Five years ago this month the Great Moderation ended. To be precise December 2007 is the month that the NBER business cycle dating committee designated as the peak of the third and final expansion of the Great Moderation and the beginning of the Great Recession.

Hundreds of research papers have been written on the nature and causes of the Great Moderation, which got started around 1983. While that research began long after the Great Moderation got underway (I published one of the earliest papers on it in 1998), we should not wait so long to start seriously researching the causes of the post-Great Moderation period, regardless of how this period is eventually named by economists.

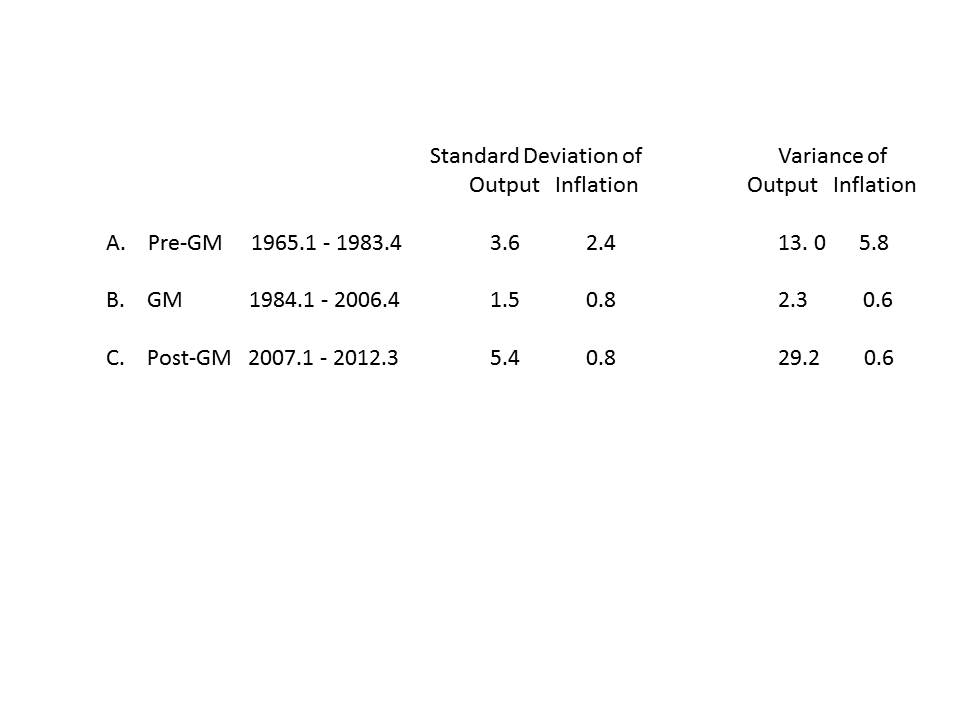

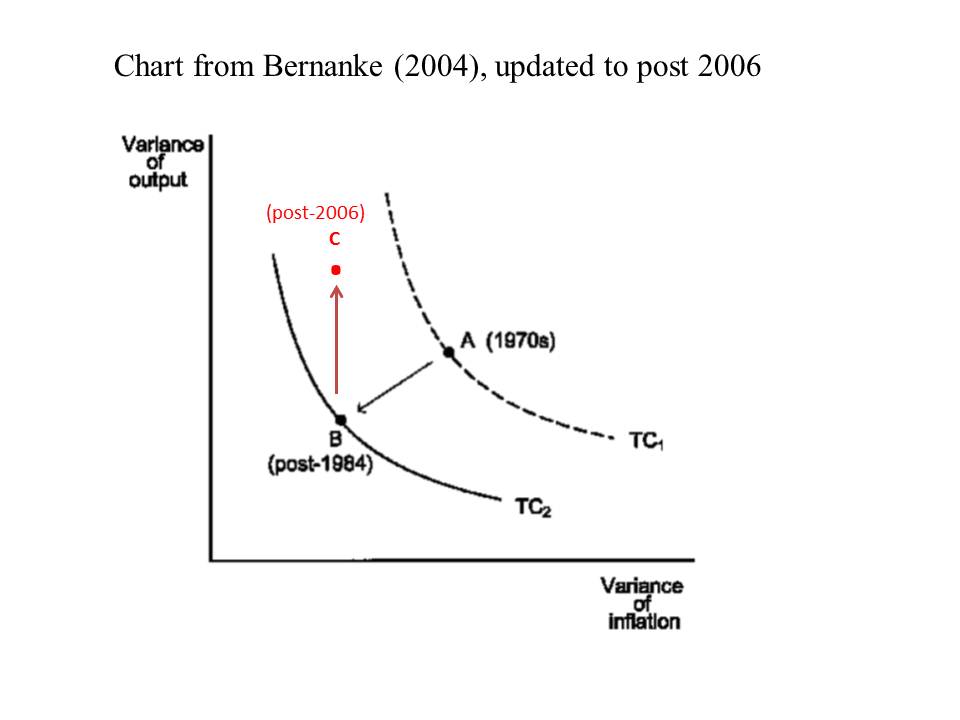

In my view, the framework that Ben Bernanke used in a February 2004 paper to study the causes of the Great Moderation is a good one. It goes back to research that started before the Great Moderation. Bernanke characterized the Great Moderation as a reduction in (1) the variance of inflation and (2) the variance of real GDP. He used the following diagram (it is a replica of Figure 1 in his paper) in which these two measures are on the horizontal and vertical axes respectively. Using the diagram he represented the Great Moderation as a move from point A to point B. He showed that a primary cause was better monetary policy, and he represented this by showing that better policy brought the economy closer to the true policy tradeoff curve (TC2) rather than the occurrence of a shift in the curve (from TC1 to TC2) . I completely agree with that interpretation.

But what caused the end? I have updated Bernanke’s diagram by adding a point C and a line from point B to point C (in red), based on the empirical volatility measures in the table below for the three periods. Observe that the post-Great Moderation deterioration does not simply retrace the previous improvement. It is nearly vertical, reflecting that virtually all the deterioration is in the output variability dimension.

In my view monetary policy was a major factor in the end of the Great Moderation just as it was the major factor in the Great Moderation itself. I review the reasons for this view in this paper on central bank independence versus policy rules which I am presenting at the annual meeting of the American Economic Association next month.