Hundreds of financial market participants and news reporters showed up for the 18th annual “ECB and its Watchers” conference in Frankfurt last week. I was one of the speakers as I was at the first conference in 1999. It was a good day for talking about policy with candid questions and answers. ECB President Mario Draghi led off with a review of current policy; I followed with a talk about asset purchase programs (my assigned topic),

Hundreds of financial market participants and news reporters showed up for the 18th annual “ECB and its Watchers” conference in Frankfurt last week. I was one of the speakers as I was at the first conference in 1999. It was a good day for talking about policy with candid questions and answers. ECB President Mario Draghi led off with a review of current policy; I followed with a talk about asset purchase programs (my assigned topic), and for the rest of the day we listened to presentations and discussion of unconventional policy, structural reform, international coordination, and an enlightening debate between

and for the rest of the day we listened to presentations and discussion of unconventional policy, structural reform, international coordination, and an enlightening debate between  Volker Wieland and John Williams on the “neutral” real interest rate moderated by Sam Fleming of the FT.

Volker Wieland and John Williams on the “neutral” real interest rate moderated by Sam Fleming of the FT.

The previous time I spoke at this event in 2014 I examined the implications of the Fed’s large-scale asset purchases from 2009 to 2014. I argued then that the purchases did not lower longer term rates except for possible signaling and temporary announcement effects, and I pointed to ten possible negative unintended consequences:

- Distortion of price discovery in markets

- Unresponsiveness of long-term rates to key events as in normal times.

