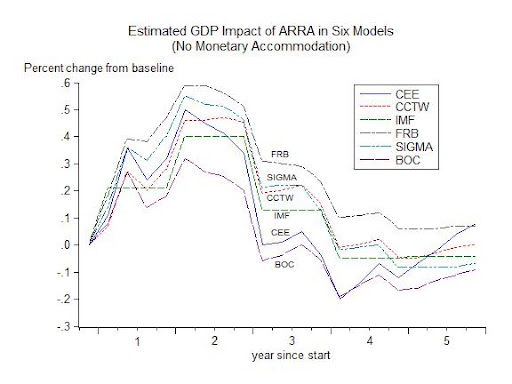

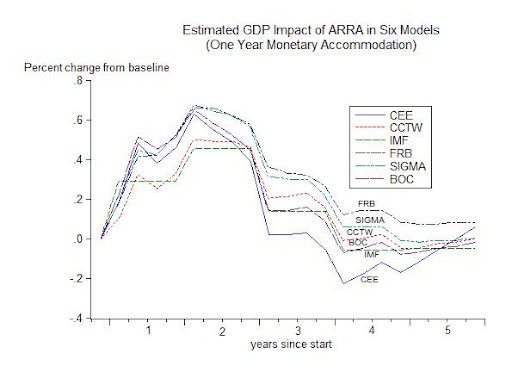

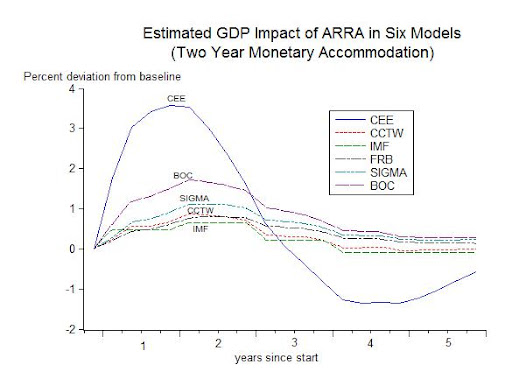

The new paper, Effects of Fiscal Stimulus in Structural Models, is written by 17 authors from central banks and international institutions around the world (Guenter Coenen, Chris Erceg, Charles Freedman, Davide Furceri, Michael Kumhof, René Lalonde, Douglas Laxton, Jesper Lindé, Annabelle Mourougane, Dirk Muir, Susanna Mursula, Carlos de Resende, John Roberts, Werner Roeger, Stephen Snudden, Mathias Trabandt, and Jan in’t Veld). As part of the research reported in the paper the authors compare the CCTW and the CEE estimates of ARRA with four estimated “New Keynesian” structural models of the kind used in practice by policymakers and their staffs. The other four models are:

Bank of Canada’s GEM model (BOC)

Fed’s FRBUS model (FRB)

Fed’s SIGMA model (SIGMA)

International Monetary Fund’s GIMF model (IMF)

Coenen and his colleagues simulated all 6 models in order to contrast and compare the impact of ARRA (using same time profile of government purchases first used by CCTW). The results for GDP are shown in the following three graphs (which correspond to Figure 7 of Coenen et. al. and refer to the US with three different levels of monetary accommodation). Observe that the four policy models confirm or validate the original CCTW estimates in the sense that they cluster around CCTW. In the case of the two year monetary accommodation the CEE model is a large outlier.