- Last Friday in New York, Charles Plosser, President of the Philadelphia Fed, proposed an exit strategy for the Fed. It’s the first explicit exit strategy to be put forth by a member of the FOMC, so it deserves careful consideration and discussion.

- Previous statements about exits by Fed officials simply listed the tools that could be used in an exit strategy, but did not actually put forth an exit strategy. In contrast, President Plosser describes a specific strategy.

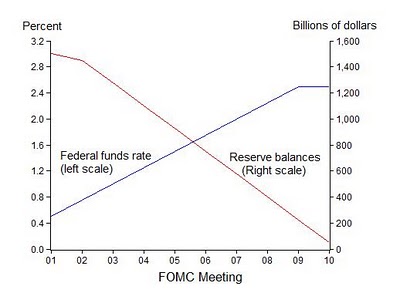

- Two things are very attractive about the strategy. First, it aims to return monetary policy to one in which the federal funds rate is determined by the supply and demand for reserves. This of course requires that the Fed bring down the enormous supply of reserve balances on its balance sheet to a level closer to a quantity demanded by banks at a positive interest rate. Reserves were $26 billion on September 10, 2008 when the funds rate was 2 percent just before the panic, which gives an order of magnitude of where reserves should go. Plosser assumes $50 billion, which seems reasonable to me. But reserve balances will be around $1,500 billion by the time QEII is over, so it’s a long way down.

- The second attractive feature of the exit strategy is that the path of reduction in reserve balances is tied to future movements of the federal funds rate. It is thus much like an exit rule, or a contingency plan, which both preserves flexibility and creates predictability. The exit rule would reduce reserves by $125 billion for each 25 basis point increase in the funds rate plus another $50 billion at each FOMC meeting. After 10 meetings $1,450 billion would be removed (the contingency plan starts at the second meeting) bringing reserves to $50 billion.

- This chart, drawn from data in his speech, shows how the strategy would work if the Fed increased the federal funds rate by 25 basis points for ten consecutive meetings. Of course an advantage of this strategy is that the pace of reserve drawdown is tied to the funds rate—if the funds rate rises more quickly reserves will come down more quickly.

- The strategy is very close to one I recommended a year ago in testimony, “An Exit Rule for Monetary Policy,” prepared for a Congressional hearing at the House Financial Services Committee. I suggested $100 billion per 25 basis points with no constant amount, but that was before QEII when reserve balances were much lower. I argued that such a strategy would reduce risks in the markets. With increased predictability about policy, banks could better manage their own balance sheets and the price discovery process would be much smoother as funds traders and other market participants could better anticipate what the Fed would do, a view which was supported by Peter Fisher (head of the New York Fed trading desk in the 1990s), who I consulted about the idea at the time.

- Of course the New York Fed trading desk should have some discretion about how to execute the FOMC’s directive if such a strategy is adopted. I hope it is.

A Good Exit Strategy Proposed by Philadelphia Fed President Plosser

This entry was posted in Monetary Policy. Bookmark the permalink.