The Plaza Accord, which took place 30 years ago this month, provides two important (and fascinating) economic lessons essential for anyone interested in reforming, or simply teaching, the international monetary system. First, sterilized exchange market interventions are largely ineffective. A newly published book, Strained Relations, by Mike Bordo, Owen Humpage, and Anna Schwartz makes this crystal clear using data from the period. They studied 129 separate interventions against the yen and mark and found “no support for the view that intervention influences exchange rates in a manner that might force the dollar lower, as under the Plaza Accord, or maintain target zones as under the Louvre Accord”

That the dollar depreciated across the board—as much against the mark as against the yen—suggests that it was part of a general reversal of the dollar appreciation experienced during 1981-1985 due to the monetary policy strategy the Fed had put in place. As Alan Greenspan put it in an FOMC meeting in 2000, “There is no evidence, nor does anyone here [in the FOMC] believe that there is any evidence to confirm that sterilized intervention does anything.”

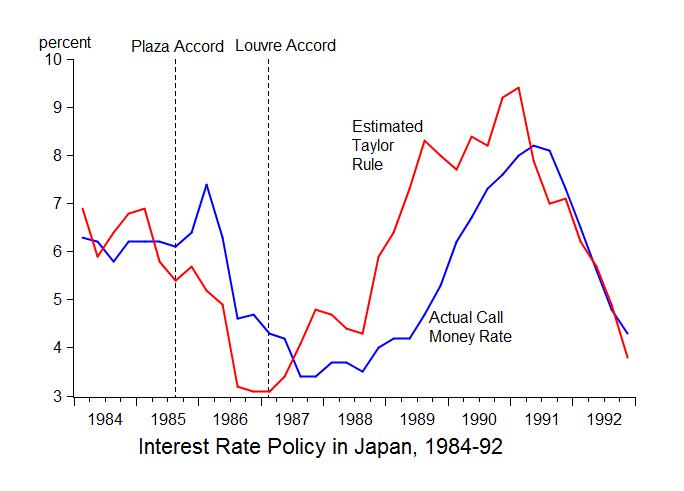

Second, the Plaza Accord had widely different effects on the monetary policies of the 5 participants: France, Germany, Japan, the US, and the UK. Compare the US and Japan, for example. For Japan there was a clear effect on its monetary policy strategy. The following chart, which comes directly from a chart published by the IMF, shows the actual policy interest rate in Japan (the call money rate) for the years 1984 to 1992 along with the policy rate recommended by the Taylor rule as calculated by the IMF. The chart shows how the interest rate was too high relative to the rules-based policy in late 1985 and throughout 1986. It also shows the swing with the policy rate set well below the rule from 1987 through 1990.

The dates of the Plaza and the Louvre meetings are marked in the chart. Observe how the move toward an excessively restrictive policy starts at the time of the Plaza meeting. Indeed, as chart shows, the Bank of Japan increased its policy rate by a large amount immediately following the Plaza meeting, which was in the opposite direction to what macroeconomic fundamentals of inflation and output were indicating. Then, after a year and a half, starting around the time of the Louvre Accord, Japanese monetary policy swung sharply in the other direction—toward excessive expansion. The chart is remarkably clear about this move. The policy interest rate swung from being up to 2¼ percentage points too high between the Plaza and the Louvre Accord to being up to 3½ percentage points too low during the period of time from the Louvre Accord to1990.

The evidence of an effect of the Plaza Accord on Japanese monetary policy goes beyond this simple correlation. The Plaza and Louvre communiques included specific commitments about Japanese monetary policy actions. In the Plaza Accord Statement, the Government of Japan committed to “flexible management of monetary policy with due attention to the yen rate.” In the Louvre Accord Statement, “The Bank of Japan announced that it will reduce its discount rate by one half percent on February 23.” Thus, the policy deviations were clearly due to the way that Japan implemented the Plaza Accord and later the Louvre Accord.

In contrast, for the US, the Fed’s monetary policy strategy was not affected at all, as Chairman Paul Volcker readily admits. The communique simply confirmed that the overall strategy that the Fed was pursuing would continue.

As will I explain in a paper prepared for the 30th anniversary conference next week, these two lessons have important implications for the future. What is past is prologue. Study the past.