During the past two days, economists from around the world gathered at the Hoover Institution to focus on the crucial problem of how to restore prosperity. They took stock of lessons from past experiences in the US and Europe, and considered possibilities with a new Administration in Washington. It was a follow up to a conference and book that Lee Ohanian and I organized 5 years ago with Ian Wright. This year Jesus Fernandez-Villaverde joined with Lee and me in the planning, adding important economic and political perspectives as well as views from Europe.

Needless to say, the need to restore prosperity is still with us, as illustrated by the chart on this cover of 2012 book (Government Policies and the Delayed Recovery) along side the updated version today—the employment-to-population ratio is still barely above the level at the end of the recession in 2009. We have go a long way to go.

A huge amount of useful new facts and ideas were put forth at the conference so a book is again planned. The conference was also notable for topics that did not come up. No one suggested secular stagnation, as introduced by Larry Summers in a 2013 Hoover-Brookings conference, as a factor in the recent slow growth. Nor did anyone suggest demand-side fiscal stimulus packages as a means of restoring prosperity. Rather, people focused on structural or supply-side economic policy as reasons for the low growth and how to implement such policies.

Slides presented at the conference will soon be available on the conference web page, and there are some really amazing charts to look at. In meantime here are some of the highlights from my perspective.

George Shultz led off—as in the previous conference—with a note of optimism and words of encouragement reviewing how changes in policy—tax reform, monetary reform—led to greatly improved economic performance in the 1980s and could do so again.

Kevin Murphy then examined the key role for education and training in raising productivity growth. He showed that returns to education have increased, but that supply has not responded leaving a great deal of growth potential on the table with special harm to those at the bottom. Rick Hanushek reported on the amazing economic growth gains that could come from simply weeding out the lowest 5% of teachers based on teaching effectiveness. Flavio Cunha examined underlying causes for poor educational performance delving into very early childhood experiences, where researchers can now monitor, for example, how many words children actually hear at home. There is no question that the US is not exceptional in K-12 education.

Bob Hall usefully decomposed empirically the recent slow growth of earnings per “member of the population,” showing that a decline in productivity growth and a drop in the share of labor in total income are the primary culprits. John Haltiwanger examined the marked decline in young firms (5 years and less) as a share of US output, and examined how that decline in dynamism might be related to the decline in productivity; he found a suggestive association for some, but not all, industries. Ed Prescott noted how technological change has created a wedge between output and real GDP citing examples of Bill Nordhaus’ work on “The Economics of New Goods.” However, Bob Hall and others noted that recent work by David Byrne, John Fernald and Marshall Reinsdorf shows that such developments are not new and do not explain changes in trends over time.

