What are the implications of all the recent economic reports (January employment, 4th quarter GDP, CBO’s downward revision of potential GDP) for an assessment of the recovery from the 2007-09 recession? In my view, they still indicate a very weak recovery. As I have argued, a good standard of comparison for this recovery is the most recent recovery from a very deep recession, namely the one that ended in 1982, and I have offered a series of charts to make the comparison easy and objective. Here are updates of those charts based on the latest data.

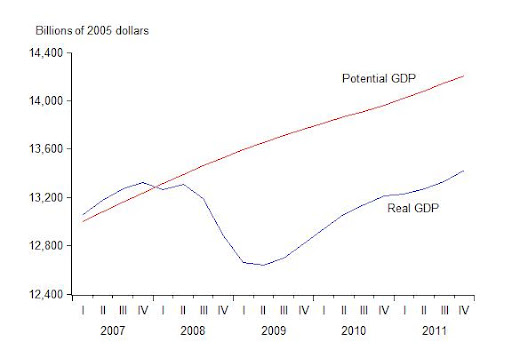

The first chart shows real GDP during the 10 quarters since the end of the 2007-2009 recession along with CBOs recently revised estimate of potential GDP. The chart clearly shows that the economy has yet to recover back to its potential. The only real difference from earlier assessments is that CBO has slightly lowered its estimate of potential.

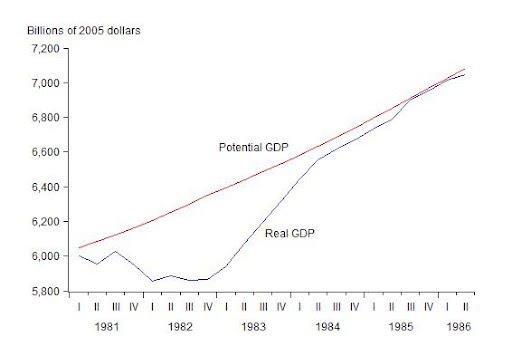

For comparison, the next chart shows the recovery back to potential in the 10 quarters following the 1981-82 recession. The difference between the two charts is striking, and is why one can say that the current recovery is a recovery in name only.

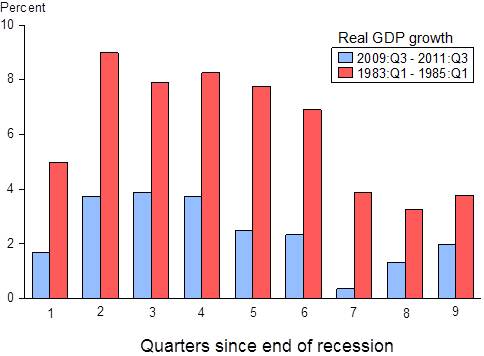

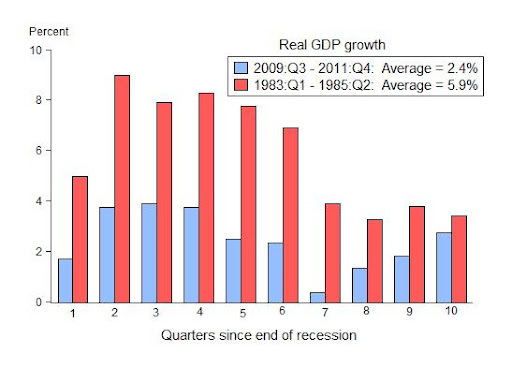

It is also helpful to compare economic growth rates during the two recoveries as shown in the next chart. Growth averaged 2.4 percent in the recent 10 quarters compared with 5.9 percent in the 1980s recovery.

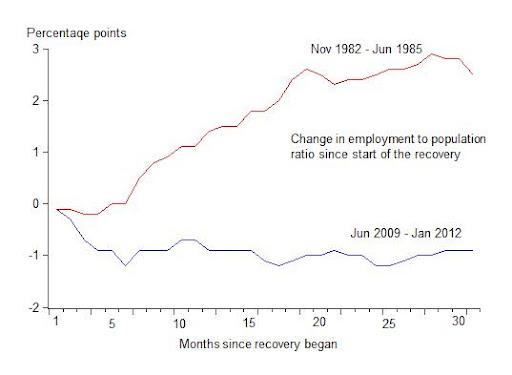

Finally, compare the employment-to-population ratio in the two recoveries as in the next chart. It shows that even with the better news on employment and the unemployment rate, the percentage of the working age population that is actually working is not rising.