New empirical research establishes a strong relationship between very low interest rates set by the Fed, as in the period 2002-2005, and a risk-taking search for yield. This policy-induced lessening of risk aversion has been emphasized by Raghu Rajan and others as a key factor bringing on the financial crisis. The new empirical support for this view is reported in the working paper “Risk, Uncertainty and Monetary Policy” by Geert Bekaert, Marie Hoerova, and Marco Lo Duca.

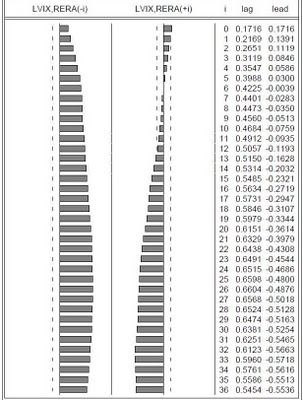

The basic evidence is the pattern of correlations over time which can found by looking carefully through the following bar graphs and table drawn from the paper.

The bar graph on the right (and the second column of numbers) shows the correlation coefficients between the VIX and values of the federal funds rate at varying months going into the future. After the first few months, these correlations are negative and significant indicating that the Fed tends to react to high levels of volatility by lowering interest rates.

The bottom line of this empirical research, as the authors put it, is that “lax monetary policy increases risk appetite (decreases risk aversion) in the future, with the effect lasting for about two years and starting to be significant after five months.” Their result is important to the policy debate because such monetary policy has been “cited as one of the contributing factors to the build up of a speculative bubble prior to the 2007-09 financial crisis.”