Paul Krugman disagrees with my recent post that the recovery is weak compared to recoveries from past serious U.S. recessions including those associated with financial crises. I’ve been writing about the reasons for weak recovery for two years, but the issue has heated up because of its relevance to the elections this fall.

In making his critique, Krugman appeals to a recent oped in Bloomberg View by Carmen Reinhart and Ken Rogoff who criticize the research of economic historian Michael Bordo and his coauthor Joseph Haubrich of the Cleveland Fed, which I have referred to. Bordo and Haubrich demonstrate that the recovery from the recent recession and financial crisis has been unusually weak compared to recoveries from past recessions with financial crises in the United States. In separate research, Jerry Dwyer and Jim Lothian report the same finding. Neither Reinhart-Rogoff nor Krugman disprove this finding.

To see this, consider the points made by Reinhart and Rogoff, and also by Krugman.

First, they argue for a narrower definition of a financial crisis. Reinhart and Rogoff say that one should “distinguish systemic financial crises from more minor ones and from regular business cycles.” Thus they exclude some cases studied by Bordo and Haubrich. But narrowing the focus to systemic crises in this way does not change the Bordo-Haubrich findings because the recovery from the recent recession is weaker than the average of past recessions cum financial crises even with these exclusions.

Second, Reinhart and Rogoff argue that one should look at recessions together with recoveries when looking at severity. In fact, in their work they explicitly “don’t delineate between the ‘recession’ period and the ‘recovery’ period.” But there is no disagreement that recessions associated with financial crises have tended to be deeper than those without financial crises. I certainly don’t deny that there was a serious financial crisis. In fact I wrote one of the first books on the crisis and found that government policy prior to 2009 was to blame, just as government policy was to blame for the even more serious Great Depression.

The issue that I and others have focused on is whether the recovery is unusually weak. By mixing recessions with recoveries Reinhart and Rogoff blur the classic distinction, which has long been at the heart of macroeconomic analysis. Because they do not examine recoveries per se, their empirical analysis does not disprove the fact that the current recovery is very weak as Bordo and Haubrich and others have shown.

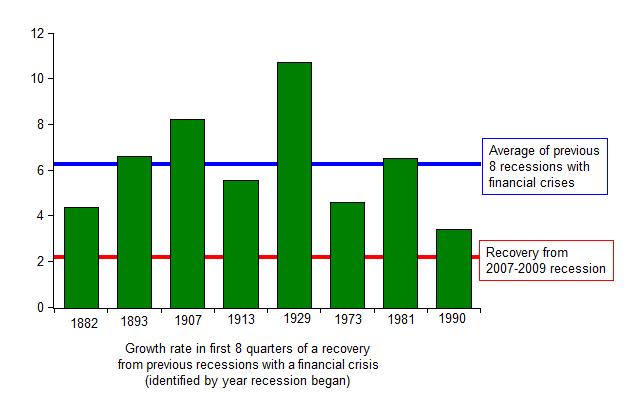

Third, there is the complaint that in a simple chart I used to show how weak the recovery has been, I only looked at the first four quarters of recovery. But I also mentioned that Bordo and Haubrich use a different measure, which goes well beyond 4 quarters, and come to the same conclusion, and also that the current recovery has weakened further since the first four quarters. In any case, the focus on four quarters has nothing to do with it. Here is a chart that looks at growth during the first eight quarters. The story is the same.

Since most of the Reinhart, Rogoff and Krugman criticism is implicitly aimed at the historical work of Bordo and Haubrich, it is appropriate to conclude with what Bordo wrote in response to a press inquiry which he shared with me. Bordo puts it this way:

Aside from the unnecessary political rhetoric and ad hominems, the basic difference between my research with Joseph Haubrich on U.S. recoveries and that of Carmen Reinhart and Ken Rogoff is over the methodology of defining a recovery. Reinhart and Rogoff focus on the behavior of the level of real per capita GDP from the peak preceding the financial crisis to the point in the succeeding recovery at which the earlier peak level of real per capita GDP is reached. We look at what is called the bounce back, the pace of recovery from the trough of the business cycle.

We find that deep recessions accompanied by financial crises bounce back faster than recessions which do not have financial crises. These results are even stronger when we focus on what Reinhart and Rogoff call systemic crises, like 1893 and 1907. The recent recession and financial crisis is a major exception to this pattern. The recovery remains tepid after three years.

Reinhart and Rogoff s methodology combines the downturn with the recovery. Using our data but following their approach one would get the same results as they do, that recessions with financial crises have slow recoveries as I show in my Wall Street Journal op ed. Their use of real per capita GDP rather than just real GDP would not make any difference to our results. Thus comparing their methodology with ours is like comparing apples with oranges. Our approach focuses directly on the question– are recoveries after recessions with financial crises associated with slower or faster than average recoveries. Their approach answers a different question than we ask.

In sum, the weak recovery deniers have not made their case.