With real GDP and employment data now in for all of 2013, the recovery still looks about as weak as ever. Sure, it’s good news that growth picked up again in the 3rd and 4th quarter, but the three updated charts below, which provide a little longer perspective, look pretty much the same as they did when I started drawing them several years ago.

Employment growth during the recovery has been far too slow to raise the employment-to-population ratio from the low levels to which it fell during the recession:

Real GDP growth has been too slow to close the gap between real GDP and the 2.5% trend that represented the economy’s potential GDP from 2000 through 2006:

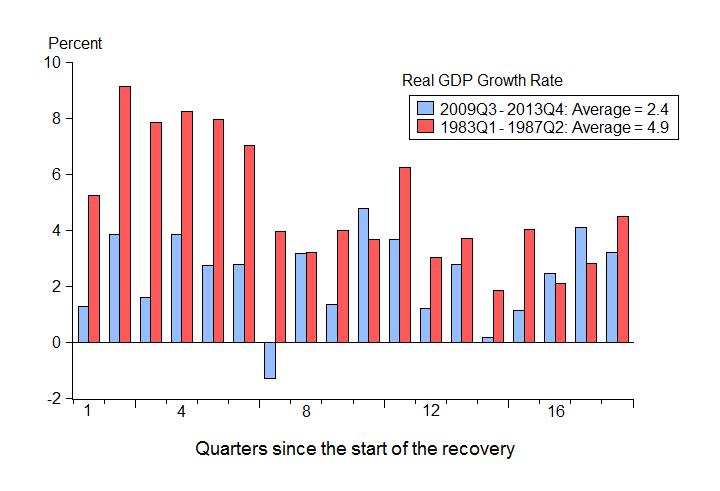

And this slow growth is in marked contrast to the rapid recovery from the previous severe recession in the early 1980s:

The big question remains why. I have been arguing for a long time that the slowness of the recovery, as well as the deepness of the great recession before that, were likely due to a significant shift in economic policy away from what worked reasonably well in the decades before. Broadly speaking, monetary policy, regulatory policy, and fiscal policy each became more discretionary, more interventionist, and less predictable in the years leading up to the crisis.

The explanation fits the facts well. There is a clear empirical association between the poor economic performance and this shift in economic policy. Macroeconomic theory that stresses the importance of time consistency, the Lucas critique, the predictability of policy, and the benefits of certain simple rules predicts that such a shift in policy would result in poorer performance. So does historical experience from the 1970s to the 1990s. So does empirical research showing that specific policy actions had adverse consequences.

The main popular alternative explanation now is secular stagnation—due to a new negative equilibrium real interest rate—a view recently put forth by Larry Summers. The “policy is the problem” view stands up well compared to this new view, but the fact that there are alternatives means that more empirical and theoretical research would be useful. If the “policy is the problem” view proves to be correct, then restoring strong sustainable growth will require changing policy to a more predictable rules-based monetary policy, a less interventionist regulatory policy, a long-term reform-oriented fiscal policy, and other reforms explained in my 2012 book First Principles: Five keys to Restoring America’s Prosperity.