” as a guideline. This rule would allow for the possibility that bank rate would be extra low in periods following a stint at the zero lower bound, but by a measurable rules-based amount that depends in a consistent way on the degree to which the desired bank rate has fallen below zero bound.

The idea comes from a very early paper (perhaps the first) on using forward guidance to deal with the zero bound. It was presented at a conference in Woodstock, Vermont more than a decade ago and published by David Reifschneider and John Williams (now president of the San Francisco Fed). I used the term “rule for all seasons” in the FT to convey the idea that it is a kind of meta-rule which would apply consistently whether or not the zero bound was constraining. In principle, it thereby mitigates the time inconsistency problems that the Fed’s current forward guidance has created.

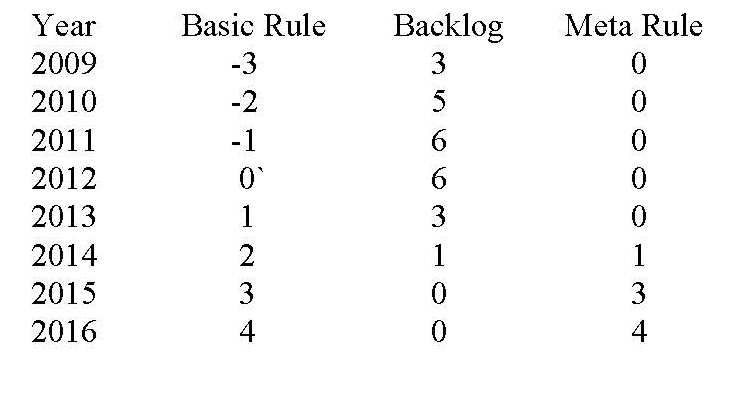

As Reifschneider and Williams explained: “What we seek is a policy that deviates from the Taylor rule in a negative direction at times when interest rates are unconstrained and there is a ‘backlog’ of past deviations—i. e. immediately following episodes of zero interest rates….”

The specific policy they propose can be written down algebraically (see equation 4 in their paper), so technically speaking it is a rule. It would require keeping track of the backlog by summing up all the past deviations, as explained in the following example. Suppose that the zero bound was not constraining, according to the basic Taylor rule, in the years up to 2008. Suppose also that in the years from 2009 to 2016 the basic rule algebraically called for the interest rate shown in the first column of the table, labeled “basic rule”. The resulting 4-year backlog and the interest rate implied by the meta-rule, which is the maximum of (1) zero and (2) the basic rate minus the backlog, are shown in second and third columns:

Notice that even though the basic rule calls for 1% in 2013, the actual rate would still be zero due to the backlog correction in the meta-rule. The actual rate is lower than the basic rule in 2014 and by 2015 the meta-rule is back to the basic rule.

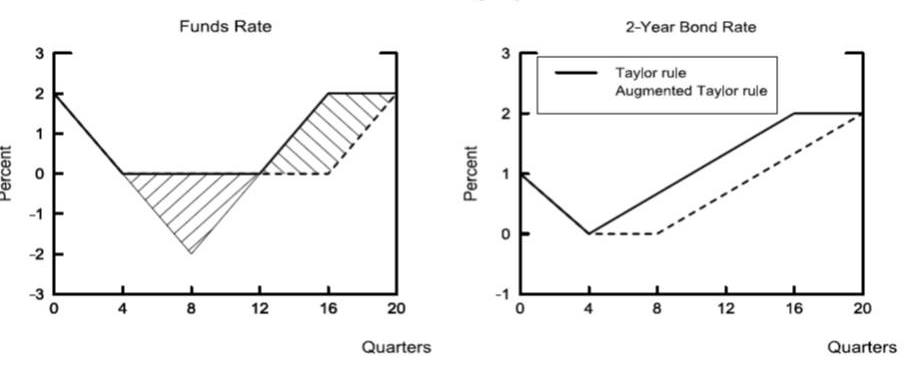

The following chart copied from the Reifschneider-Williams paper illustrates how such a path for the short rate could affect a longer rate using an expectations theory of the term structure.