- Non-functioning of money markets

- Risk of discouraging lending and investment

- Uncertainty about unwinding

- Too much risk-taking by risk-averse investors

- Undermining of fiscal discipline

- Public questioning of the need for central bank independence

- Large re-distributive impacts

- International contagion of policy as central banks followed each other

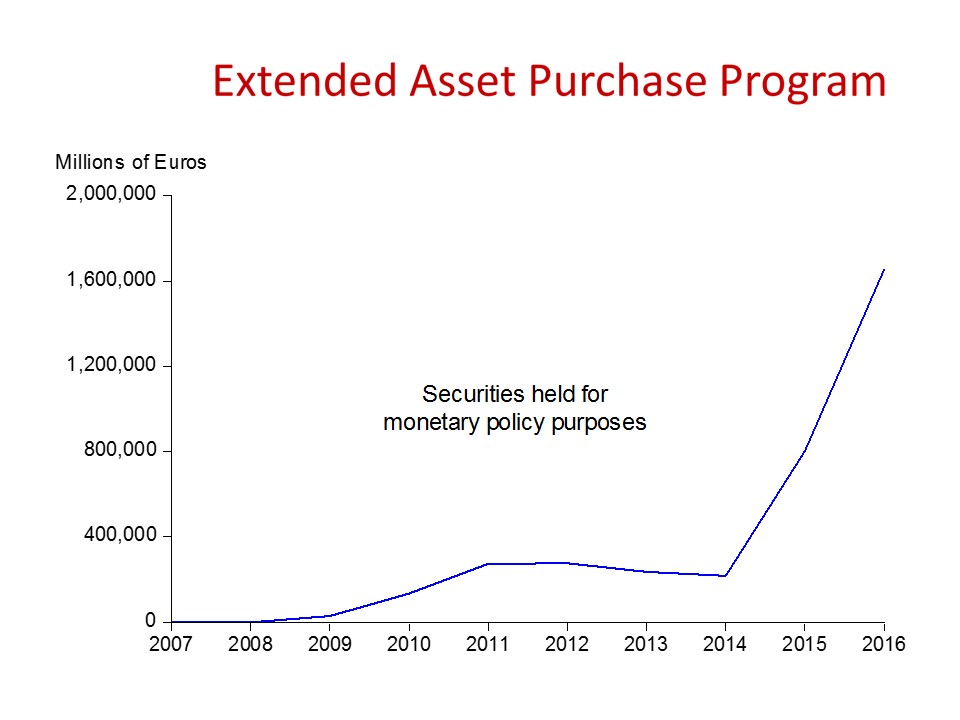

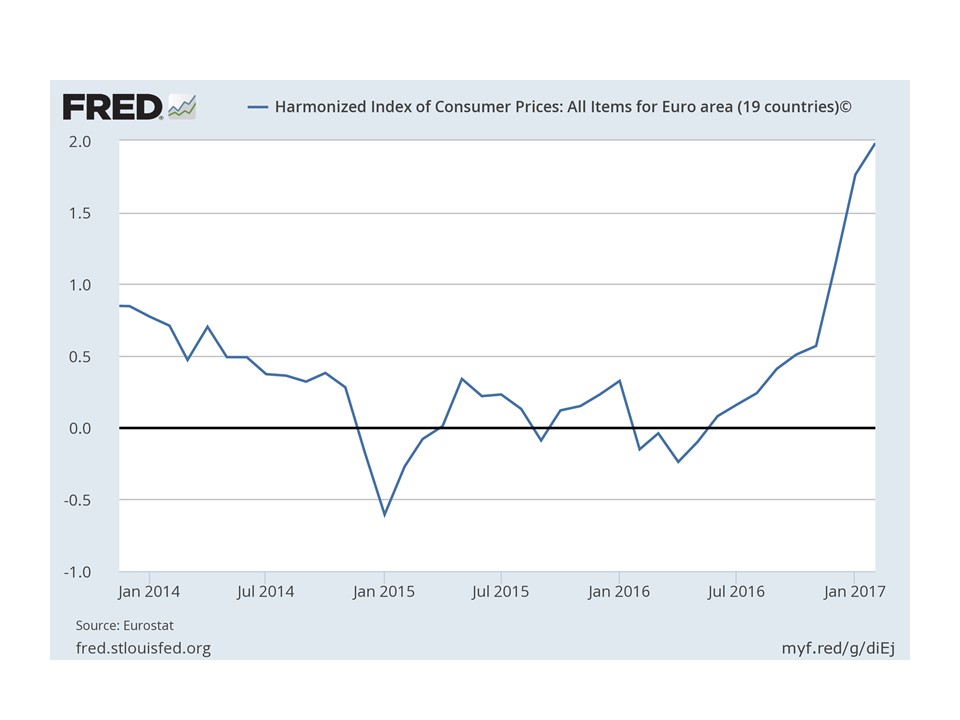

This time I examined the ECB’s asset purchase program, which expanded dramatically in 2014. I mentioned the same ten concerns (later the ECB’s Peter Praet noted they were monitoring these). But I also noted more of an impact on financial markets and possibly inflation than in the US. The graphs below show the expansion of ECB purchases and the accompanying change in the ECB inflation rate, though the latter may prove to be temporary.

There are also much more detailed studies of the ECB’s asset purchases, many of which find large exchange rate effects. Empirical work by Demertzis and Wolff in a June 2016 Bruegel Policy Contribution found a big effect on the euro exchange rate as did a January 2017 Bundesbank Monthly Report which went beyond announcement effects with dynamic regression estimates. A September 2016 ECB working paper by Andrade, Breckenfelder, De Fiore, Karadi, Tristani found effects on asset prices, though they focused on announcements; they then plugged these into a model to see the impact on lending, but, in my view, the model simulations still need to be checked for robustness.

