Two years ago I published a piece in the Wall Street Journal titled The Economic Hokum of ‘Secular Stagnation.’ I wrote it after Larry Summers presented the secular stagnation view at a joint Brookings-Hoover conference. I argued that the bout of slow growth was not secular, but rather due to recent—and entirely reversible—swings away from good economic policy. Since then economic policy has not reversed course, economic growth has not picked up, and the economic hokum has engulfed the public intellectual world. If the past two years are any guide, the longer a policy reversal is delayed, the more that secular stagnation will appear to be real.

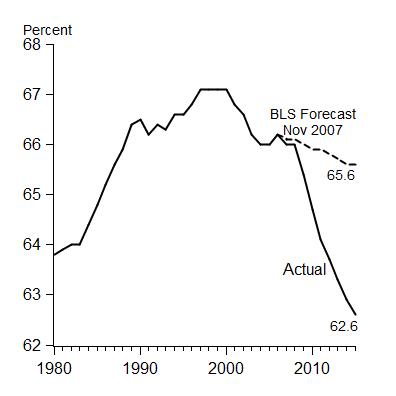

In the meantime, evidence keeps accumulating that the slow economic growth is anything but secular. Economic growth equals the sum of employment growth and labor productivity growth. With the unemployment rate at 5 percent, boosting employment growth requires an undoing of the recent sharp drop in the labor force participation rate (shown in the chart). Such an undoing is possible with right policy incentives. Comparing the 2007 BLS forecast, which took demographics into account, with the actual labor force participation rate, indicates that the sharp drop is not due to secular demographics and should be responsive to incentives from policy reforms which encourage firms to expand and hire. A three percentage point rise in the labor force participation rate from 62.6 percent to 65.6 percent—as the BLS predicted —would mean a 5 percent increase in the labor force. Over 5 years it would mean a 1 percentage point rise in the growth rate. Over ten years it would mean another .5 percent per year rise which would double the .5 percent per year now forecast by the BLS.

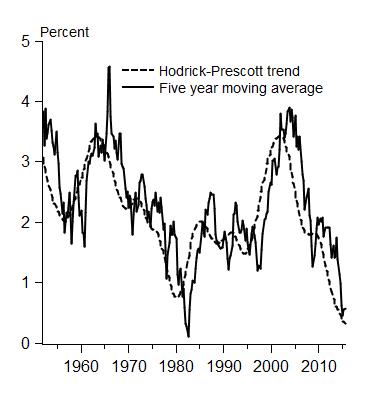

Recent labor productivity growth also reveals nothing secular. The chart below shows the cyclical-like swings in labor productivity growth in the nonfarm business sector. In my view the swings are related to policy.  According to the BLS, annual labor productivity growth fell from 3.0 percent during the years 1996-2005 to 0.7 percent during the years 2011-2014, or by 2.3 percentage points. Over those same two periods, multifactor productivity growth fell from 1.6 percent to .6 percent per year, and growth in capital services per hour fell from 3.7 percent to -.5 percent per year. Restoring these two contributors to growth to their pre-crisis levels would give a huge boost to productivity growth.

According to the BLS, annual labor productivity growth fell from 3.0 percent during the years 1996-2005 to 0.7 percent during the years 2011-2014, or by 2.3 percentage points. Over those same two periods, multifactor productivity growth fell from 1.6 percent to .6 percent per year, and growth in capital services per hour fell from 3.7 percent to -.5 percent per year. Restoring these two contributors to growth to their pre-crisis levels would give a huge boost to productivity growth.

It’s time to change policy and get all this started.