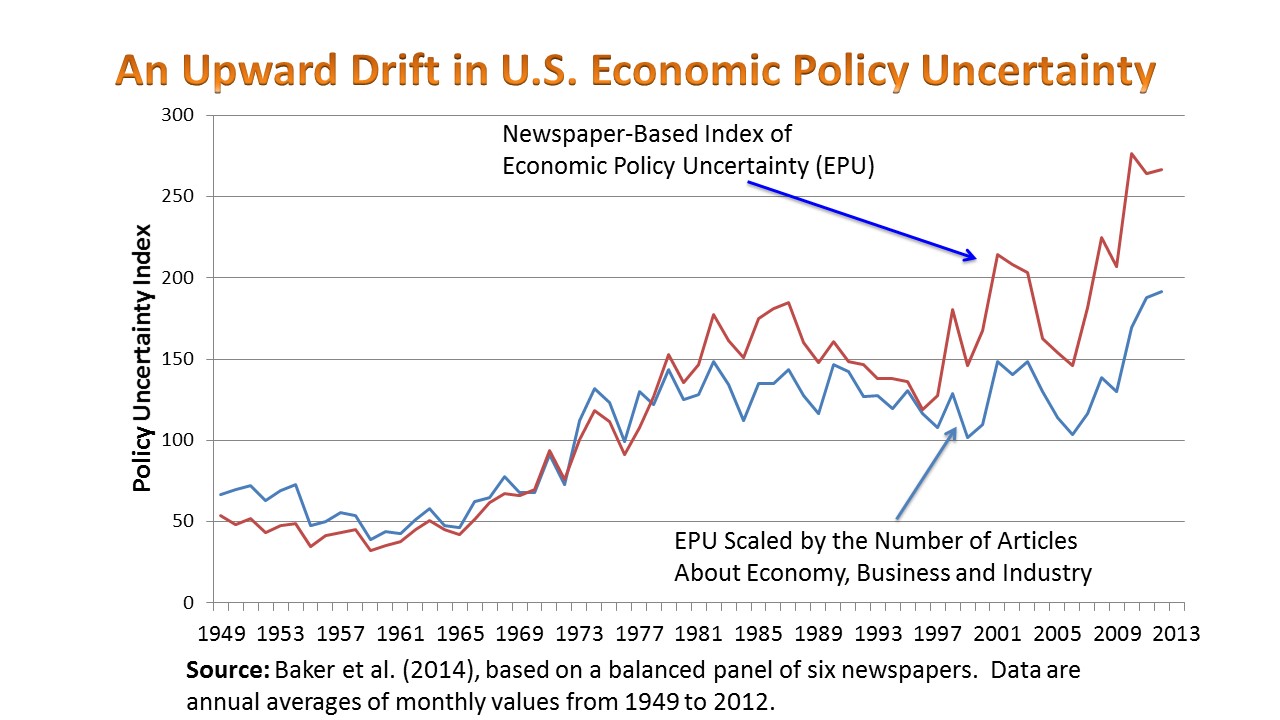

A full session concentrated on the role of government economic reforms in restoring prosperity. Harald Uhlig focused on the role government in health care examining the recent ups and downs in the price of pharmaceutical firm stocks in response to statements coming from Washington.  I assessed whether the US is having a much needed turning point in economic policy by applying the ideas in my book First Principles. This chart shows the potential gain in productivity growth if reforms such as regulatory reform and tax reform are implemented; in my view the response to such supply side reforms can be large. Steve Davis then discussed recent trends in regulation, intervention and policy uncertainty, provided new data and making new reform proposal to contain the costs. He provided a chart—which I replicate below—which shows some correlation between the swings in policy uncertainty and historical swings in productivity growth from my chart.

I assessed whether the US is having a much needed turning point in economic policy by applying the ideas in my book First Principles. This chart shows the potential gain in productivity growth if reforms such as regulatory reform and tax reform are implemented; in my view the response to such supply side reforms can be large. Steve Davis then discussed recent trends in regulation, intervention and policy uncertainty, provided new data and making new reform proposal to contain the costs. He provided a chart—which I replicate below—which shows some correlation between the swings in policy uncertainty and historical swings in productivity growth from my chart.

A good part of the conference was about the slow growth in Europe.  Much of this fascinating discussion focused on how poor policy has pulled down growth. Fortunately, the discussion will be broadcast by Russ Roberts on his famous Econtalk Podcast and includes Nicholas Crafts, Luis Garicano, and Luigi Zingales—so watch for that. Joel Mokyr talked about his new book: A Culture of Growth, and examined whether the development of a “market for ideas,” which he argues led to the Industrial Revolution, has lessons for the future. Jesus Fernandez-Villaverde spoke at lunch on European lessons for the US. To paraphrase the key lesson, coming from joint work with Lee Ohanian, is: “If the US does not get its policy act together it will surely follow Europe to stagnation.” He reminded everyone how unemployment rates in Europe used be less than in the US, and they are now of course much greater. He was not optimistic about reforms in Europe given the demographic situation in there.

Much of this fascinating discussion focused on how poor policy has pulled down growth. Fortunately, the discussion will be broadcast by Russ Roberts on his famous Econtalk Podcast and includes Nicholas Crafts, Luis Garicano, and Luigi Zingales—so watch for that. Joel Mokyr talked about his new book: A Culture of Growth, and examined whether the development of a “market for ideas,” which he argues led to the Industrial Revolution, has lessons for the future. Jesus Fernandez-Villaverde spoke at lunch on European lessons for the US. To paraphrase the key lesson, coming from joint work with Lee Ohanian, is: “If the US does not get its policy act together it will surely follow Europe to stagnation.” He reminded everyone how unemployment rates in Europe used be less than in the US, and they are now of course much greater. He was not optimistic about reforms in Europe given the demographic situation in there.

Joel Peterson, Chair of JetBlue and a leader in venture capital funding, gave the dinner talk explaining how government policy actually affects business formation and growth with many examples from his own experience. He thereby provided a much needed connection—and I would say confirmation—between the empirical/theoretical work of the economists and what actually goes on in individual firms. Some of Joel’s examples came from his fascinating new book, The Ten Laws of Trust.

Conferences like this are useful if they help bring ideas into practice. Let’s hope that when we have the next conference on economic growth and prosperity–say in another 5 years–that many of the ideas from this conference will have been applied in practice and that we might be able to title the conference “Prosperity Restored.”