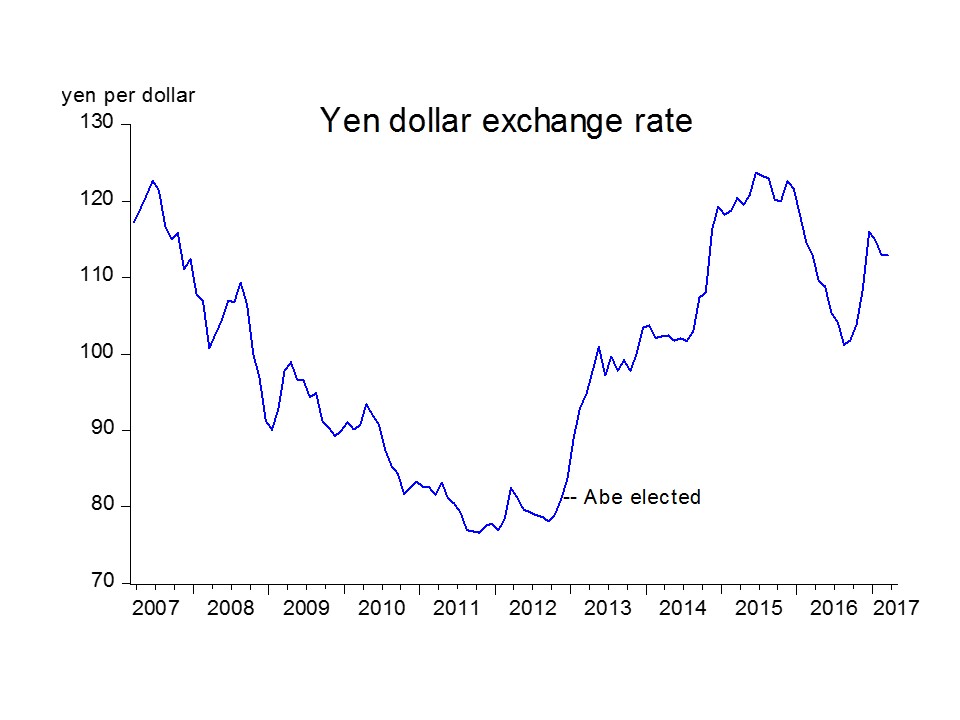

The exchange rate effects raise international issues (per the tenth unintended consequence on the above list). To see this, trace the recent history of the asset purchase programs at the Bank of Japan and ECB. During the Fed’s asset purchase program, Prime Minister Shinzō Abe, when he was first running for office, complained about the strong yen, and, when he won, he appointed Haruhiko Kuroda, who then expanded asset purchases in 2013 which was accompanied by a depreciation of the yen as seen in the yen-dollar graph.

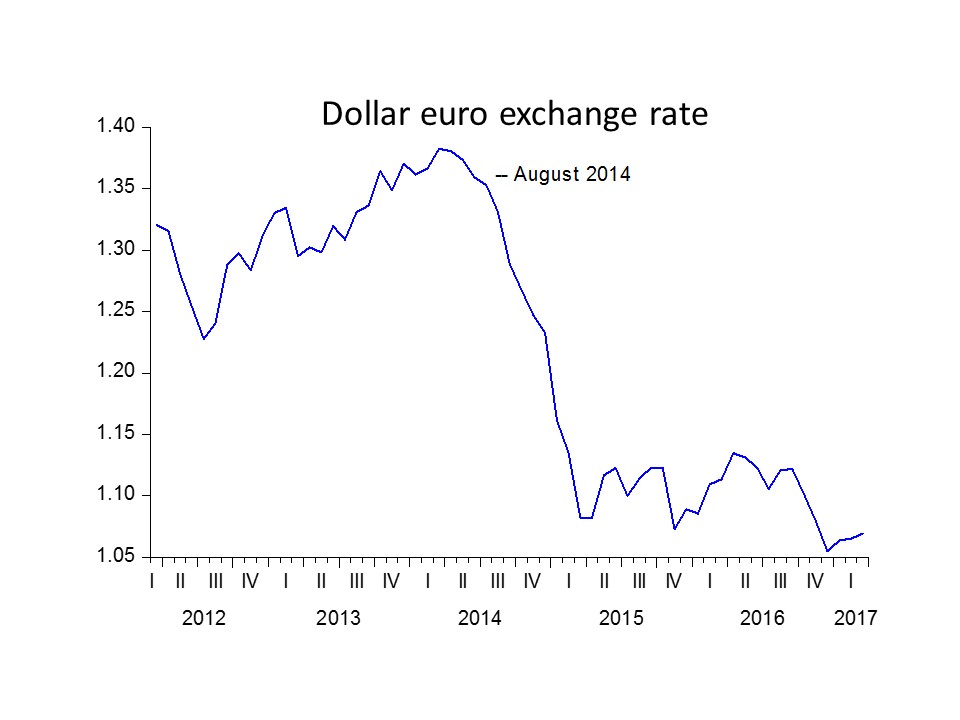

Soon after that Mario Draghi spoke about the strong euro at Jackson Hole in August 2014, the ECB’s asset purchase program began, and there was a large depreciation of the euro also shown in the euro-dollar  graph.

graph.

These international developments along with improving conditions in the euro area indicate that it is time to consider a strategy for normalizing ECB policy in a clear, predictable way. Economics and the experience with normalization by the Fed suggest ways to do it gradually and strategically (including the taper tantrum experience of what not to do). The question of sequencing (reducing the size of purchases versus policy rate increases) is best approached by paying careful attention to the negative impacts listed above, as Mario Draghi suggested in his talk, and there are special considerations for a currency zone where some countries are performing differently than others.

It would be best if normalization were toward a rules-based monetary policy which has worked well in the past, as I explained in a presentation on interest rate rules at the 1999 ECB Watchers conference. Moreover, rules-based monetary policy at the ECB, the BOJ, and other central banks would help to create a much-needed rules-based international monetary system.