In Jared Bernstein’s interesting recent piece “Checking in on the Taylor Rule and the Fed,” he writes that the federal funds rate has been “camping out at between -1 and -2 percent” according to the Taylor Rule.

He then goes on to give this definition the Taylor Rule: The federal funds rate should equal

2 + p + 0.5(p – 2) + y

where p is year-over-year percent change in the PCE inflation index and y is the output gap: 2*(nairu-unemp) where 2 is the Okun coefficient and the nairu is from CBO.

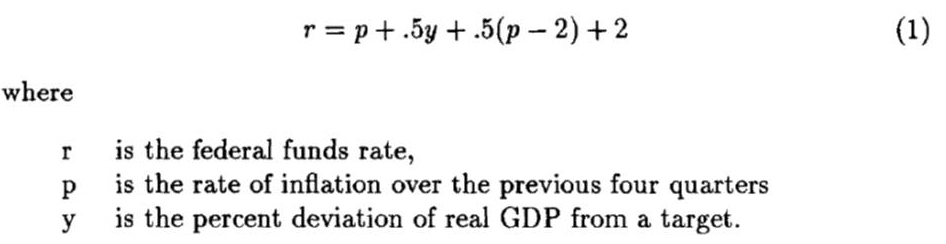

But this is not the policy rule I recommended in a 1993 paper using a formula which has come to be called the Taylor Rule. Here is the formula copied from that paper*

The two equations may looks similar, but there is a key difference. Bernstein’s formula leaves off the .5 coefficient on y. Thus, he effectively doubles the impact of the output gap on the interest rate compared to what I recommended then—and still recommend now.

How much difference does this make? For the first quarter of this year, I calculate that Bernstein’s output gap (y) is about -4.4% [that is, 2*(5.5- 7.7)]. So if you use 0.5 rather than 1.0 for the coefficient on y, the interest rate would be 2.2 percentage points higher than Bernstein calculates. (The difference was much larger in 2009 and 2010 when the gap was larger). Adding back in the 2.2% puts the interest rate into positive territory (say 0.7% rather than -1.5%), which would mean that the zero-lower-bound on the federal funds rate is not “a serious macroeconomic constraint on policy” contrary to what Bernstein argues. That constraint is the rationale for quantitative easing and forward guidance.

I realize that there are differences of opinion about what is the best rule to guide policy and that some at the Fed (including Janet Yellen) now prefer a rule with a higher coefficient. But at the least people should be cross-checking below-zero interest rate calculations and debating the difference with other approaches when the Fed’s rationale for purchasing $85 billion per month of mortgage-backed and Treasury securities hangs on those calculations.

There are other important cross-checks on such calculations. Bernstein’s estimate of the output gap uses an Okun’s law coefficient of 2, but if you use 1.5 (the empirical estimate over the past 50 years) rather than 2, the gap is smaller, which also moves the rate up toward positive territory. Similarly, the average of the San Francisco Fed’s most recent survey of output gaps is smaller than what Bernstein uses. And the inflation rate over the past 4 quarters with the GDP price index is higher than with the PCE price index used by Bernstein; that cross-check also pushes the interest rate toward positive territory.

*Discretion Versus Policy Rules in Practice, Carnegie-Rochester Series on Public Policy, North-Holland, 39, 1993, pp. 195-214